Vertical Spread in Options: Key Points

In this material, we will continue studying options trading strategies. In the previous article, we covered the simplest strategies: directional options trading and creating synthetic futures.

Today we will talk about trading vertical spreads, more complex strategies whose clear advantage is predefined profit and loss. Traders here cannot earn more than the calculated amount, but they also cannot lose more than the calculated amount.

This material is for informational purposes, cannot and should not be construed as a consultation or advice.

Vertical Spread: A Strategy with Limited Risk

There are four basic types of vertical spreads: Bull Call Spread, Bull Put Spread, Bear Call Spread, and Bear Put Spread.

Do not understand what this is about? Then go and first read the basics about options, and then continue studying this material.

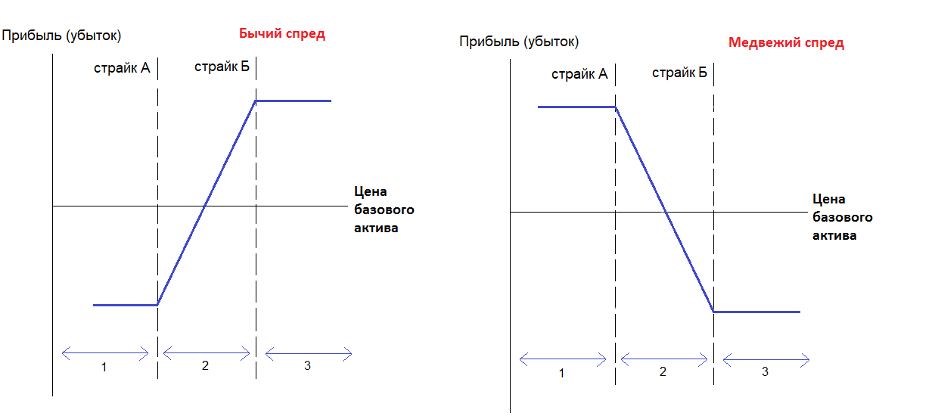

Bull Spreads

Bull Call Spread

This options strategy is used with a moderately bullish outlook. The structure of the strategy looks as follows. The trader buys a Call option with a lower strike and simultaneously sells a Call with a higher strike.

A Bull Call Spread has a lower cost compared with buying a single option and has limited risk. The downside is that potential profit is limited by the level of the sold Call.

The profit calculation looks like this:

(sale price of the call option - purchase price of the call option) - total premium. The break-even point equals the purchase price of the call option + total premium.

As an example, let us consider a hypothetical situation on ETH.

The trader buys a call option with a strike of 2000 and sells a call option with a strike of 2200. The premium for the call (strike 2000) is 120$, and the premium for the 2200 call is 60$. Thus, the net cost of this vertical spread is 60$ (60-120).

The profit profile looks as follows.

| Column 1 | Column 2 |

|---|---|

| ETH Price | Result |

| 1800$ | −60 |

| 2000$ | −60 |

| 2100$ | +40 |

| 2200$ | +140 |

| 2500$ | +140 |

In this example, the loss is limited to 60$, and the profit to 140$. The break-even point is at 2060$.

Bull Put Spread

The structure of a Bull Put Spread is similar to the previous one in construction, but opposite in outcome: the trader sells a Put with a higher strike and buys a Put with a lower strike.

This strategy makes a profit if the price remains above a certain level. At the same time, the maximum income is limited by the premium received, and the loss by the difference between the strikes.

For example, the price of ETH is 2000$, the 2000 put is sold for a premium of 120$, and the 1800 put is bought for a premium of 60$. The net profit in this options structure is immediately 60$.

The profit profile in this case looks like this.

| Column 1 | Column 2 |

|---|---|

| ETH Price | Result |

| 2200$ | +60 |

| 2000$ | +60 |

| 1900$ | −40 |

| 1800$ | −140 |

| 1500$ | −140 |

Thus, the maximum profit is 60$, while the loss is 140$. The breakeven point is 1940$.

This strategy assumes that the asset (ETH) will not fall below 2000$, but will rise moderately or remain in a sideways range.

The advantages of the strategy are that profit is formed immediately at the moment the structure is created; the downside is that the potential risk is greater than the potential profit.

To sum up, at first glance the bull put spread seems less interesting. But in a consolidation situation it often happens that the difference in premiums gives more profit than the profit from the difference in strikes.

Bear Spreads

Mirror-image structures are used to trade a falling market.

In general, bear put and call spreads are built in a similar way. The only difference is that the trader sells an option with a lower strike and buys one with a higher strike, whereas in bull spreads the trader buys the lower strike and sells the higher one.

Traders more often form a bear put spread, because in this case the loss is limited by the difference in premiums, while the maximum profit is the income from the difference in strikes taking into account the loss from the difference in premiums.

In turn, the bear call spread seems less profitable: you cannot earn more than the difference in premiums here, while the loss depends on the difference in strikes and premiums.

Bear Put Spread

Let us immediately examine this trading strategy using the example of ETH, whose price is, let us assume, $2000.

The trader buys the Put 2000 for 120$ and sells the Put 1800 for 60$. Thus, the initial loss from the difference in strikes is 60$.

Let us look at the payoff profile.

| Column 1 | Column 2 |

|---|---|

| ETH Price | Result |

| 2200$ | −60 |

| 2000$ | −60 |

| 1900$ | +40 |

| 1800$ | +140 |

| 1500$ | +140 |

The breakeven point is at 1940$, the loss is limited to 60$, and the profit to 140$.

The strategy is used when the trader expects ETH to decline, but not collapse.

Bear Call Spread

And again the same example with ETH.

The coin price is 2000$. The trader sells a call option (strike 2000) and buys a call option (strike 2200). The trader immediately receives a premium of 120$ for selling the call 2000 and pays a premium of 60$ for buying the call 2200. The immediate income is 60$.

The payoff profile is as follows.

| Column 1 | Column 2 |

|---|---|

| ETH Price | Result |

| $1800 | +60 |

| $2000 | +60 |

| $2100 | −40 |

| $2200 | −140 |

| $2500 | −140 |

By now it is clear to everyone that the maximum profit is the difference in premiums of 60$, while the loss does not exceed 140$. The breakeven point is at 2060$.

This options strategy is recommended during consolidation when a decline is expected.

The Effect of Time Decay on Vertical Spreads

Vertical spreads are limited in both profit and loss. With a proper understanding of what is happening in the market, as well as with the right choice of option. Which options are better to choose?

In my opinion, for trading a vertical spread it is better to choose quarterly options, or at worst monthly ones. The reason is banal: the longer the holding period, the greater the chances of entering the profit zone and closing the structure against the market maker in the case of American options (CME exchange), or finding a counterparty in the open market (crypto exchanges like Bybit or Binance) in the case of European options.

On the other hand, the longer you hold an option, the more the dependence on theta grows, that is, the time decay of options. Let me remind you that the closer the expiration, the more sharply the value of options located at ATM, and even more so OTM, falls.

Below is a convenient table on time decay (time decay / theta) in vertical spreads. It is important to remember that for vertical spreads theta is not constant: bullish spreads have negative theta, while bearish spreads have positive theta, which is why the overall effect depends on where the spot is relative to the strikes.

| Column 1 | Column 2 | Column 3 | Column 4 |

|---|---|---|---|

| Spread | When time helps | When time hurts | In short for a beginner |

| Bull Call Spread | If the price is close to the upper (short call) strike or above it, the spread can benefit from time because this call decays faster. | If the price is close to the lower (long call) strike or below it, the spread usually loses from time because that call decays faster. | For a bull call, time is not always a friend; in the "right" zone it already starts to work better. |

| Bull Put Spread | If the price is close to the upper (short put) strike or above it, the spread earns from time decay because the short put decays faster. | If the price is close to the lower (long put) strike or below it, time decay starts to harm the position. | For a bull put, time is usually on the premium seller's side as long as the market does not collapse downward. |

| Bear Call Spread | If the price is near the upper strike, the spread can benefit from theta. | If the price goes upward, the spread loses value; when it moves toward the short call, time no longer saves it. | For a bear call, decay usually helps as long as the market does not break the upper barrier. |

| Bear Put Spread | If the price is close to the lower (short put) strike or below it, time decay can help; the sold put decays faster. | If the price is close to the upper (long put) strike or above it, the spread usually loses from time because the bullish put decays faster. | For a bear put, time more often works against the buyer if the market does not fall fast enough. |

Thus, professionals take time decay into account when creating vertical spreads, but our article is purely informational in nature, and therefore there is no point in analyzing this situation in more detail.

Let Us Summarize the General Conclusions

- Bear Put: you bet on a decline, but time often works against you; time is usually on your side.

- Bear Call: you earn if the price does not rise, time usually helps.

- Bull Call: you bet on growth, but theta can eat away the position if the move is too weak.

- Bull Put: you earn if it does not fall, time is usually on your side.

Thus, if the market is in a balance phase, it is more profitable to work with a bear call or a bull put, but if a non-aggressive directional move is expected, then a bull call or a bear put are better suited.

Trading vertical spreads limits both profit and loss, which means it allows you to forecast profitability.

Vertical spreads are the basis for more complex options structures, which we will examine in future publications.