What Are Options and Why Are They Needed

An option is a derivative financial instrument with a fixed term that gives the right to buy or sell an asset in the future (a stock, index, cryptocurrency, commodity, etc.) at a pre-agreed price.

It is important to understand that the option buyer is not obliged to buy or sell the asset under the contract. In turn, the option seller is obliged to fulfill their obligations (to sell or buy the asset at the pre-agreed price) if the buyer demands it.

The Tlap portal is beginning to study options and invites you to join this extremely exciting, though quite labor-intensive, process. Here is what we found and summarized in simple words.

What are options for participants in the derivatives market?

Insurance. The option buyer insures themselves against the asset becoming cheaper or more expensive.

A classic example: the Mexican government annually buys an over-the-counter put option from Barclays, Deutsche Bank, Goldman Sachs, Morgan Stanley. This option insures Mexico against an oil price decline below a certain level.

Investment bankers also insure (hedge) their risks on these options and therefore protect the price written into the contract in one way or another. Naturally, if the price of oil for various reasons falls below the agreed price level, or the strike, the bankers pay Mexico the money due under the contract.

Thus, from 2001 to 2017 Mexico netted about $2,4 billion from options, having paid option sellers $11,7 billion and received $14,1 billion back.

On the other hand, over 16 years the bankers got funds to manage at just over 1,7% per year. That is an excellent long-term cost of money. The only hard year was 2020, when oil fell through the floor and Mexico immediately received $6 billion in payouts. Goldman Sachs suffered the most in this operation, but they quickly made it back.

A bet. The option buyer uses different methods to determine the probability of volatility increasing and the direction of price movement within the specified time, and in fact places a bet on that movement.

I will give the example of Canadian lone trader Christopher DeVocht, who bet on a strong rise in Tesla shares in 2019–2021. He backed his expectations with the purchase of call options and further pyramiding.

And this produced an excellent result: if in 2019 he had $88 000 in his brokerage account, then by the end of 2021 the deposit had grown to $415 million. And all this thanks to bets on explosive growth in Tesla shares and margin pyramiding.

And then Tesla shares went down, which led to an almost complete wipeout of the deposit. This time margin pyramiding played a cruel joke on Christopher DeVocht. Then came the lawsuits, where our hero accused brokers of causing his blow-up, but that is a completely different story.

Options in simple words

The main terms in the world of options are as follows:

- Call: an option for upside.

- Put: an option for downside.

- Strike: the fixed price at which the asset can be bought or sold in the future.

- Premium: the cost of the option when buying it.

- Intrinsic value: the difference between the asset price and the option strike.

- Time decay: the constant decrease in the value of an option as the expiration date approaches.

- Implied volatility: the future amplitude of fluctuations in the asset price expected by the market and built into the current option price. This is the "price of fear and greed."

- Expiration: the date the option expires, after which it becomes worthless.

- Exercise: the realization of the right to buy or sell the asset to the option seller.

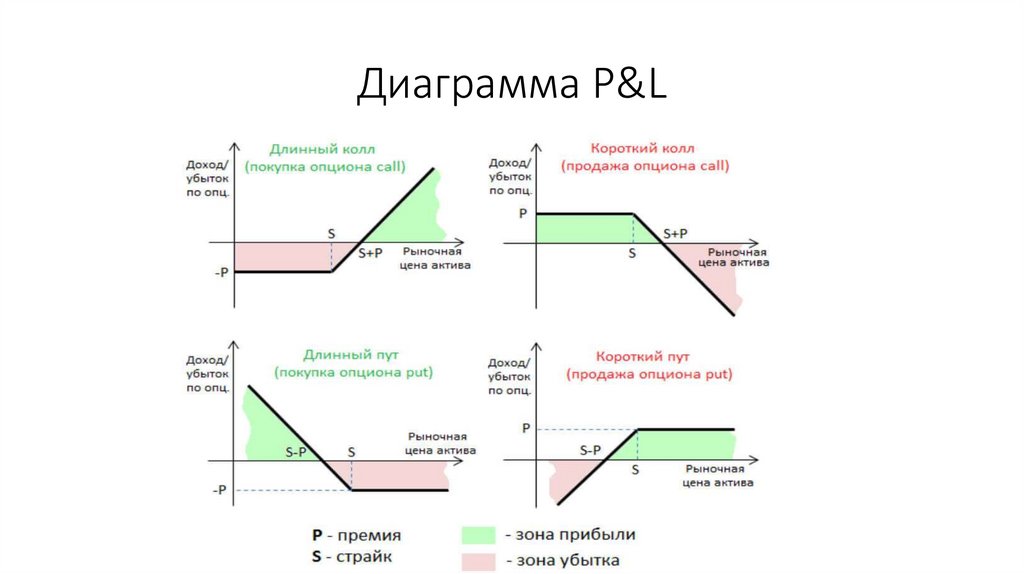

At first glance, the mechanics of working with options are fairly simple.

The option buyer pays the premium. Their risk is limited to this premium, while the profit potential is high. In turn, the option seller receives the premium immediately. Their risk is potentially unlimited (for a call) or very large (for a put), while profit is limited to the premium received.

Exercise and sale on the market: American and European options

There are two types of option exercise: American and European. Their key difference lies in the timing of exercise.

An American option can be exercised on any business day up to and including the expiration date, while a European option can be exercised only on the expiration date itself.

Early exercise of an option makes it possible to lock in profit immediately or limit loss. In addition, early exercise of a call makes it possible to get the asset cheaper than the market in the event of explosive growth and the expectation of its long-term continuation. Early exercise of a put, for example, makes it possible to sell shares above the current price after the ex-dividend date. Thus, by exercising a put option, the trader receives double profit: from dividends and from selling the stock above the market.

On the other hand, it is often more profitable to sell the option itself on the market than to exercise it. The reason lies in time value, which is discussed in more detail below. If an option is "in the money" (also more on that below), then its price equals the sum of intrinsic value and time value. By exercising the option, the buyer receives only intrinsic value, whereas by selling the option, the buyer also receives the remaining time value.

For example, a buyer has a Call on a stock currently worth 12₽ with a strike of 90₽. The current stock price is 100₽. If the option is exercised, the profit will be 10₽. But if the option itself is sold on the market, the profit will be 12₽ (10₽ of intrinsic value + 2₽ of time value).

On the expiration date, all options that are "in the money" are exercised automatically (I will explain what that means below). Options that are "at the money" or "out of the money" expire worthless and produce a loss equal to the option premium.

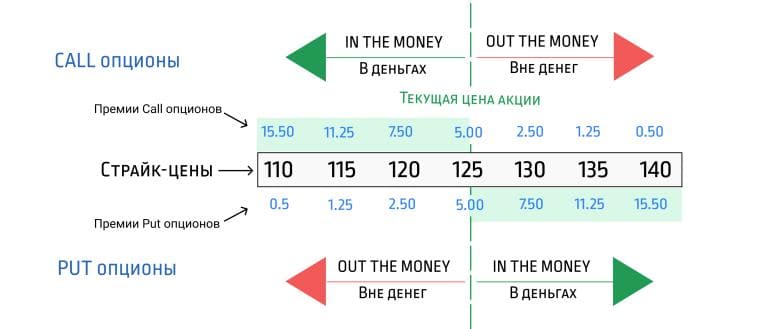

In-the-money, ATM, and OTM options

To characterize the current financial state of an option relative to the price of the underlying asset, the following concepts are used: In the Money (ITM), At the Money (ATM), and Out of the Money (OTM).

An option "in the money" is a contract that is profitable right now. Its premium consists of intrinsic value (the difference between price and strike) and time value (hope for even greater profit).

If an option is "in the money," then it has intrinsic value and therefore can already generate a profit right now.

For example, a call option on bitcoin was bought with a strike of 90000$, and the current price is 100000$. If the option is exercised immediately, the "paper" profit net of costs will be 10000$.

In turn, a put option on bitcoin was bought with a strike of 110000$, and the current price is 100000$. In this case, if the option is sold immediately, the "paper" profit will also be 10000$.

An option "out of the money" has no intrinsic value, and exercising it right now will lead to a loss.

If bitcoin is worth 100000$, and the call option has a strike of 110000$, then there is no point in exercising it. With the same bitcoin price of 100000$ and a put strike of 90000$, there is likewise no point in exercising the right to sell the asset.

Thus, an OTM option is a pure bet on the future. It has no intrinsic value, only time value. It is the cheapest of all, but for it to bring profit, the market must move strongly in the desired direction. These are the riskiest, but also the potentially most profitable, options.

For an option "at the money", the price of the underlying asset is equal or very close to the strike. For example, the strike of bitcoin options is 90000$, and the price of the coins is also around 90000$.

In other words, ATM is a point of balance. Exercising the option right now will bring no profit at all (intrinsic value = 0). The entire option price is pure time value (only "hope" for movement). These are the most popular options for trading, since they are the most sensitive to changes in the asset price.

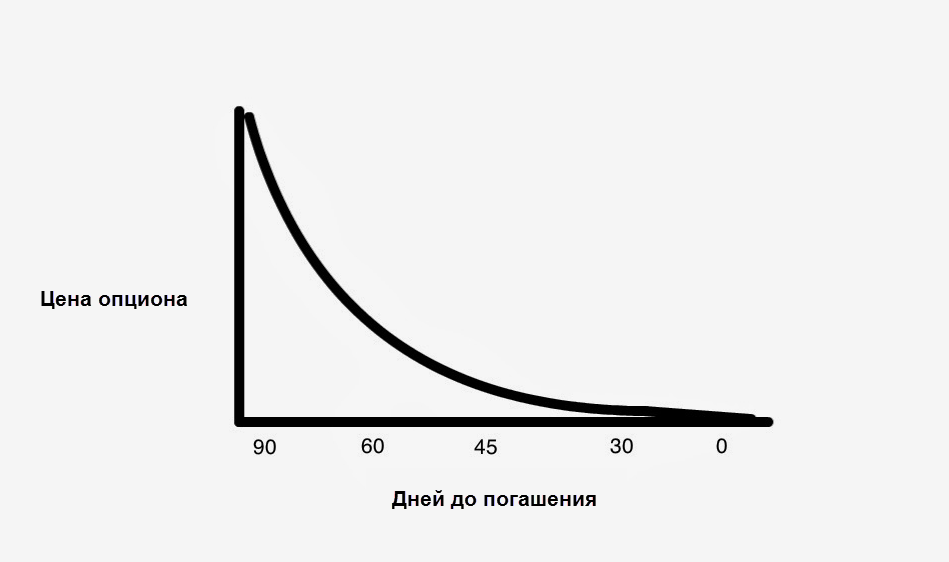

Option time decay

It would seem that everything is simple with options trading, but if you take time decay into account, the options game becomes more complicated.

The value of an option consists of two parts: "intrinsic value" (is there real benefit right now) and "time value" (the chance that this benefit will appear later).

Time value is the "hope premium" that the buyer pays. The more time there is before expiration, the greater the chances that the asset price will move in the right direction, and the more expensive this "premium" is. Every day, the "time for hope" shrinks, so time value continuously decreases. This process is called time decay.

Time decay is not a linear process and accelerates as the expiration date approaches. 3 months before expiration the option loses value slowly, in the last month significantly faster, in the last week very quickly, and on the last day catastrophically fast.

Time is the option buyer's main enemy and the seller's important friend.

The option buyer always counts on rapid growth of the asset, otherwise time decay will "eat up" the profit. In other words, time works against the buyer, even if the asset price is moving in the right direction, but slowly.

In turn, the option seller not only receives the premium immediately, but time also works for them.

Implied volatility

Implied Volatility (IV) is perhaps the most difficult concept to understand and at the same time the key one for successful options trading. Without understanding Implied Volatility, it will be difficult to make a profit.

In simple words, implied volatility is the future amplitude of fluctuations in the asset price expected by the market and built into the current option price. It is the "price of fear and greed."

To understand implied volatility, it is necessary to take into account historical (realized) volatility, which is the range of the asset's fluctuations in the past. In turn, Implied Volatility is the current expectation of future amplitude, which can change over time.

Knowing the current option price, the asset price, the strike, and the time until expiration, one can calculate the expected future volatility that leads to such an option price. The Black-Scholes formula is used for this calculation, which we will discuss another time.

Thus, implied volatility is a quantitative assessment of expectations of future movements that forms time value. The higher the IV, the sharper the moves in the market will be. In the case of low IV, traders assume that the market will be calm.

Implied volatility is the main driver of time value. If all other parameters (asset price, time) are frozen, then a rise in IV will instantly increase the price of all options (both calls and puts), and a fall in IV will reduce it. This is critically important.

By the way, the VIX "fear index" is IV in its pure form. When there is panic in the market (regardless of the reason), everyone starts buying options for protection, their price flies up, and that means the IV measured by VIX also flies up.

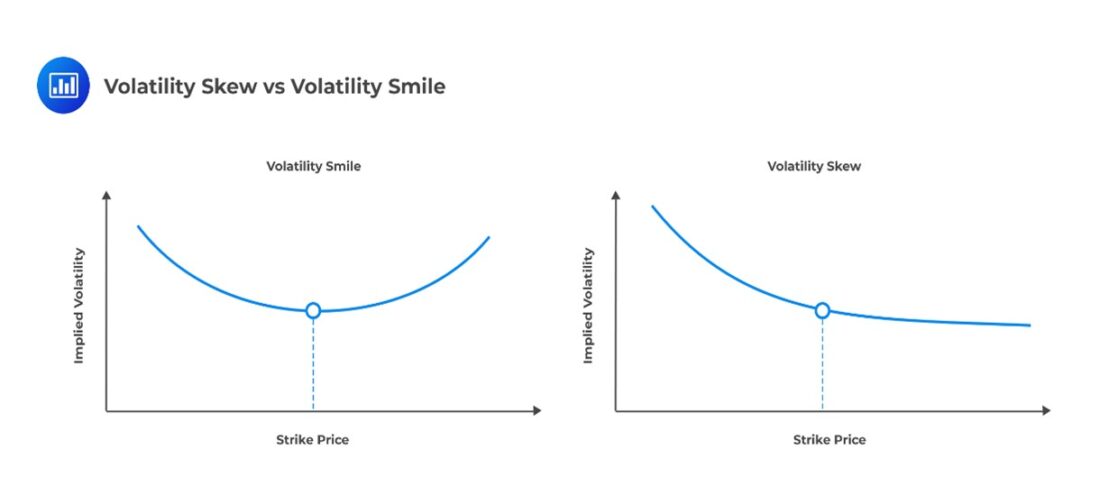

IV has the shape of a "smile" or a "skew" (Volatility Smile/Skew).

With a "volatility smile," the implied volatility of options with strikes around the current price of the underlying asset is, as a rule, lower than the volatility of options with distant strikes.

Often, IV is not the same for different-strike out-of-the-money (OTM) options. In turn, out-of-the-money put options (downside insurance) have higher IV than calls. This is the "skew": the market is more afraid of a sharp collapse than a sharp rise.

The Greeks: key risk indicators

The "Greeks" make it possible to move from intuitive guesses ("it seems the option should become more expensive") to precise quantitative risk analysis ("if the stock rises by 1 ruble, the option will rise by 60 kopecks, but overnight it will lose 10 kopecks because of time, unless volatility jumps").

The main Greeks are as follows:

Delta (Δ) is "Speed".

Delta shows how an option's price will change when the underlying asset changes by 1 unit. If the delta of a call = 0.6, then if the asset rises by 10 rubles, the option will rise by 6 rubles. It moves with the stock, but does not fully keep up with its price.

Delta is the probability that the option will be in the money by the expiration date. The range of a call's delta is from 0 (far out of the money) to +1 (deep in the money), and for a put it is from 1 to 0.

Gamma (Γ) is "Acceleration".

Gamma shows how delta itself will change when the stock price changes by 1 unit. High gamma means that a position can sharply accelerate or slow down.

For example, we have a call with a delta of 0.5 and a gamma of 0.1. The asset rose by 1 ruble. The new delta = 0.5 + 0.1 = 0.6. Now the option will react even more strongly to the asset's movement (0.6 for the next ruble).

Gamma is highest for at-the-money (ATM) options and lowest for far out-of-the-money and deep in-the-money options.

Theta (Θ) is "The Timer" or "The Ticking Clock".

Theta shows how much the price of an option will decrease over time, all else being equal. Theta is almost always negative for the option buyer (time works against them) and positive for the seller (time works for them).

For example, a theta of -0,05 means that the option price will decrease by 5 cents every day if nothing changes.

Vega (V) is "Sensitivity to panic and greed".

Vega shows how the price of an option will change when implied volatility changes by 1 point (for example, from 20% to 21%). If volatility (fear) rises, then insurance (the option) becomes more expensive, even if the asset price stands still.

Vega is positive for both calls and puts. Rising volatility increases the price of all options, because the probability of large moves increases.

Rho (ρ) is "Sensitivity to rates".

Rho shows how the price of an option will change when the interest rate changes by 1%. This is the most "macroeconomic" Greek.

Higher rates make buying assets on credit more expensive, which theoretically makes puts slightly cheaper and calls slightly more expensive. Over short periods and for individual assets, the effect of Rho is minimal. Rho is of great importance for long-dated options and index portfolios.

The role of options in forming asset prices

The role of options in determining (forming) asset prices lies in the fact that they contain concentrated information about market expectations, risks, and likely scenarios for the future price of the underlying asset. The key aspects can be examined by describing them as follows:

Options as a source of market expectations.

The price of an option reflects market expectations about the future level of the asset price, the probability of strong moves, and the asymmetry of risks (upside vs downside).

Connection through arbitrage.

Options, futures, and the spot price are linked by arbitrage relationships. A violation of these relationships leads to arbitrage, which returns the asset price to a "fair" level. Thus, the options market "disciplines" the underlying asset market.

Information about the probability distribution of price.

From the prices of options at different strikes, one can recover the risk-neutral distribution of the future asset price (the Breeden-Litzenberger result).

This makes it possible to assess the probability of extreme moves, identify "fat tails," and understand where the market sees the main risks. Neither spot nor futures can provide this on their own.

Hedging and influence on the spot market.

Options are actively used for hedging. By selling options, market makers hedge delta in the underlying asset, which creates order flow in the spot market and influences the price.

Options and the risk premium.

The option price includes time value and compensation for the risk of tail events, including crash risk. This helps to assess risk premiums, which are then reflected in the price of the asset itself as well (for example, the equity risk premium).

Role in asset pricing models.

Modern models use option data to refine stochastic volatility, estimate jump processes, and calibrate models (Heston, SABR, etc.). Without options, asset pricing models would be substantially less accurate.

Let us summarize

Options are complex, but accessible to understanding. And if they are accessible to understanding, then they can be traded or used as a tool that indicates current and expected price behavior.

But we will talk about that in the following materials.

Respectfully,

Ivan Rusin