Pip Value: What It Is and How to Calculate It

Success in financial markets is determined not so much by the ability to forecast the direction of price as by the ability to manage risks properly. This management is based, among other things, on a clear understanding of the monetary value of one point (pip) or one tick. Without knowing how much money each minimum price movement will bring or take away, it is impossible to calculate the correct position size, and therefore impossible to protect the deposit from uncontrolled losses.

In this material, we will systematically examine how pip value is calculated for key classes of instruments: currency pairs, CFDs on metals, commodities, stocks and cryptocurrencies, and also find out how to build disciplined risk management through the pip value parameter.

What a Pip Is in Simple Terms

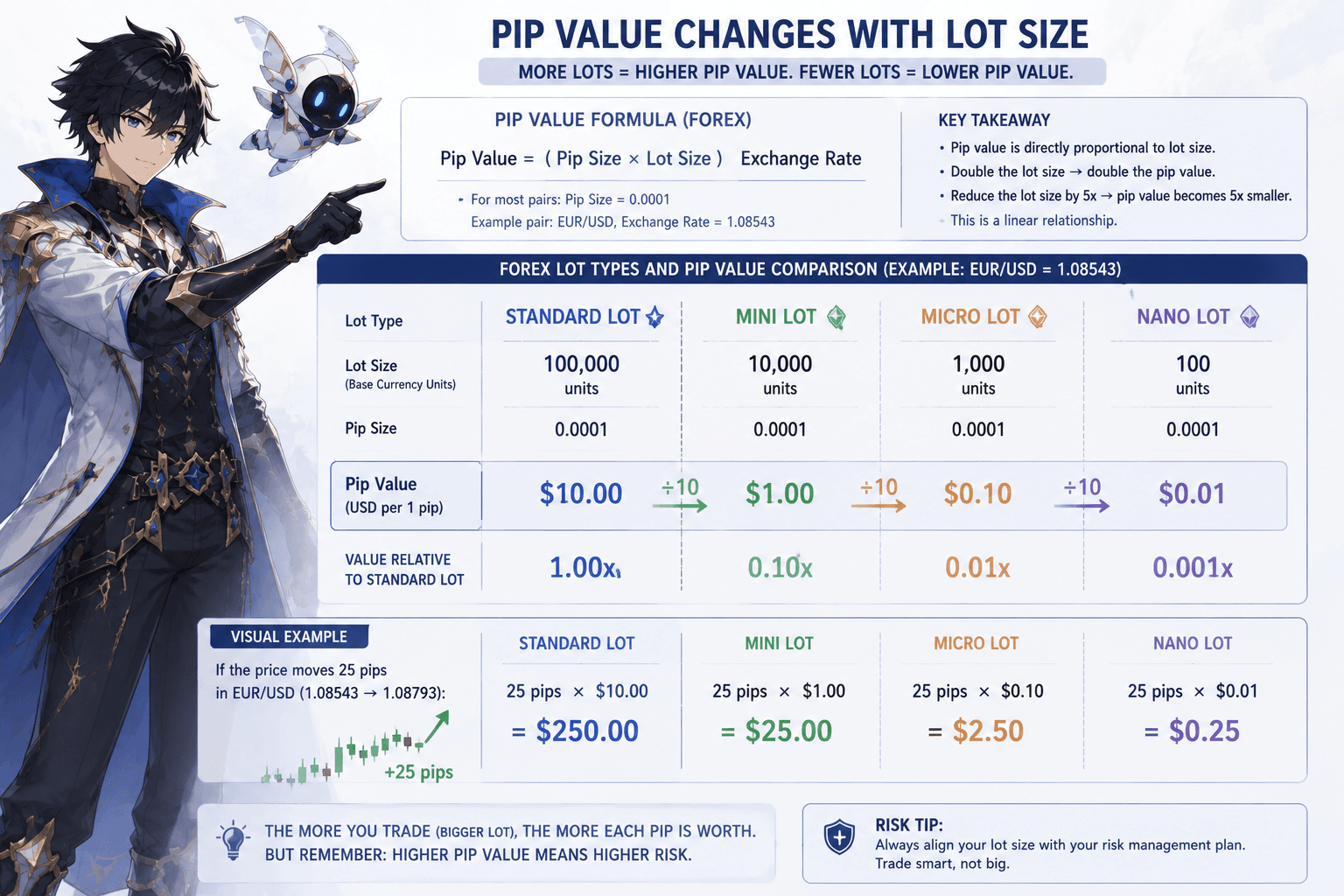

Trading is work with volume. Profit or loss is formed not by the very fact of price movement, but by multiplying the number of points passed by the price of that point, and the point price is directly determined by the lot size - the quantity of the base asset you are trading. Increase the lot twofold, and the pip value also doubles. Reduce it fivefold, and the pip price falls five times. This is a linear relationship, and it must be kept in mind in every trade.

In the Forex market, the basic standard lot is equal to 100,000 units of the base currency. A mini-lot is 10,000 units, and a micro-lot is 1,000 units. In CFDs on other assets, the lot is often tied to a certain number of units of the commodity - for example, 100 troy ounces of gold, 1,000 barrels of oil, or a specific number of shares. It is the contract specification that dictates how much the minimum price change costs. Let us analyze the calculation principles for each class of instruments.

Forex and CFDs: Three Types of Pip Value Calculation

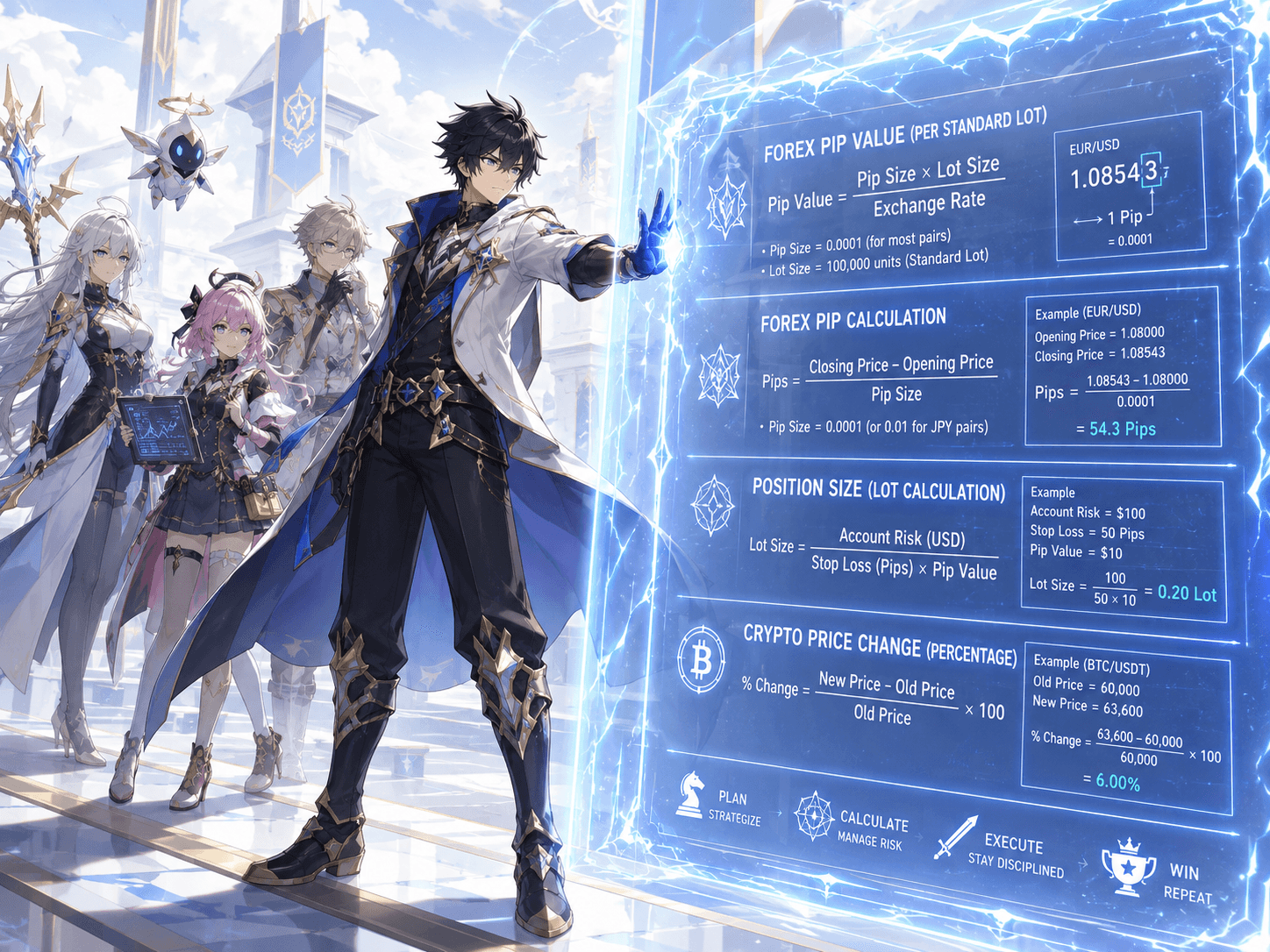

In the currency market, a point (pip) is traditionally the fourth decimal place for most pairs; the exception is pairs with the Japanese yen, where the pip is the second digit. Pip value depends on what position the US dollar occupies in the quote.

Dollar in the Quote Currency (EUR/USD, GBP/USD, AUD/USD)

Here the result of the movement is immediately expressed in dollars. The formula is simple: pip value = volume in units of the base currency × pip size. For one standard lot, this is 100,000 × 0.0001 = 10 USD. Accordingly:

0.1 lot → 1 USD per pip,

0.01 lot → 0.10 USD,

2 lots → 20 USD.

Any change in volume proportionally changes the pip value. If you increase a position from 0.5 to 1.5 lots, the pip value rises from 5 to 15 USD.

Dollar in the Base Currency (USD/CAD, USD/CHF, USD/JPY)

In this case, the monetary value of a pip is first formed in the quote currency, after which it must be converted into dollars at the current rate. Example: the USD/CAD pair at a rate of 1.3600. For one lot (100,000 USD), a movement of 0.0001 gives 10 CAD. Divide by the rate: 10 / 1.3600 ≈ 7.35 USD. If the rate rises to 1.4000, the pip value becomes 10 / 1.4000 ≈ 7.14 USD - it is floating. For USD/JPY at a rate of 151.50 and a pip size of 0.01: 100,000 × 0.01 = 1,000 JPY → 1,000 / 151.50 ≈ 6.60 USD. Increasing the lot by k times will also increase this value by k times.

Cross Rates Without the Dollar (EUR/GBP, GBP/JPY, EUR/AUD)

We receive the result in the quote currency and convert it into USD through the exchange rate of the quote currency against the dollar or through a cross rate. For EUR/GBP with one lot (100,000 EUR), one pip equals 10 GBP. If GBP/USD is trading at 1.2700, the pip value is: 10 × 1.2700 = 12.70 USD. Here, too, there is a direct dependence on volume: at 0.2 lot, the pip value will be 20% of this amount - 2.54 USD.

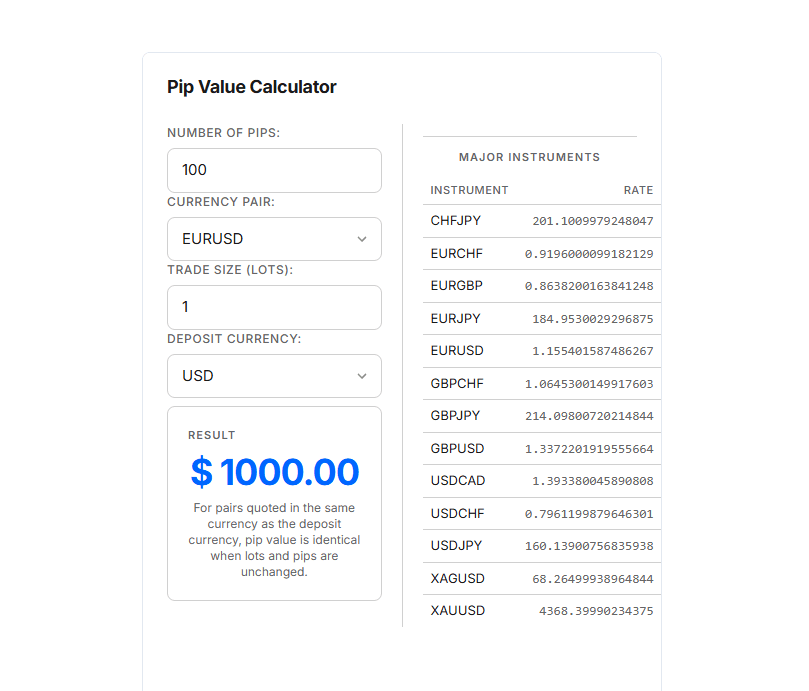

To calculate the value of one pip depending on the number of lots on different currency instruments, we recommend using the “Pip Value Calculation” calculator.

CFDs on Metals, Commodities, Stocks and Cryptocurrencies: Contract Specification Decides Everything

If in Forex the underlying asset is a currency, then in CFDs it is a specific physical or digital commodity. Therefore, pip value is calculated from the number of commodity units in one lot and the tick size (minimum price change). The general formula for calculating pip value is as follows:

CFD on gold (XAU/USD). A standard CFD contract is usually equal to 100 troy ounces. The tick step is often 0.01 USD. Then the value of one tick = 100 × 0.01 = 1 USD. If the broker uses a point as a 1 USD movement (i.e. 100 ticks), then 1 point costs 100 USD. Take the exact figures from the specification. By increasing the lot to 3 contracts, you get three times the value of each minimum change.

CFD on silver (XAG/USD). The lot is 5,000 ounces. With a tick of 0.001 USD, the tick value = 5,000 × 0.001 = 5 USD. Again, linearity: half a lot (0.5) is 2.5 USD per tick.

CFD on stocks. Here the lot is most often equivalent to one share. Suppose you buy a CFD on Apple with a price step of 0.01 USD. The pip (tick) value for 1 lot = 0.01 USD. If the position is assembled from 500 lots (shares), then each cent of movement brings 5 USD. Be careful: in the specifications of some brokers, the minimum lot may be equal to 100 shares - always check.

CFD on cryptocurrencies (BTC/USD, ETH/USD). Usually a lot corresponds to 1 coin. With bitcoin priced around 70,000 USD, the tick is often set as 1 USD. Then 1 lot × 1 USD = 1 USD per tick. If the price moves 2,000 USD in a day, a position of 3 lots will give a valuation change of 6,000 USD. For Ethereum, the tick may be 0.01 USD, and then 10 lots (coins) give a tick value of 0.10 USD. The dependence on volume is just as strictly proportional.

CFD on WTI/Brent oil. The lot is 1,000 barrels. The tick is usually 0.01 USD. Tick value = 1,000 × 0.01 = 10 USD. For a trade with a volume of 0.3 lot, the tick price will be 3 USD.

Stock and Derivatives Markets

Stock Market

The stock market operates with ticks, whose size is set by the exchange. For most U.S. stocks, the tick is 0.01 USD (one cent). The tick value for one share, accordingly, is 0.01 USD. If a position consists of 500 shares, every cent of price movement gives 5 USD. With Apple stock priced around 200 USD and a daily range of 3–4 USD, a position of 500 shares may bring a valuation change of 1,500–2,000 USD.

For stocks priced below 1 USD (so-called penny stocks), the tick is often reduced to 0.0001 USD, which must be checked in the specification of the specific instrument.

When trading on the Russian market, stocks are quoted in rubles, and the tick also varies: for expensive securities, 0.5 or 1 ruble; for cheaper ones, 0.001 ruble. The mechanics remain unchanged: tick value = number of shares × tick size. By increasing a position from 100 to 1,000 shares, you increase the price of every minimum movement tenfold.

Point value calculators for stocks are useful primarily for bringing risk into the single deposit currency and quickly calculating the allowable volume for a given stop-loss.

Futures Market

Commodity, index, and currency futures are traded on exchanges (CME, MOEX) according to strict specifications that fix the contract size and tick value. This is the most structured market from the calculation point of view.

Oil (CL, BRN). The WTI futures contract (CME) equals 1,000 barrels, and the tick is 0.01 USD per barrel. Tick value = 1,000 × 0.01 = 10 USD. The Brent futures contract (ICE) is also 1,000 barrels and the tick is 0.01 USD, but in some contracts the minimum increment may be 0.5 USD, giving 500 USD per tick. A trader must check the exchange specification.

Gold (GC). The CME futures contract equals 100 troy ounces, and the tick is 0.10 USD. Tick value = 100 × 0.10 = 10 USD. A price movement of 1 USD (10 ticks) gives a result of 100 USD.

Index futures (ES, NQ). E-mini S&P 500 has a contract size of 50 USD × the index value, and the tick is 0.25 point. Tick value = 50 × 0.25 = 12.50 USD. For NQ (Nasdaq-100), the contract size is 20 USD × the index, the tick is 0.25, and the tick value = 5 USD.

RTS Index and other MOEX futures. The RTS Index futures contract has a specification where the tick value is tied to the dollar-to-ruble exchange rate, adding a layer of currency conversion similar to crypto crosses. A trader must take this factor into account when calculating risks in ruble equivalent.

In the futures market, tick value is strictly fixed by the specification and does not change with fluctuations in the price of the underlying asset (except for currency futures, where fixation may be in one currency while the account is in another). When trading futures, you know exactly the price of every tick for one contract, and it remains unchanged.

Crypto Exchanges

Cryptocurrency Spot

In the cryptocurrency spot market, the base asset is the coin itself (BTC, ETH, SOL), while the quote currency is the U.S. dollar, a stablecoin (for example, USDT), or another cryptocurrency. Point value here directly depends on two factors: the number of coins in the position and the size of the minimum price change. For dollar-quoted instruments (BTC/USD), the standard tick size is often 1 USD; for lower-priced altcoins, it is 0.01 or 0.0001 USD.

The calculation formula is simple: tick value = number of coins × tick size. If you hold a 0.5 BTC position with a 1 USDT tick, every minimum movement brings or takes away 0.5 USDT. With a daily bitcoin movement of 2,000 USDT, a 0.5 BTC position will give a valuation change of 1,000 USDT. A direct linear relationship: you double the volume, and the tick value doubles too.

Cross pairs without a peg to the dollar or a stablecoin, for example ETH/BTC, are arranged much more complexly.

Here the result of the movement is first expressed in the quoted coin (BTC), and then recalculated into dollars at the current BTC/USD rate. This creates a floating point value: even if the price of the ETH/BTC pair itself stays in place, a change in bitcoin's rate against the dollar or USDT changes the dollar valuation of every tick. For example, a position of 10 ETH on the ETH/BTC pair with a tick of 0.00001 BTC gives a movement of 0.0001 BTC. At a BTC/USD rate of 70,000 this equals 7 USD, and with a fall to 60,000, only 6 USD. A trader must account for this double layer of volatility when calculating risks.

Cryptocurrency Futures

Cryptocurrency futures (both on CME and on centralized exchanges such as Binance Futures) add extra specifics through standardized contracts.

The BTC futures contract on CME has a contract size of 5 BTC, and the minimum price change (tick) is 5 USD per bitcoin. The value of one tick for the full contract: 5 BTC × 5 USD = 25 USD.

On Binance Futures, perpetual contracts (perpetuals) are popular, where the contract size usually equals 1 coin, and the tick is 0.1 or 0.01 USD. An ETH futures contract with a 0.01 USD tick gives a tick value of 0.01 USD with a position of 1 contract. It is important to remember that futures add the effect of leverage, which increases the potential result of price movement but does not change the nominal tick value; it remains tied to the contract specification.

Let's examine the situation with cryptocurrency perpetual futures on Bybit in more detail using ETH as an example.

On Bybit, two main types of Ethereum futures are traded: linear (ETHUSDT) and inverse (ETHUSD). The value of the minimum price change (tick) depends on the contract specification, and the real value of a “point” for your position also depends on the number of contracts.

Linear ETHUSDT Futures Contract (Settlement in USDT)

Contract size: 1 ETH.

Minimum tick: 0.01 USDT.

Tick value for 1 contract: 1 ETH × 0.01 USDT = 0.01 USDT.

Thus, if you bought 1 ETH perp long, every price movement of 0.01 USDT brings or takes away 1 cent.

A price movement of 1 full dollar (100 ticks of 0.01) gives the result: 100 × 0.01 USDT = 1 USDT.

With a volume of 10 ETH (10 contracts), the tick value = 0.1 USDT, and each dollar of movement brings 10 USDT.

The minimum allowed volume is 0.01 ETH, i.e., you can open a position with a tick price of 0.0001 USDT.

Inverse ETHUSD futures (settlement in ETH)

Contract size: 1 USDT.

Minimum tick: 0.05 USDT.

Tick value in USDT for 1 contract: 0.05 USD.

Tick value in ETH: 0.05 / Current ETH price.

At an ETH price = 3500 USD, the tick value is 0.05 / 3500 ≈ 0.00001429 ETH per contract. The higher the ETH price, the less ETH you receive per tick. As the number of contracts increases (for example, 1000 contracts = 1000 USDT), the tick value in USD becomes 50 USD (1000 × 0.05), and in ETH it is 0.01429 ETH.

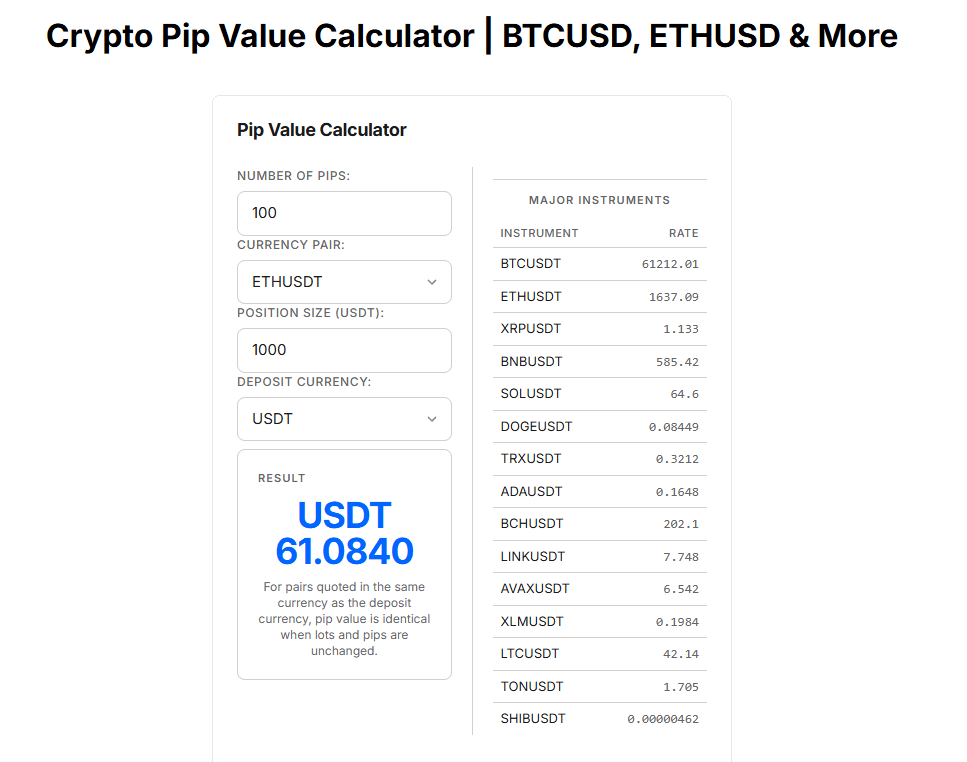

To quickly calculate the point value of a cryptocurrency, we recommend using the "Crypto point calculation" calculator.

Practical Risk Management: Capital Formula and Two Strategic Vectors

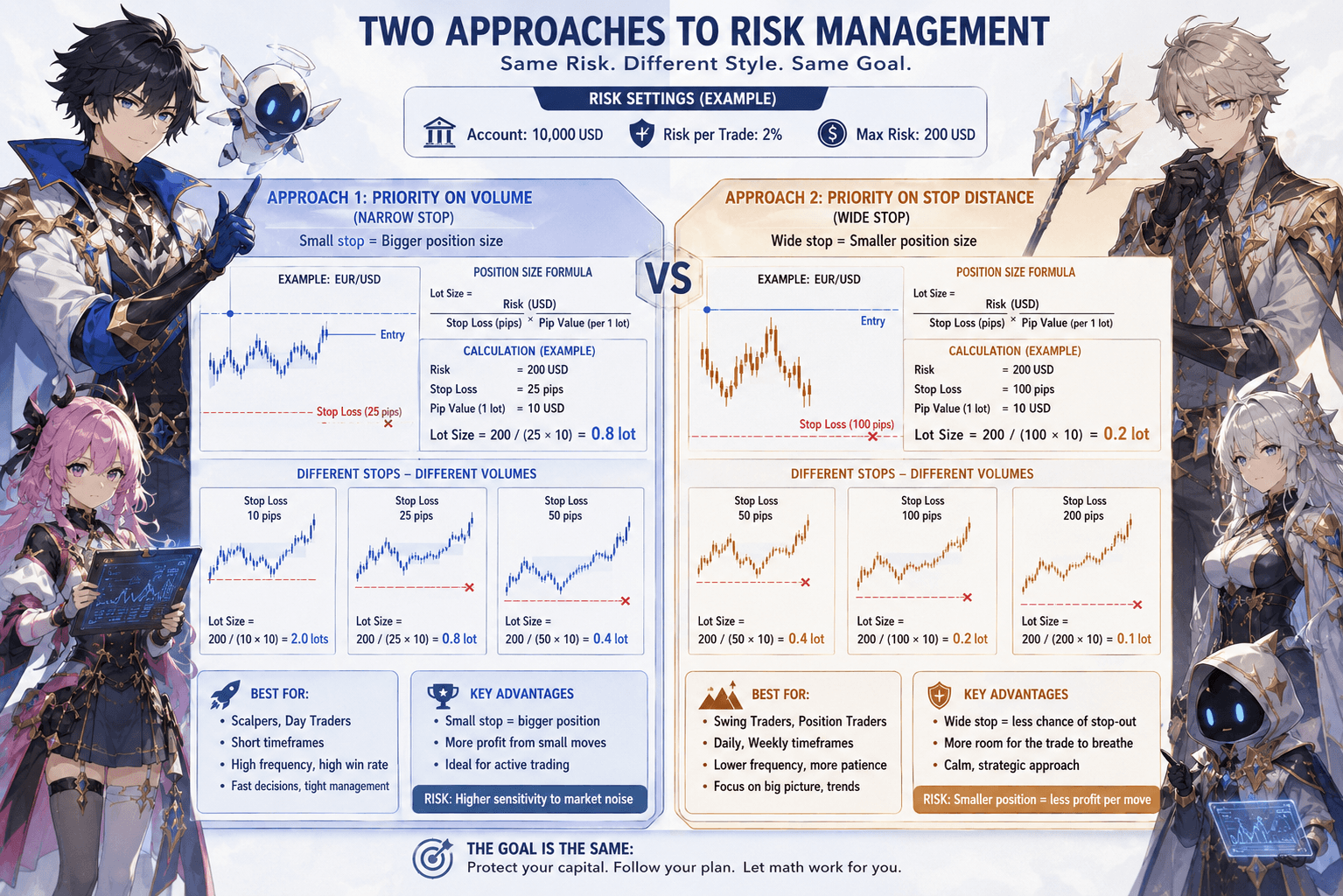

Understanding point value is only half the work. A disciplined trader operates with a fixed percentage of risk per trade, usually 1-2% of trading capital. Suppose the deposit is 10,000 USD, the allowable risk is 2% = 200 USD. In each trade, we can lose no more than 200 dollars. The stop-loss is set in points (ticks) based on technical analysis.

Knowing the point value for one standard lot, we calculate the working volume:

Example: EUR/USD, stop-loss 25 points, risk 200 USD. Point value for 1 lot is 10 USD. Volume = 200 / (25 × 10) = 200 / 250 = 0.8 lot. If the stop were 50 points, the volume would fall to 0.4 lot. If the stop is 10 points, we could take 2 lots. This is the fundamental relationship: the wider the stop, the smaller the volume, and vice versa.

From this arise two styles of working with risk, and the choice between them depends on the trader's psychotype and time horizon.

First Approach: Volume Priority (Narrow Stop)

The trader seeks an accurate entry, using short time intervals, reactions to levels, the order book, or news. The stop-loss is strict, often 5-15 points (or ticks). Since the risk per trade is fixed, a small stop allows opening a significantly larger volume and extracting substantial profit even from a small price movement.

This style is typical of scalpers and active intraday traders. It requires lightning-fast reaction, high concentration, and discipline to immediately lock in a loss, because one unsuccessful entry due to slippage can eat up a noticeable part of the permitted risk. It suits those who can continuously monitor the market and are ready for frequent trades with a high win rate.

Second Approach: Priority of Distance to Stop (Wide Stop)

The trader proceeds from the idea that market noise can knock out protective orders that are too close. He places the stop-loss beyond significant support/resistance levels, which often requires 50, 100, or more points. To fit within the same 2% risk, the position volume has to be reduced.

This style is characteristic of swing traders and position investors working on daily and weekly charts. Advantages: more room to maneuver, fewer false triggers, a calmer pace of decision-making. The drawback is lower profitability for each point of movement, compensated by holding the trend for a long time. It suits balanced traders who cannot or do not want to sit in front of a monitor all day and prefer to analyze the global picture.

There is no universal recipe: an extremely wide stop with microscopic volume gives almost no tangible profit unless the trend lasts for months; an ultra-narrow stop with huge leverage is fraught with a series of stop-outs due to natural volatility. The optimal balance is the one in which you maintain psychological comfort and observe the mathematics of risk.

Conclusion

Point value is not an abstract technical detail, but a measuring tool of your trading system. It changes in direct proportion to the lot and is determined by the specification of the specific instrument: on EUR/USD one standard lot always gives 10 USD per point, on gold the point price depends on the contractual volume of ounces, and on stocks it depends on the number of shares in the lot.

By applying the fixed risk percentage rule, you link allowable losses, stop-loss, and point value into a single formula that automatically determines a safe position volume. As a result, you stop guessing whether it is "a lot or a little" and start trading consciously, adapting the volume to the asset's volatility and the distance to the stop. This is exactly what turns trading from gambling into professional activity with a calculated edge.