Is everything really so good on the stock exchange?

"Once I make some cash on Forex, I'll move to stocks!", "Your Forex is a scam, cluck-cluck, civilized markets are a whole different story, there is no risk of fraud there!", "There is no leverage on the stock exchange, so it is impossible to lose there!".... and similar cries can periodically be seen in the comments under posts in our VK group.

"Once I make some cash on Forex, I'll move to stocks!", "Your Forex is a scam, cluck-cluck, civilized markets are a whole different story, there is no risk of fraud there!", "There is no leverage on the stock exchange, so it is impossible to lose there!".... and similar cries can periodically be seen in the comments under posts in our VK group.

But for some reason the "trading elite" forget that all the books that talk about 90% of losing traders were written... (drumroll) ... about the stock market. Something does not add up here, don't you think?

"How can that be, it is impossible to lose on stocks!!! Unicorns run there and there is a rainbow in the sky!! You dealing-center shills were all paid off!" I can already see comments like that under this article))

In today's article you will learn whether it is easy to make money on the stock exchange, what risks and drawbacks exist there, whether there are ways to manipulate prices there, and we will also sort out the most popular myths about the stock and derivatives markets.

Where did the myths about the stock market come from?

As a rule, money is lost for a standard set of reasons stemming from a trader's lack of readiness to work in the financial and commodity markets. Besides knowledge, this requires a psychological transformation of personality. However, brokers, whose earnings depend on clients paying commissions for every opened trading order, begin to convince the client that the choice was wrong:

- Strategy

- Instrument

- Market

The last argument is an echo of the struggle between brokers for the client. Each company specializes in one particular market, for example stocks or derivatives (futures and options), because of separate licensing. The Forex market stands apart on this list: firms offering currency speculators trading services in currency pairs and CFD contracts can open a business under a simplified scheme using offshore registration.

Forex is decentralized, unlike the stock, commodity, and derivatives markets tied to specific exchanges. These venues have strict state regulation and impose higher, and therefore more costly, requirements on brokers. The most expensive thing is a license to trade securities, and by a "strange" coincidence it is the stock market that is considered "the most profitable for traders, where it is impossible to lose money".

The stock market: grail or slavery?

To understand how the stock market and brokers work, it is enough for a trader to read the book "Reminiscences of a Stock Operator." The confession of Jesse Livermore described in it made him famous, and his trading results put him in the unofficial first place among stock traders.

Despite the recognized value of the tactical and psychological advice placed on the pages of this book, one should always remember the tragic fate of the author. Along his path there were many cases when Livermore went broke and, in the end, another loss of funds in stock speculation drove him to suicide.

Ruin is the traditional end of any stock speculator. The reason is the specific nature of selling and the trends of the securities market. Shares for sale are borrowed from one's broker, for which loan interest is charged to the client, while the client is limited by the list of instruments available for shorting. Will the broker hand over securities that will bring him a loss from the sale?

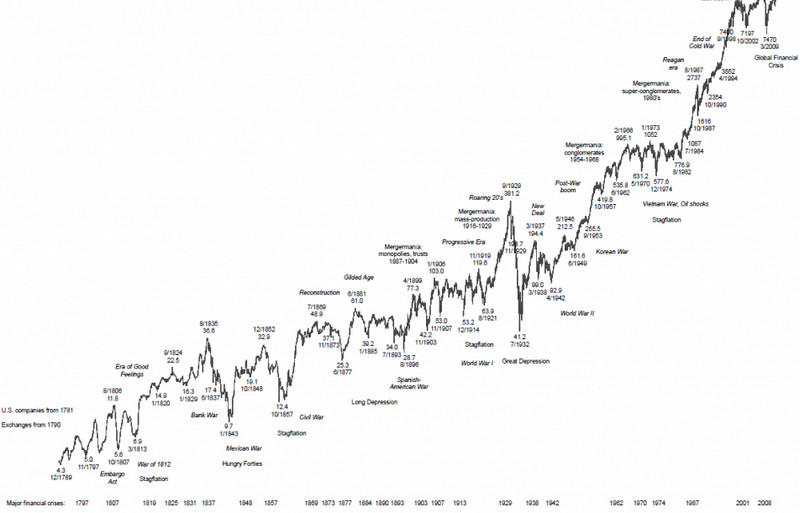

As for the trend, company shares have a greater tendency to rise than to fall. See for yourself by opening a chart of indices. Pay attention to the oldest indicator, the Dow Jones, which has gone through many crises over 240 years:

Therefore, speculative sales bring losses. Stock brokers usually say that the principle of the grail that allows you never to lose money lies in the "Buy and Hold" strategy. The trader must constantly buy additional securities, increasing investment amounts on market declines.

Therefore, speculative sales bring losses. Stock brokers usually say that the principle of the grail that allows you never to lose money lies in the "Buy and Hold" strategy. The trader must constantly buy additional securities, increasing investment amounts on market declines.

Translated into the language of money management, companies are calling for averaging down a position in stocks and for martingale. Forex traders know that both methods are not recommended for use in trading; every trend pullback leads to multiplied losses after a new investment. To incline the client toward this tactic, the broker shows a chart with a clear upward trend in stock indices reflecting the growth of shares and tells stories of Warren Buffett's fabulous wealth.

The company's interest is understandable: shares bring the highest percentage of commissions. Besides paying margin for the trade, the client pays monthly for maintaining a loan account and for depository services. When trying to withdraw profit, a "tax deposit" will be withheld from the funds, and an amount of "minimum balance" will be blocked in the account, which the broker will use free of charge until the end of the tax period.

To dispel the myth of the "buying grail," let us take a "conditional investor" who invested in shares 10 years ago in the highly liquid S&P 500 index consisting of "blue-chip" flagships of American business.

The chart shows that buying securities in 2008 turned into a loss. The initial value of the investment came back only after five years of waiting. Throughout that period the investor would have had to live on hope, though he would have earned money if he had kept adding funds. In that case, the five-year wait would have turned into a period of being tested by losses, funds would have periodically melted away, and losses would have grown.

A ten-year investment period means six years of flat trading, when the investor sat and waited for new highs so that the account balance would become positive again, that is, for 60% of the long-term period there could be no talk of taking profit.

A ten-year investment period means six years of flat trading, when the investor sat and waited for new highs so that the account balance would become positive again, that is, for 60% of the long-term period there could be no talk of taking profit.

It would seem that waiting pays off with profit: over 10 years the total return amounted to 80%. However, from this amount one must subtract 20% inflation (Fed statistics) and 30% for maintaining the loan account and depository services, as well as taxes (personal income tax 13%). The net income over such a long period would have been 1.7% per year.

The example examined the result of an investment in one of the most profitable indices. An attempt to invest in the stock market of the UK or Japan would have resulted in losses, taking into account commission costs and inflation. The situation on the exchanges of developing countries is even more deplorable.

Buffett's proof

Every beginner entering the stock market believes that he will be able to make money there by picking the most profitable and fastest-growing shares. Thanks to the mass media, each of us knows about the rise of Tesla shares, the very profitable growth of Facebook stock, the constant trend in Visa or Mastercard, and so on.

Warren Buffett dispelled this myth through a public dispute with Protégé Partners, offering them a bet that any professional hedge fund managers chosen by his opponents would not be able to show returns above the S&P 500 over 10 years. In 2017, when the term expired, the disputants handed the great investor the lost $1 million. The five hedge funds chosen by the opponents as the "best of the best" managed to earn only 22% in 10 years, while the S&P 500 showed 80%.

The conclusion is simple: no trader makes money in the stock market if inflation and the costs of commissions and taxes are subtracted from the income amount. Proven by Warren Buffett, who is ready to argue about this again with anyone who wishes.

Why is Warren Buffett confident in his victory? The answer is simple: the great investor managed to earn 99% of his huge fortune after the age of 50, having spent 35 years studying the market, and even then he still lost 80% of his capital in 2003. He is the only truly lucky investor on the planet trading shares, not a book author who showed super results over a short trading period and then immediately switched to teaching other traders and holding seminars.

Myths about low leverage in futures and options

In futures, traders lose money just as they do in Forex currencies. Contracts are traded at the rate of the underlying asset: a share, index, bond coupon, commodity, or even a currency pair, with limited leverage that usually multiplies profits and losses by 10, 20, or 30 times. On the one hand, this is less than the size of leverage in Forex, which starts from 50 or 100 and goes up to 1000, but this approach is dictated by the volatility of the assets, which exceeds the variability of the exchange rate by 3 to 5 times.

Unlike Forex, where currencies very rarely exceed a twofold surge in volatility, in futures and especially options the risks of a sharp change in the fluctuation range are much higher.

When any price panic or euphoria arises, trading halts will occur, the deposit in futures will be blocked, and the trader will only be able to watch the rate of the underlying asset. If after the exchange reopens a gap does not lead to the ruin of the account, the client will still have to urgently look for funds or close part of the positions because of the increased margin requirements, since the exchange will sharply raise leverage.

Options may be closed even earlier than futures; the change in leverage in these contracts occurs nonlinearly. To guarantee protection from risks, brokers set an unofficial stop-out level at 50%. An options seller must be ready for unexpected closures of part of the contracts and futile disputes with the company about the legitimacy of such actions.

The myth of transparent futures and options trading

The high rate of trader ruin in futures forces companies to invent other ways of luring clients without promising "fail-safe grails." Beginners are told about the transparency of the trading process. Derivative contracts are traded on an exchange where every participant in the order book sees his own pending order and sees its execution in the "Time and Sales" tape.

The problem is that transparency of trading is an obvious pretext for manipulation: the exchange openly leaks information about pending-order levels and order sizes to specially hired companies, market makers. Traders gave them an apt name: puppet masters.

The specifics of their work give them not only an informational advantage about the "map of the market," but also access to large financial resources entrusted to them by many large and small clients.

Clients are also told about government oversight, without being let in on the history of the century-long unsuccessful struggle of state bodies against broker cartel collusion, which is hard to prove and difficult to bring to court. And even when it succeeds, the case still ends with a fine incomparable to the profits from manipulation.

A beginner or professional trading futures gets put onto the assembly line of market makers, a large-scale dealing desk where brokers systematically use the following strategies against clients:

- Painting the tape: a multitude of small-lot trades to create the illusion of activity in the instrument, attracting scalpers to create a trend in the instrument. It is used to generate high demand for the "distribution" of large volumes bought earlier before the market reverses;

- Phantoms in the order book, or "wash transfers": fake pending orders or real prearranged deals aimed at stopping an undesirable trend by "scaring" Sellers or Buyers, who will believe in the reality of counterdeals or opposite demand, take profit, and leave the market;

- Gap: advancing supply or reducing demand so that a price gap appears on the chart, sharply changing the value of the futures contract in one tick;

- Sweeping the book: a preliminary calculation and a sharp dumping of trades at the highest market price, exceeding in volume all nearby pending orders in the order book. The impulse attracts Buyers or Sellers working by a "breakout" strategy, but they become victims of a preplanned dumping of the book in the opposite direction;

- Manipulation of the futures opening price level: placing premarket orders with inflated volume in order to lock in the price of the first trade after the market opens at the desired level;

- Corner: an agreement with partners to transfer dominant volumes in the underlying asset in order to manipulate futures prices;

- Squeeze: the reverse of the operation described above, building a short futures position under conditions of a shortage of the underlying asset in order to satisfy a client's demand for a short position (borrowing shares to sell);

- Controlled flat: trading the asset within certain price boundaries before the expiration of futures or options in order to hold the required contract settlement price level;

- Artificial backwardation or contango: market makers hunt arbitrageurs trading without stops by selling and simultaneously buying futures on the same asset with different expiration dates. The strategy is considered risk-free because the price difference at the start of the contract evens out by expiration;

Unlike the futures and options market, often gathered on one venue, the Forex market is completely decentralized and the exchange rate is formed by fixing information from real trades from many large banks.

The myth that there is no "dealing desk" in futures and options

Clients are convinced that, unlike the Forex market, there are no so-called "dealing desks" among brokers that organize trading inside the company, and that the exchange protects the asset from any manipulation because it is accountable to state regulators. Therefore, trends are supposedly subject to logical fundamental and technical forecasts, governed by logical supply and demand.

This is indeed true: a broker cannot organize a "dealing desk" on its own, which cannot be said about the exchange itself. National trading venues try to offer traders a large list of trading instruments, using data from international trading centers, including the Forex market, to form exchange rates.

Few people pay attention to the fact that under the Agreement the exchange should, but is not obliged to, maintain correspondence with those rates. What does this mean in practice? In particular, on the Moscow Exchange a trader can quite easily, while trading futures on oil, metals, or currencies, get an unexpected jump in the rate by several percent, different from global values.

In Forex practice, such a phenomenon is called a spike, and in 99% of cases a decent broker will return the funds to the affected client. In the case of the Moscow Exchange, this is called "the market," and nobody will return the losses from the difference.

A recent illustration of such behavior was Brent oil trading on December 25, 2018. The venue, using the fact that trading on U.S. exchanges was closed, sharply pushed the oil price down by 11% during a 40-minute trading interval. Thanks to the "price limit" mechanism described in the article above, many positions were closed by margin call or stop-out.

This is not the first case of such a price difference. Earlier, EURUSD futures, palladium contracts, and gold futures had already "run away" from world prices. In all the stories listed above, the Central Bank of Russia investigated, but found no violations or facts of price manipulation.

Conclusion

Trading without leverage in the stock market does not reduce risks. Any attempt at speculation (buying and selling) will ultimately lead to ruin because it is necessary to hold a position long enough to earn money and justify commissions.

The "Buy and Hold" strategy, as well as attempts to entrust funds to professionals, will bring profit only to hedge fund managers, who immediately charge a fee for managing finances. The investor is guaranteed to be left with empty pockets at the moment of the next economic crisis, which occur every 5 to 10 years throughout the three centuries of exchange history.

Trading futures and options on an exchange does not differ from the Forex market if the broker is chosen correctly: the trader will be protected from market makers' lawlessness and from the risks of exchange-rate collapses caused by exchange illiquidity.

Respectfully, Alexey Vergunov TradeLikeaPro.ru