Everything You Need to Know About High-Frequency Trading

Hello, fellow traders!

Hello, fellow traders!

Surely, many of you have heard of such a concept as “high-frequency trading.” High-frequency trading has become a very popular topic over the past decade and has brought significant improvements to the markets. These improvements include reduced volatility, greater market stability, improved transparency, and lower costs for traders and investors.

Today I have prepared a lot of information for you about what high-frequency trading (HFT) actually is, how HFT systems are used in modern financial markets, the various HFT strategies, and the history and development prospects of this area of trading. Let's begin!

Changes in the Markets Over Recent Decades

Let's first look at the history of the development of modern markets to understand the prerequisites for the emergence of HFT. Over the past couple of decades, consumer demand for computer technology has led to a significant drop in the price of trading equipment. As a result of advanced technologies and subsequent investment in software, trading platforms have become much more accessible and powerful. In addition, increased terminal resilience, greater reliability in the execution of orders, and the provision of platforms for connectivity and custom software development have led to an ever greater complexity in the trading process.

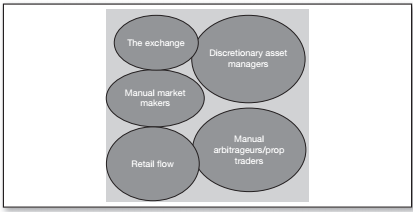

The figure above illustrates the main segments of the financial services market in the 1970s. Here is what the market looks like today:

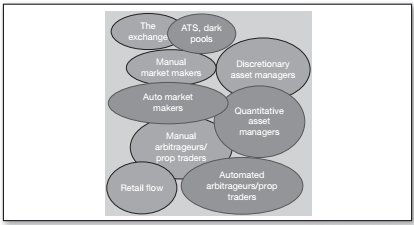

The figure above illustrates the main segments of the financial services market in the 1970s. Here is what the market looks like today:

In the 1970s, the main participants in the financial markets were institutions and large individual players, many of which still hold leading positions today. These were mainly various funds: pension funds, mutual funds, and hedge funds. Private traders, market makers, and various intermediaries also joined them.

In the 1970s, the main participants in the financial markets were institutions and large individual players, many of which still hold leading positions today. These were mainly various funds: pension funds, mutual funds, and hedge funds. Private traders, market makers, and various intermediaries also joined them.

Transaction costs were very high, while securities turnover was quite low. There was also a high probability of errors in order processing, since all orders were handled manually. Most traders in those days relied primarily on their own experience and intuition rather than on technical or fundamental analysis because the calculations were too complex.

Now let's take a look at the markets today. New participants successfully compete with financial tycoons, because these days high technologies, complex mathematical calculations and the construction of accurate models of market processes no longer seem like something fantastic.

The various funds use the latest economic and financial theories, as well as the latest mathematical tools, to make increasingly accurate predictions of price behavior in financial markets, which lead to increasingly efficient trading.Market makers,brokers and hedge funds are exploring the microstructure of markets and emerging technologies in developing automated HFT strategies to ensure low transaction costs while taking significant market share from traditional dealers. Funds dealing statistical arbitrage, also use quantitative algorithms, including high-frequency ones.

Nowadays markets are very democratic. Due to the spread of cheap technology, anyone can trade on real markets, place orders and thereby participate in the formation of the price of an asset, which was previously strictly the privilege of dealers. With all this automation of the trading process virtually eliminates the possibility of errors when executing trading operations. Strong competition between new entrants and old players has also led to a decline marginal requirements from brokers.

Here's how the trading process happened in the 70s:

- Brokers call their clients, offering their ideas on buying or selling particular securities;

- If the client can be persuaded, he places a verbal trading order directly over the phone. Brokers sat on the trading floor, and the noise from the pit often interfered with the precise execution of the client's instructions;

- After receiving the instruction, the broker either executes the order, if it is large enough, or waits until a suitable batch of orders with enough volume accumulates, all to be executed at one price. Thus, the smaller the client, the worse the execution prices he receives;

- So, once a sufficient volume of orders has accumulated, the broker executes the trade;

- Next, exchange representatives called “specialists” processed the orders. It is no secret that manipulating prices in orders was common practice, and such people received the lion's share of their remuneration precisely from trade execution;

- The broker notifies the client that the order has been executed and collects commissions and bonuses.

Nowadays, clients are often better informed about market analysis and equipped with more modern equipment than the brokers themselves. The scope of brokers' competence has also narrowed significantly. Here is a modern algorithm for broker-client interactions:

- The client conducts research, develops trading strategies and algorithms;

- The client places an order via an electronic network, which almost instantly reaches the broker’s server;

- The client selects the optimal mechanism for executing his order (pending, market order);

- Information about the order is automatically executed on the corresponding trading platform;

- The trading platform automatically confirms the execution of the client's order;

- The broker automatically sends confirmation to the client that the transaction has been completed and receives a small commission for its services. In 1997, Merrill Lynch's commission for completing a transaction was $70. Today Interactive Brokers charges approximately $0.35.

Steve Swanson was a typical 21-year-old computer geek. It was the summer of 1989, and he had just received a mathematics degree from the College of Charleston. When it came to clothing, he was drawn to T-shirts and flip-flops, and to television, the Star Trek series. He spent most of his time in the garage of Jim Hawkes, a statistics professor at Steve's college. There he programmed algorithms for what would become the world's first high-frequency trading company, called the Automated Trading Desk. Hawkes was obsessed with the idea that he could make a profit in the stock markets by using formulas for predicting price behavior developed by his friend, David Whitcomb, who taught economics at Rutgers University. Swenson's task was to turn Whitcomb's formulas into machine code.

A satellite dish mounted on the roof of Hawkes' garage picked up signals carrying updates.quotes, receiving which, the system could predict the behavior of prices in the markets within the next 30-60 seconds and automatically buy or sell shares. The system was called BORG - short for Brokered Order Routing Gateway, Brokerage Team Routing Gateway. The name also referred to the Star Trek series - or more precisely to an evil alien race capable of absorbing entire species, turning them into parts of a single cybernetic mind.

One of the first victims of BORG were market makers on the floors of the stock exchange, who manually filled out cards with information about buying and selling shares. ATD not only knew better who gave the more attractive price. The new system carried out the process of buying and selling shares in a second. By today's standards, this is a snail's pace, but then no one could surpass it. As soon as the stock price changed, ATD computers began trading on conditions that other market participants had not yet had time to adjust, and a few seconds later ATD sold or re-bought shares at the “correct” price.

ADT averaged less than a penny per share, but the company handled hundreds of millions of shares a day. As a result, the firm was able to move from Hawks' garage to a modern $36 million business center in a swampy suburb of Charleston, South Carolina, about 650 miles from Wall Street.

By 2006, the company was trading approximately 700-800 million shares per day, representing more than 9 percent of the entire U.S. stock market. And it had competitors. A dozen other major electronic trading firms entered the scene: Getco, Knight Capital Group, and Citadel grew out of the trading floors of the Chicago commodities and futures exchanges and the New York stock exchanges. High-frequency trading began to gain momentum.

Major world exchanges

The largest stock exchanges in the world are in a state of fierce competition and are too dependent on the interests of investors who expect constant growth in profits. As a result, exchanges are forced to look for non-standard marketing solutions and ways to stand out among competitors. Let's look at what allows the world's leading exchanges to develop.

Australian Securities Exchange (Australian Securities Exchange—ASX)

The main goal of the Australian Securities Exchange (ASX) is to maintain a dominant position in the Australian securities market. In addition, the ASX is committed to listing securities of companies from Southeast Asia. Low costs and consistently high sales performance make the Australian Securities Exchange competitive in the global financial system.

In 2005, the ASX gave brokers the ability to trade anonymously. The initiative helped to significantly increase liquidity securities - in particular, shares included in the S index&P and ASE, which account for more than three-quarters of the total market value.

Other ASX initiatives include opening a secondary market similar to the London Stock Exchange's Alternative Investment Market (AIM) for companies with a market capitalization below A$100 million (which is two-thirds of the AIM).

German Stock Exchange (Deutsche Börse)

The German Stock Exchange seeks to differentiate itself by creating a unique portfolio of services that covers the entire chain of exchange processes, such as securities and derivatives trading, settlement and closure of transactions, provision of up-to-date market information, development and operation of electronic trading systems. Thanks to its exchange-oriented business model, Deutsche Börse creates an efficient capital market: issuers benefit from low capital costs and investors benefit from high liquidity and low transaction costs.

European stock exchange Euronext

The European stock exchange Euronext (now part of the world's largest exchange NYSE Euronext) was formed as a result of a large-scale merger of the stock exchanges of Amsterdam, Brussels and Paris and subsequently expanded to include the Lisbon stock exchange, LIFFE and the London Financial Derivatives Exchange.

Euronext was created with the aim of dividing spheres of influence in Europe and jointly controlling the three original securities markets. Contrary to the agreements, Paris took the lead in most areas of Euronext's activities. The exchange now uses the original French electronic trading system. In addition, most major French privatizations take place on Euronext.

Euronext is pursuing a strategy of diversification and expansion, adding new products and services and seeking to increase its influence internationally. Euronext analysts have developed a “Technological Improvement Program” similar to the system operating on the London Stock Exchange. The new electronic platform will help Euronext significantly increase the speed and number of simultaneous transactions.

The Hong Kong Stock Exchange (HKEX)

The Hong Kong Stock Exchange (HKEX) is inextricably linked to China's rapidly developing economy. HKEX's main advantages are its geographical proximity to mainland China, relatively lenient corporate governance and the favor of the Chinese government, which is conducting privatizations of state-owned enterprises here.

Chinese companies trust the Hong Kong Stock Exchange and prefer it to Western and American competitors. It is more convenient, cheaper and culturally easier to list securities on the Hong Kong Stock Exchange. Listing standards on HKEX are high, but the requirements for companies are not nearly as stringent as in the United States, as the exchange's management has repeatedly stated.

Currently, only securities of companies registered in Hong Kong, China, Bermuda or the Cayman Islands can be listed on the exchange. However, the Hong Kong Stock Exchange's marketing strategy involves changing the rules to include shares of companies from other countries in the Asia-Pacific region (for example, Australia) and reduce dependence on China.

London Stock Exchange (LSE)

The London Stock Exchange is spending a lot of money on its Technology Road Map, a massive program to modernize its trading mechanisms. One of the latest successful steps in this direction was the introduction of a new system for storing and transmitting market data Infolect, which made it possible to reduce the average speed of a transaction to two milliseconds (which is approximately 15 times less than previously required).

Like Euronext and NASDAQ, the London Stock Exchange is looking to expand its influence around the world. LSE's focus is on China, India and Russia. The strategy of attracting foreign companies to the listing procedure really works - in 2006, several large Russian private enterprises listed their shares on the London Stock Exchange. Management also decided to open an additional office in Hong Kong in October 2004 to compete with US exchanges for Chinese business.

US stock exchange NASDAQ

NASDAQ is the largest electronic stock exchange in the United States based on the number of securities trades closed and the presence of companies that are leaders in their industries - for example, shares of Microsoft, Intel, Google, Oracle, Nokia, K-Swiss, Carlsberg, Starbucks and Staples are traded on this exchange. Despite the fact that NASDAQ initially positioned itself as an “exchange for growing companies,” today it faces some of the most stringent requirements for applicants to be listed on the exchange.

The world's first electronic stock market, NASDAQ strived to become a leader in trading technology. The speed of transactions was reduced to a record low of one millisecond.

New York Stock Exchange (NYSE Euronext)

NYSE Euronext positions itself as the world's leading stock exchange. The most liquid stocks, the highest standards of listing and blue chips (securities of the largest companies with stable income) allow the New York Stock Exchange to maintain its secret gold status.

Like all major stock exchanges around the world, NYSE Euronext is looking to expand its reach beyond the US and overcome the competition of local exchanges that have grown over the past few years in large metropolitan areas (for example, Milan or Mumbai).

In order to gain access to shares of companies located outside the United States, in June 2005 the New York Stock Exchange proposed merging with Euronext, one of the largest securities exchanges in Europe. The merger, approved by Euronext shareholders, took effect in the first quarter of 2007 and for the first time created an “intercontinental” securities market, with the total value of listed companies amounting to approximately 26 trillion dollars.

Singapore Stock Exchange (SGX)

The Singapore Stock Exchange has carved out a niche in the Asian securities market. The largest companies from the countries of the Asia-Pacific region are represented here (except for Japanese, Korean and state-owned Chinese enterprises, which prefer to list their shares for sale on domestic exchanges). SGX is an extremely attractive trading platform for countries that do not have a globally recognized exchange. In addition, the Singapore Stock Exchange has succeeded in attracting private Chinese capital.

In order to maintain its competitive advantage, the Singapore Stock Exchange seeks to cooperate with smaller regional exchanges and thereby expand its global network of trading platforms. In mid-January 2007, SGX became the only Asian exchange to officially announce its desire to acquire a 26% stake in the Bombay Stock Exchange. The other three exchanges competing for Bombay shares, NASDAQ, London Stock Exchange and Deutsche Börse, are based in North America and Europe.

Japan Exchange Group, Inc

The Japan Stock Exchange strives for regional leadership and global competition and positions itself as a "prestigious listing destination." The significant advantages of Japan Exchange are the sale of securities with high liquidity and the introduction of cutting-edge information technologies into the trading process.

The exchange is a member of the Federation of Stock Exchanges of Asia and Oceania. Japan Exchange Group, Inc resulted from the merger of the Tokyo Stock Exchange and the Osaka Stock Exchange in 2012. Before this, the main player in the Japanese stock market was the Tokyo Stock Exchange (it absorbed the Osaka Stock Exchange).

Moscow Exchange

The Moscow Exchange was formed in December 2011 as a result of the merger of two main Russian exchange groups - MICEX and RTS. The exchange structure that emerged as a result of the merger gained the ability to trade in all major categories of assets.

At the moment, the Moscow Stock Exchange is the largest stock exchange in Russia and Eastern Europe. In addition, the share of post-trading services on the Moscow Exchange is increasing, which, according to management, can attract new issuers and investors. Armed with the experience of American competitors, MB began to provide management services risks and provide investors with business information. Trading mechanisms are being modernized, and the speed of transactions on the derivatives market is increasing.

What is high-frequency trading

The term "hft" includes a wide range of operations from algorithmic trading. High-frequency trading is a fairly closed area. It is very difficult to find information about how HFT firms work. However, some information can still be obtained from lists of open vacancies, advertisements and individual Internet articles. HFT is also very different from other forms algorithmic trading. It is based solely on technical solutions and a huge number of calculations. Once trading is launched using a specific algorithm, virtually no adjustments are made to its operation (as long as it remains profitable), which is very different from low-frequency systemic trading, in the process of which people often make their own adjustments.

Working in such an environment is highly competitive and can often break people down. Many months of research become irrelevant overnight if the exchange's operating structure changes, a new legislative framework appears, or if competitors are able to start processing data at higher speeds. Therefore, this type of work is suitable for well-disciplined people with several higher technical educations, able to work under pressure, who value independence and a highly professional team.

Despite the fact that the activities of HFT traders are often criticized, only certain types of HFT trading create chaos in the modern financial market. The line between algorithmic trading, electronic market making and harmful HFT trading is quite blurred, and high-frequency trading often refers to electronic trading. In fact, the phenomenon of HFT trading in itself is neither good nor bad, but the devil is in the details.

To clearly understand the possibilities of HFT trading, it is worth taking a closer look at some types of market activities.

Algorithmic/systemic trading is the general name for the process of using programmable systems that use a specific mathematical model to automatically execute trades. A person creates a program on a computer for a specific financial strategy based on a given criterion and controls the developed system from this computer. HFT trading is a type of algorithmic trading, but not all algorithmic trading can be considered high-frequency.

In 2011, the Commodity Futures Trading Commission (CFTC) admitted that it was not trying to come up with a precise definition of high-frequency trading. Instead, she proposed seven main signs of HFT trading:

- Using systems that implement extremely fast order placement, cancellation and modification in less than 5 milliseconds or with virtually minimal latency;

- The use of computer programs or algorithms to automate the decision-making process, during which the placement, execution, direction and execution of orders are determined by the system and do not require human intervention in the case of each individual order or transaction;

- Use of colocation, direct market access or dedicated data link services offered by exchanges and other organizations to reduce network and other delays;

- Very short time frame for opening and closing a position;

- High daily turnover of the securities portfolio and/or a high proportion of submitted orders in relation to the number of transactions carried out;

- Placing a large number of orders that are canceled immediately or within a few milliseconds;

- Ending the trading day in a position as close to zero as possible (without holding large unhedged positions overnight).

The history of HFT strategies

Many people now complain that high frequency traders who use mathematical algorithms have an unfair advantage over those whose algorithms are not as good, or that their (hft traders) trading systems are faster than other players.

This dissatisfaction underscores a larger historical fact: any technology that increased the speed of information flow was immediately adopted by the trading community in both Europe and the United States. Traders have used every known vehicle to execute trades faster and with less effort. They were among the first to master high-speed boats, faster crews and private couriers.

In the late 1830s, Philadelphia broker William Bridges operated a personal signal station between New York and Philadelphia that relayed stock market news to him and his patrons (and no one else). Signals were transmitted using an "optical telegraph", which consisted of a series of shields on a pole mounted on a hill, which could be seen through a telescope. Reports indicate that they could transmit stock market information anywhere from New York to Philadelphia in 10 to 30 minutes. In the 1830s this was high speed trading.

It is not surprising that complaints began to come from speculators in New York, who were not involved in this system and who had until then enjoyed a significant advantage. When the system was shut down after the advent of the telegraph in 1846, a local newspaper report wrote that “many of the ingenious moves in the Philadelphia stock and commodity markets were responsible for the speculators who contributed to the creation of the telegraph. No doubt the speculators paid its creators well."

It is not surprising that complaints began to come from speculators in New York, who were not involved in this system and who had until then enjoyed a significant advantage. When the system was shut down after the advent of the telegraph in 1846, a local newspaper report wrote that “many of the ingenious moves in the Philadelphia stock and commodity markets were responsible for the speculators who contributed to the creation of the telegraph. No doubt the speculators paid its creators well."

Unfortunately, the organized trading community was not very keen on openness. In its early days, the NYSE (New York Stock Exchange, then known as the New York Stock and Exchange Board) did not allow the public to listen in on trading sessions (sessions were not available to the public until 1869). Competing traders (over-the-counter traders working literally from the outside) who intended to sell trading information on the NYSE were furious that they could not be near the exchange. In 1837, the NYSE discovered that over-the-counter traders had drilled a hole in the brick wall of the exchange building in order to eavesdrop on trading.

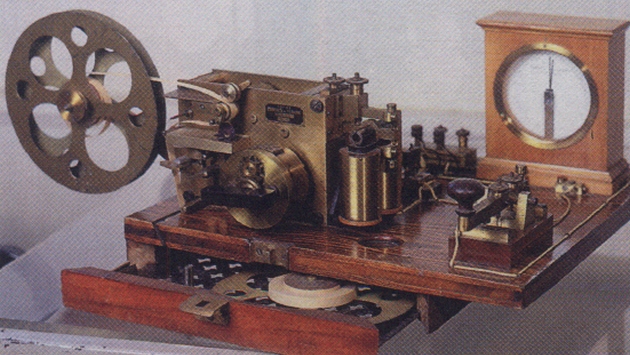

While the public was wondering how to get ahead of the fast horses, a new technology appeared on the scene that turned trading into a truly high-speed area: the telegraph, which came into use after 1844. He was the greatest invention of his time. Newspapers took time to produce and were mostly released at regular intervals. But the telegraph worked constantly, and it could be used for personal communication.

As expected, the use of the telegraph to transmit “secret knowledge” caused outrage. Several inventors of the early telegraphs were forced to stop their experiments by warnings that they might be persecuted for disseminating information faster than mail. The telegraph's leading inventor, Samuel Morse, supported the introduction of the telegraph into mass production for personal and public purposes, particularly to protect it from being used for profiteering purposes.

As expected, the use of the telegraph to transmit “secret knowledge” caused outrage. Several inventors of the early telegraphs were forced to stop their experiments by warnings that they might be persecuted for disseminating information faster than mail. The telegraph's leading inventor, Samuel Morse, supported the introduction of the telegraph into mass production for personal and public purposes, particularly to protect it from being used for profiteering purposes.

Forty years later, the telegraph was still the main tool of stock market speculators. In 1887, the president of Western Union stated that 87% of the company's income came from speculators in the stock and commodity markets and those who made money from horse racing.

Introduced in 1867, the stock ticker became the next great electronic device and was immediately adopted by the trading community. Before its appearance, stock exchange transactions, as a rule, were carried out with the help of “runners” - boys who ran from the stock exchange pit to brokerage houses. It was hugely superior to the telegraph for several reasons: traders no longer needed to be physically present in the trading pit, its introduction reduced transaction costs, it helped disseminate information continuously in real time, and its invention eliminated the number of pesky middlemen like telegraph companies and newspaper editors. Not surprisingly, journalists and editors became concerned that the introduction of the ticker would force them out of the lucrative trading of financial news.

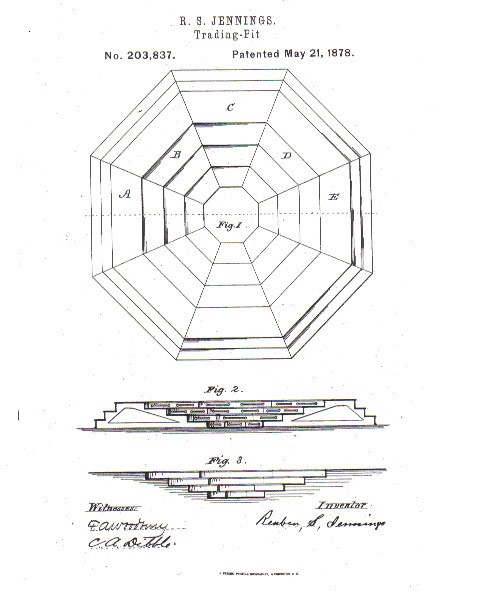

The first stock pit was patented by Reuben S. Jennings in 1878. He designed the pit in such a way that traders could see and hear other traders in the best possible way. Therefore, there were several steps in the pit. The trader at the very top had the best visibility and the advantage of being able to easily see and hear his colleagues, all of which allowed him to execute trades faster.

To gain a speed advantage, one had to be physically taller than other traders, so height began to play an important role in reducing delays. That’s why former basketball players often became traders: it was easier to notice them. Already at the end of the twentieth century, some pit traders wore high heels to stand taller and execute trades faster.

To gain a speed advantage, one had to be physically taller than other traders, so height began to play an important role in reducing delays. That’s why former basketball players often became traders: it was easier to notice them. Already at the end of the twentieth century, some pit traders wore high heels to stand taller and execute trades faster.

This has led, for example, to falls due to lack of balance when walking in high heels. As a result, the Chicago Exchange was even forced in November 2000 to decide to set a maximum heel and/or platform height of two inches (just over 5 centimeters), and, for example, the London Metal Exchange still has a rule according to which transactions can only be concluded while sitting.

Introducing such standards was one way to level the playing field in terms of speed on the trading floor, but in the end there was always someone who would beat the competition. Those traders who were most successful in reducing trading delays profited from the inefficiencies of the then existing system, in which growth could provide a big advantage, for example.

As a result of their work, these inefficiencies were gradually leveled out - somewhere by the introduction of regulatory rules, somewhere by the very course of history - for example, the computerization of exchanges itself made the desire to be physically superior to everyone else simply irrelevant.

This continued with the invention of the telephone (first tested by Bell in 1876, by 1878 the NYSE already had its own telephone), with the creation of pneumatic mail, the computer in the 1950s, punch cards in the 1960s, the first advent of electronic trading when the Nasdaq exchange began operating in 1971, and algorithmic trading in the 1990s. The same disputes arose: someone received information before others, and some could trade because they had a faster ship, horse, carriage, telegraph line, computer communication, algorithm.

In 1967 Edward Thorpe, a professor of mathematics, published the book “Beating the World.” The author described a method by which one could make money in the stock markets. The system he invented was so good that some trading houses had to change their trading rules.

Later in Britain, the developments of mathematicians brought new methods of analysis and the belief that in the future computer systems could make a real revolution in predicting market fluctuations. Then a completely new branch of science was born - quantitative analysis.

In 1989, with the advent of newer technologies and computer systems, the idea of high-frequency trading was born as a method of using high-performance systems to make money on trading exchanges. The author of this idea is Steve Swanson.

He worked on analyzing the movement of quotes on stock exchanges 30 seconds before a transaction. At the same time, he and his partners David Whitcomb and Jim Hawkes founded the first and only automated trading company at that time - AutomatedTradingDesk. While all financial market participants worked via telephone, the order processing speed through AutomatedTradingDesk was one second. This is how the history of HFT began. As a result, 70% of trades on Wall Street these days are carried out by high-frequency algorithms.

Today, trading is typically carried out using electronic servers in data centers, where computers exchange offers to buy and sell by transmitting messages over a network. This shift from back-office trading to electronic platforms has been particularly beneficial for HFT companies, which have invested heavily in the infrastructure required for trading.

Even though the place and participants in trading have changed a lot in appearance, the goal of traders, both electronic and traditional, has remained the same - to purchase an asset from one business or trader and sell it to another business or trader at a higher price. The main difference between a traditional trader and an HFT trader is that the latter can trade faster and more often, and the portfolio holding time of such a trader is very low. One operation of the standard HFT algorithm takes a millisecond, which traditional traders cannot match, since just blinking in humans takes approximately 300 milliseconds.

Hft as an evolution of classical trading

Brokers who were vocal against HFT tended to rely on technical analysis when deciding when to enter or exit a position. Technical analysis was one of the earliest methods to become popular with many traders and in many ways it is a direct predecessor to modern econometrics and other HFT methods.

Technical analysts, who came into vogue in the early 1910s, sought to identify recurring patterns in prices. Many techniques used in technical analysis measure current price levels relative to moving average prices or combinations of moving averages and standard deviation of prices (Bollinger Bands).

For example, a technical analysis indicator such as MACD, uses three exponential moving averages to generate trading signals. Advanced technical analysts look at prices in conjunction with current market events or market conditions to get a better idea of where prices might be headed next.

Technical analysis flourished in the first half of the 20th century, when trading technology was in its infancy and the complexity of trading strategies was much lower than it is today. The speed of dissemination of information and quotes, among other things, was amazingly low. The previous day's trades did not appear in the newspaper until the next morning. In the post-war years, technical analysis became a self-fulfilling prophecy.

If, for example, enough people believed that the figure "head and shoulders", a huge number of traders began to place sell orders, realizing the prediction in this way. Currently, classical technical analysis works well only on timeframes from D1 and above. And yet, many technical analysis methods and indicators are used by quants to build high-frequency trading strategies.

Scientifically proven that investors tend to trust more strategies that have worked in the past. It also follows common sense that what worked before will probably continue to work. As a result, vehicles operating last month are also likely to operate next month, forming a trade trend, which can be detected using simple technical indicators based on a moving average, as well as more complex quantitative tools. Quite often, quants use the Bollinger Band indicator in their strategies to track the current market conditions.

Another type of analysis, Fundamental Analysis, originated in the stock market in the 1930s. Traders have noticed that future cash flows, such as dividends, influence market price levels. Graham and Dodd (1934) were the earliest traders to use this approach, which remains popular to this day. Fundamental analysis developed throughout most of the 20th century. In equity markets, fair prices are still often determined based on forecasts of companies' future earnings.

On the market forex The most common are macroeconomic models, which calculate fair prices based on information about inflation, trade balances of various countries and other economic indicators. Derivatives are traded primarily through advanced econometric models that incorporate statistical properties of the price movements of the underlying instruments. Various aspects of the application of fundamental analysis are also used in the construction of HFT systems. The date and time of news release are usually known in advance, and the information necessary for making a decision is disclosed during the announcement of the news.

It is absolutely clear that in such a situation, the systems that respond most quickly to changes receive the maximum profit. In fact, speed has become the most obvious aspect of competition. To speed up the process of executing transactions, traders began to use more and more powerful computers and use more and more advanced technologies.

Modern period

By 2012, there was a trend towards a decrease in the efficiency of HFT and its market share. Since 2009, in just three years, the volume of profits from high-frequency trading has decreased 5 times from $5 billion to $1.25 billion. In 2014, the book “Flash Boys: The High-Frequency Revolution on Wall Street” was published, detailing the history and mechanisms of HFT as financial fraud and market development. The product became a bestseller, its author is Michael Lewis. In 2016, due to low volatility, most of the smaller HFT companies began to leave the market. Their profits have become incomparable to what they were in 2009-2010.

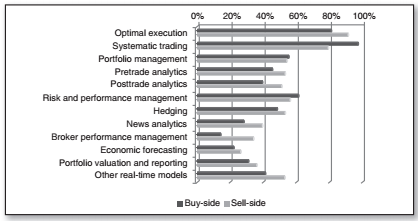

For the successful implementation of the HFT system, signal-generating algorithms, algorithms that optimize order execution, risk management algorithms, and optimization are required.portfolios and so on. The figure below illustrates a survey of traders conducted by Automated Trader in 2012. Here's how traders responded about the purposes for which they use automated trading systems:

HFT systems cover almost the entire range of decisions a trader makes, from selecting trading instruments to achieving the best possible execution of orders.

HFT systems cover almost the entire range of decisions a trader makes, from selecting trading instruments to achieving the best possible execution of orders.

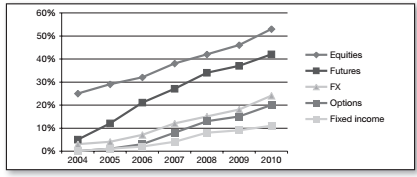

And yet, even today, not all markets are suitable for high-frequency trading. According to researchb conducted by Aite Group, equity markets have the largest percentage of algorithmic participants, who account for more than 50% of trading volumes. Futures are in second place (over 40%). The share of algorithmic traders in the Forex market, options markets and fixed income markets is noticeably lower.

Algorithmic trading has been shown to outperform human trading in several key metrics. Aldridge (2009), for example, shows that algorithmic funds consistently outperform traditional funds. Aldridge (2009) also shows that algorithmic tools outperform classical ones in returns during periods of crisis.

Algorithmic trading has been shown to outperform human trading in several key metrics. Aldridge (2009), for example, shows that algorithmic funds consistently outperform traditional funds. Aldridge (2009) also shows that algorithmic tools outperform classical ones in returns during periods of crisis.

Interesting study was carried out by the Central Bank for the Russian stock market and currency pair USDRUB. According to it, 50 HFT algorithms work on this currency pair, providing more than half of the order volume.

This may be due to the lack emotions inherent in algorithmic trading systems compared to human beings driven by emotions. In addition, computers are superior to humans in such basic tasks as collecting information and quickly analyzing multiple data and news. Physiologically, the human eye cannot capture more than 50 data points per second. In modern films, the human eye is exposed to only 24 frames per second. Even then, most static images displayed over successive frames appear to us to be continuously moving objects.

For comparison, modern price flow includes rapidly changing quotes, the number of which can easily exceed 1000 per second per financial instrument. You need to be able to quickly process all this information, make various calculations and make trading decisions based on them.

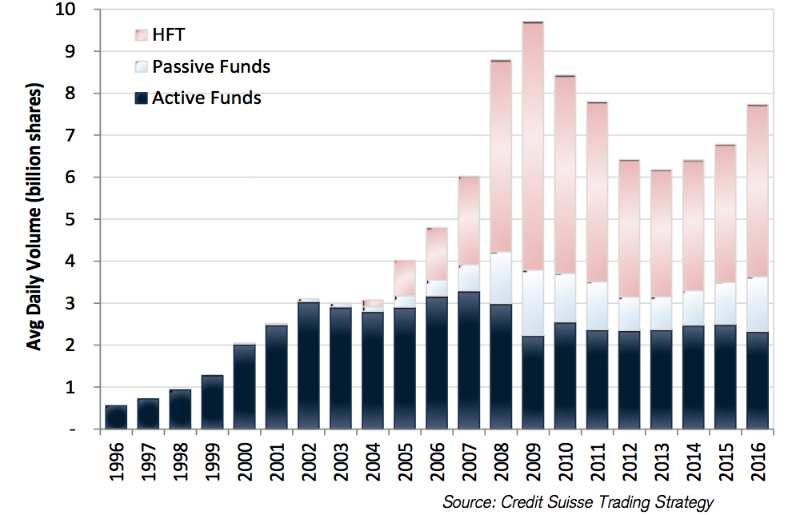

In the spring of 2017, Credit Suisse bank analysts published a report on “the real role of HFT trading in the modern financial market ecosystem.” The document talks about how high-frequency trading has changed the landscape of world exchanges. Here are the study's four main findings.

Trading volumes have increased

The development of high-frequency trading technologies has had the largest, most noticeable and long-lasting impact on trading volumes. Credit Suisse estimates that the trading volume of fiduciaries and investors, both active and passive, in the US stock market has remained virtually unchanged over the past ten years (3-4 billion shares per day).

At the same time, the total trading volume on US exchanges more than doubled in the period after the 2008 crisis; it was during these years that HFT trading developed especially actively.

At the same time, the total trading volume on US exchanges more than doubled in the period after the 2008 crisis; it was during these years that HFT trading developed especially actively.

This fact also has negative consequences. For example, the topic of “fake” trading activity is widely discussed robots, which may place multiple bids and then cancel them outright in hopes of influencing the price. However, overall, Credit Suisse analysts believe that “much of the HFT activity helps connect people in the financial market, reducing the time it takes for a counterparty to wait.”

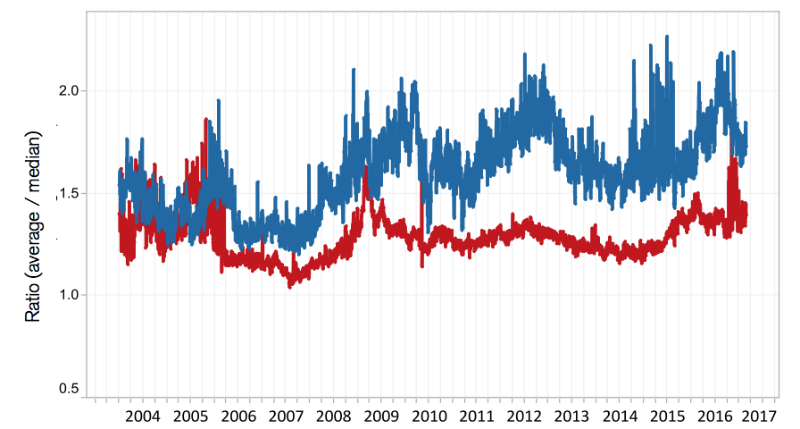

The difference in prices for buying and selling shares has changed

In theory, the less spread, the better for the market. The development of HFT has had an impact here too. The size of spreads for shares of large companies has decreased, while for smaller companies, on the contrary, they have increased. This suggests that high-frequency traders are more often interested in more liquid shares of well-known companies.

According to a report by Credit Suisse, equity spreads move in line with volatility, and the dispersion of spreads between the most and least liquid stocks has increased significantly since 2009. That is, spreads between large and small company stocks no longer move in the same direction.

According to a report by Credit Suisse, equity spreads move in line with volatility, and the dispersion of spreads between the most and least liquid stocks has increased significantly since 2009. That is, spreads between large and small company stocks no longer move in the same direction.

Stocks of large and small companies are volatile at different times of the day

Increased volatility in shares of large and small companies in recent years has been observed at various periods of the trading day. For example, at the beginning of trading, the price of shares of not the largest companies changes more actively. This happens because it takes more time to determine a fair (at the moment) price for such shares. However, by the end of the trading session, on the contrary, such shares behave calmer than securities of large organizations.

In contrast, shares of large companies that are actively traded in the market sometimes experience price fluctuations where they move rapidly within the spread multiple times at the end of the trading day. Analysts also attribute both of these phenomena to hft.

In contrast, shares of large companies that are actively traded in the market sometimes experience price fluctuations where they move rapidly within the spread multiple times at the end of the trading day. Analysts also attribute both of these phenomena to hft.

The number of noticeable spikes in the prices of shares of large companies has decreased

Typically, HFT trading strategies are aimed at profiting from market inefficiencies rather than participating in large price movements. This results, among other things, in a reduction in large price fluctuations of well-known companies, with which high-frequency traders more often transact.

Execution speed

Often, an extra millisecond can lead to a trader receiving a loss instead of a profit, because his trading robot was ahead of someone else. The pursuit of speed and the financial bottom line at stake has led to the rapid development of various technologies to reduce trade delays. Here are some of the approaches used to improve performance.

Direct access to the exchange

To trade on the stock exchange, an investor must enter into an agreement with a broker who provides access to trading. Typically, such companies also develop their own trading systems, which process customer orders before sending them to the core of the exchange system. However, in a situation where everything can be decided in a few milliseconds, the “user - brokerage system - exchange” scheme is not suitable for everyone.

To remove the unnecessary link in the form of a brokerage system, the technology of direct access to the exchange (DMA, direct market access) was created. Its essence lies in the fact that the application is submitted directly to the exchange’s trading system, bypassing the broker’s infrastructure.

Direct access is a technology for high-speed access to exchange platforms, in which an application is submitted to the exchange's trading system directly, bypassing the broker's trading system. All this allows you to significantly reduce the time it takes to deliver an application to the exchange and obtain information about its status.

With such an organization of the trading process, a trader can count on a significant gain in time. For example, when directly connecting to the stock and foreign exchange markets of the Moscow Exchange, the application processing time is reduced to 0.5 ms, and on the FORTS and Standard markets it does not exceed 3 ms. When using a brokerage system, orders are processed in a time from 5-10 ms to 150-500 ms, depending on the brokerage system, market type and connection method. Through brokerage systems, orders are processed 10-100 times slower than with a direct connection (although this speed is quite satisfactory for many traders).

We are still talking about very short periods of time from a human point of view, but for some trading strategies such a difference can be critical and affect their overall performance. Naturally, using direct access technology costs more, often significantly, and is only suitable for those who perform a large number of transactions per day and are willing to pay for their speed.

Despite the fact that technically, thanks to direct access to the exchange, traders can carry out trading operations without going through a broker, documented access is still provided through broker companies. That is, in order to get the opportunity to directly trade on, say, the stock market of the Moscow Exchange, an investor needs to enter into an agreement with a broker and purchase the service of direct access to the exchange from him.

Placing equipment near the exchange

If we continue to move along the chain of reducing the time for performing transactions, it becomes obvious that it is necessary to place the trading robot not only logically, but also physically as close as possible to the servers with the core of the exchange trading system.

Direct access to the exchange allows you to logically bring the trading system closer to the core of the exchange, but it is obvious that you can get even greater speed gains by placing it physically closer to this end point. As a rule, exchanges provide equipment colocation services in their data centers. In this case, the trading system can be launched on a server that is actually located in the same rack with the exchange core servers.

The robot can be located either on a separate server, which can be placed in a rack in a data center (this service is called Colocation), or on a virtual machine (Hosting), which in turn is launched together with the virtual machines of other clients on a server also installed in the data center, next to the exchange servers. Hosting services are, as a rule, provided only by large brokers with their own racks in data centers.

Placement in the exchange colocation zone allows you to connect trading robots directly to the exchange core. Also in this zone it is possible to obtain market data (Market Data) using the FAST protocol, which we will talk about a little later. The advantage of using a free colocation zone is the fact that this option is much cheaper. But when it comes to the pursuit of speed, high-frequency traders choose the fastest option, even though it can sometimes be the most expensive.

Placing in the exchange colocation zone has obvious advantages: virtual machines and servers connect directly to the core of the exchange, while from the free zone the connection goes through intermediate servers. In addition, receiving data via the FAST protocol and a dedicated channel for connecting to the market are available only from the exchange colocation area.

One way to significantly reduce infrastructure costs is to place the robot in a free colocation zone. The services provided in it are almost similar to the services of the exchange colocation zone. However, there is only free cheese in a mousetrap - you will have to pay for the relative cheapness of deploying a robot with a few milliseconds of increased transaction processing speed.

In addition, since the interfaces for creating direct connection software do not initially imply any graphical capabilities for displaying information about trading, the ability to synchronize orders and positions formed on a direct connection with the broker’s trading system in real time is practically a necessary thing for monitoring trading operations. Therefore, many brokers try to provide their clients with such opportunities.

All this, in comparison with regular access to the exchange through brokerage systems, costs money, and quite a lot. However, for those investors who have reached a certain level of income, such spending makes sense. According to representatives of the exchange, the owners of robots that won the “Best Private Investor” competition in 2011 spent from 100 to 500 thousand rubles per month on services related to direct access. However, taking into account the fact that some traders (although there were not so many of them) managed to reach a profitability of over 8000% and earn millions of rubles per month and, taking into account all the commissions of the broker and the exchange, these expenses paid off quite quickly.

Hardware acceleration (FPGA)

In the last few years, the use of FPGAs has become widespread among algorithmic traders to reduce latency in trading applications. Modern FPGAs can implement various aspects of high-speed trading systems. For example, market data processing can be done entirely on the FPGA without transferring it to the machine's processor.

Using programmable hardware allows you to get serious gains in processing speed and reduce latency, but there are also some difficulties. First of all, these include the complexity of developing and supporting trading applications using FPGAs. To interact with hardware, traders need to master not only high-level programming languages, but also the so-called hardware description languages (HDL, hardware description languages). Also, do not forget about the need for additional expenses on the equipment itself.

New data transmission technologies

The most important component of success in high-frequency trading is data transfer speed. Market players are actively looking for various ways to optimize it, which leads to the development of technologies such as data transmission using microwave radiation. Despite certain disadvantages (unresistant to rain and fog, limited bandwidth), it makes it possible to send data directly. In other words, you don’t need to lay a fiber optic cable through the mountains, you can simply install antennas on towers and find the shortest distance between point A and B. Thus, requests can be transmitted over the air faster than through fiber optics.

Such technologies are quite expensive, but the possible financial return from their use is so great that many HFT companies are investing millions in building their own microwave networks.

However, the use of microwaves to transmit data is not the only innovation. Like the Wall Street Journal wrote back in 2014 - the next technological breakthrough in this area could be the creation of data transmission networks using lasers. According to journalists, HFT companies have already agreed to create a similar network to work with the Nasdaq exchange.

Types of protocols and connection methods

In general, the direct access scheme is as follows: the server with the trading robot is connected to an intermediate server, which is located as close as possible to the core of the exchange trading system. This server has special software installed - the so-called gateways, which are used to transmit orders and market information directly to the trading system. At the same time, various protocols and connection methods are used to perform operations and receive data.

Currently, exchanges offer the following protocols for developers to directly access exchange markets:

| Protocol | Markets | Available features |

| ASTS Bridge | Stock, Currency | Trading + receiving all market data. 100% support for all operations. |

| Plaza II | Urgent | Trading + receiving all market data. 100% support for all operations. |

| FIX | Stock, Foreign Exchange, Urgent, OTC | Trading operations in basic trading modes (without support for negotiated transactions), Trade Capture (stock and currency only), Drop Copy. |

| FAST | Stock, Currency, Urgent | Obtaining anonymous market data. |

| Information and statistical server (ISS) | All | Obtaining anonymous market data through exchange web services. |

ASTS Bridge

The exchange gateway is Bridge. Gateway, which I also really want to translate as a gateway, is another story, it’s more of an access server. Gateway is a native protocol of the ASTS trading and clearing system, existing since 1998 (previously the solution was called TEAP (TCP/IP version) or TEServer (RS-232 version, no longer supported)). Many developers know the protocol under the name MTESRL, after the name of the corresponding DLL. Due to the native nature of this protocol, its main feature is the support of all transactions and all market data from all markets operating on the ASTS trading and clearing system.

The use of this protocol is recommended primarily for those who need access to clearing data and operations (viewing their positions, obligations, risk parameters, setting various kinds of limits, transferring securities and money between accounts, and so on), as well as participating in trading in negotiated transaction modes (that is, not quick anonymous trading in the order book, but direct conclusion of transactions with a specific counterparty). The API is provided as a dynamic library - in 32- and 64-bit versions for Windows and Linux.

The connection architecture is as follows: the dynamic library is included in the package of the software you developed, this package is installed on a server that has network access to the so-called server part of the gateway. The server part is a kind of proxy server, which is located at the broker and is connected to the exchange infrastructure via dedicated network channels.

In the case of HFT trading, when your software installed in the exchange data center under colocation conditions, an intermediate link in the form of a gateway server is no longer required - you connect directly to the exchange Gateways.

An interesting feature of the gateway protocol is its support for “interfaces”. An interface is a versioned set of tables and transactions available to the user, with the corresponding structure and data types. With almost every update of the trading and clearing system, new opportunities appear for users that require modifying the table structure or changing the transaction format. The presence of versioned interfaces allows users who are not ready for changes to remain on the old version of the interface and not modify their software.

Protocol Plaza II

For direct connection, native protocols are used. These protocols arose even before the merger of the MICEX and RTS exchanges into the Moscow Exchange. Thus, in the markets belonging to the RTS exchange (FORTS - futures and options, Standard), the Plaza II protocol is used to directly carry out transactions and receive data in connection mode.

To connect using this protocol, the exchange provides the CGate API. On the one hand, this allows trading participants to implement full-fledged functionality for accessing trading, including clearing functionality for limiting sections, setting restrictions on instruments and viewing market maker obligations. On the other hand, this allows clients of trading participants to implement their own high-speed robots with a minimum set of functions (place an order or withdraw an order). The API is provided as a set of dynamic libraries - in 32- and 64-bit versions for Windows and Linux.

With almost every release of the derivatives market, the exchange makes changes and improvements to its own program code, which is transmitted to clients in the form of an API. To the user, it looks like a new distribution with new versions of the libraries inside. In addition to the code itself, the structure of the data provided to users changes periodically along with the release.

FIX protocol

The FIX protocol (Financial Information eXchange) is a financial information exchange protocol that is a global standard for the exchange of data between exchange trading participants in real time. Supported by the world's largest exchange platforms, including the Moscow Exchange and all Forex market brokers.

The creation of the FIX protocol was initiated by a number of US financial organizations in 1992 - brokers and investment funds wanted to speed up the process of carrying out trading operations on the exchange. At that time, a significant part of trading transactions were carried out using the telephone, and the FIX protocol made it possible to transfer interactions to electronic form.

As a result, an open standard for transmitting information electronically was born, which is not controlled by any of the large organizations. Today, FIX has become an industry standard that is used by financial market participants in different countries to link their products.

Currently, the protocol is defined at two levels - session (working on data delivery) and application (describing the content of the data). There are two protocol syntax options - traditional, like Tag=Value, and in XML format (FIXML).

Work on creating the XML syntax began in 1998, and the first version of FIXML appeared in January 1999. At the beginning of the XML version of FIX, only the DTD syntax definition mechanism was used. Subsequently, the W3C organization developed a new mechanism - XML Schema, which forced the FIX developers to adapt the standard to use this syntax option.

This step allowed us to improve the XML version of the FIX protocol, in particular, users were able to add attributes and contextual abbreviations to messages. The basic organization of XML schema involves the data types used in the fields, which are contained in a separate file. FIX fields are defined in a special shared file, and components and FIXML syntax elements are defined in special component files. FIXML messages are defined using special files that indicate the category.

FAST protocol

In November 2004, the then CEO of the financial holding Acrhipelago Holding, Mike Cormack, at a FIX community conference called FPL (FIX Protocol Limited) in New York, stated that the current version of the protocol could not cope with the increased volume of financial information generated in the stock market. When transferring large volumes of data using FIX, there were significant delays in their processing, which brought losses to traders and deprived them of the opportunity to develop effective trading strategies.

The classic Tag=Value message passing format used in FIX turned out to be too cumbersome to process quickly. Soon after this speech, the first steps were taken to correct the situation.

When creating the FAST protocol, the developers pursued the goal of achieving the ability to transfer large amounts of data, avoiding delays in receiving information. The development of the protocol was carried out by a working group of the FIX community called the Market Data optimization working group (mdowg), which was formed in 2004.

In 2005, the group’s experts presented a pilot project (proof of concept) of the protocol, and a year later the first version of FAST 1.0 was released. Subsequently, several updates were released, and currently most financial market players use protocol version 1.2.

According to the FIX protocol standard, each message has the format Tag = Value SOH, where Tag is the number of the transmitted field, Value is its value, and SOH is the separator character. The FAST protocol eliminates redundancy by using a template that describes the structure of the entire message. This method is called "implicit tagging" because the FIX tags in the transmitted data are only implied.

ISS

This protocol stands out somewhat from the general series, since it covers a segment of tasks related not to carrying out transactions, but to working with exchange data. Essentially, this is an API for exchange web services, implemented according to the Restful concept. It makes it possible to obtain general market information, such as quotes, transactions, indices, volumes, trading results, and so on, via the http/https protocol. The service is only available via the Internet, so minimizing delays in receiving data does not apply to it.

This protocol is used to display stock quotes on websites (including all data on the moex.com website is broadcast from there), download trading results for analytics, and render graphs on various demo panels and displays and in any other applications running via the Internet.

For those traders who do not use robots for trading, there is the opportunity to trade on a direct connection, using a trading terminal that is more familiar to them. However, the software that works with the brokerage trading system does not work with direct exchange protocols, so separate programs are created for it.

Additionally, because direct-to-connect technologies are open, investors can develop the software for themselves. However, since these programs ultimately have almost direct access to the core of the trading system, the exchange has implemented a procedure for certifying trading solutions from third-party developers to eliminate the possibility of a “crazy robot” completely destroying the entire system. This procedure goes through both the development of individual investors and software created by special companies to order.

What do exchange data centers look like?

The NYSE Euronext data center is located in Mahwah, New Jersey. The area of the halls used for traders' server colocation is about 18 thousand square meters, while the total building area exceeds 120 thousand square meters. Data Center Knowledge published some photos of this data center.

Facility Management Center - it combines the interfaces of building management systems (BMS) and data center infrastructure management (DCIM). This is where specialists sit who control temperature and humidity conditions, the condition of power supplies and other elements in each server room.

And this is what the “hot corridor” looks like, into which the air emitted by the servers enters:

And this is what the “hot corridor” looks like, into which the air emitted by the servers enters:

The long main corridor of the data center allows you to feel the enormous scale of the facility.

The long main corridor of the data center allows you to feel the enormous scale of the facility.

Equinix is one of the world's largest players in the data center and colocation market. One of its facilities is a former optical manufacturing plant in Secaucus, New York, with an area of more than 100,000 square meters, converted into a state-of-the-art data center. Exchanges such as NASDAQ, BATS, and CBOE use its services, and this is what it looks like.

Equinix is one of the world's largest players in the data center and colocation market. One of its facilities is a former optical manufacturing plant in Secaucus, New York, with an area of more than 100,000 square meters, converted into a state-of-the-art data center. Exchanges such as NASDAQ, BATS, and CBOE use its services, and this is what it looks like.

There are bars on either side of the data center's long main corridor; These grilles and posts are connected by a cable that runs through yellow overhead cable ducts.

The 12-meter high ceiling provides ample space for multiple levels of cable ducts that fill the top of the Equinix data center, containing separate ducts for interconnect, carrier and power cables.

The 12-meter high ceiling provides ample space for multiple levels of cable ducts that fill the top of the Equinix data center, containing separate ducts for interconnect, carrier and power cables.

The uninterruptible power supply (UPS) room in the Equinix NY4 data center, powered by a 26-megavolt-ampere substation. The equipment consists of a 30 megawatt uninterruptible power supply system that supports the operation of the computing installation in the event of a power failure.

The uninterruptible power supply (UPS) room in the Equinix NY4 data center, powered by a 26-megavolt-ampere substation. The equipment consists of a 30 megawatt uninterruptible power supply system that supports the operation of the computing installation in the event of a power failure.

In the event of a power outage, the NY4 data center equipment is equipped with these 18 backup Caterpillar diesel generators with a capacity of 2.5 megawatts each, which in total provide 46 megawatts of emergency power, enough to fully power the equipment, as well as refrigeration units and UPS systems. During Hurricane Sandy, these generators kept equipment running for an entire week.

In the event of a power outage, the NY4 data center equipment is equipped with these 18 backup Caterpillar diesel generators with a capacity of 2.5 megawatts each, which in total provide 46 megawatts of emergency power, enough to fully power the equipment, as well as refrigeration units and UPS systems. During Hurricane Sandy, these generators kept equipment running for an entire week.

The NY4's refrigeration system features huge pipes that carry chilled water to the equipment, as well as a plate heat exchanger (right) that acts as a refrigerator in the winter, saving energy that would normally be wasted running the refrigeration units.

The NY4's refrigeration system features huge pipes that carry chilled water to the equipment, as well as a plate heat exchanger (right) that acts as a refrigerator in the winter, saving energy that would normally be wasted running the refrigeration units.

Currently, the largest Russian exchange platform, Moscow Exchange, offers traders the opportunity to place their equipment in the Moscow M1 data center. The data center was put into operation in 2006, its total area is 3850 square meters, of which 2400 square meters are allocated for server rooms (load capacity 5-8 kW per rack). There are about 950 such racks in total.

Currently, the largest Russian exchange platform, Moscow Exchange, offers traders the opportunity to place their equipment in the Moscow M1 data center. The data center was put into operation in 2006, its total area is 3850 square meters, of which 2400 square meters are allocated for server rooms (load capacity 5-8 kW per rack). There are about 950 such racks in total.

To maintain the required temperature (22 ± 4 degrees) and humidity (45 ± 10%), supply and exhaust ventilation systems and precision industrial-type air conditioners are installed in the server rooms.

Server racks are arranged according to the principle of hot and cold aisles; closing the latter prevents the mixing of hot air emitted by equipment with cold air coming from air conditioners.

Server racks are arranged according to the principle of hot and cold aisles; closing the latter prevents the mixing of hot air emitted by equipment with cold air coming from air conditioners.

Uninterruptible power supplies are designed for a longer operating time of all equipment than is necessary to start diesel generator sets and switch to autonomous power supply to the data center.

Uninterruptible power supplies are designed for a longer operating time of all equipment than is necessary to start diesel generator sets and switch to autonomous power supply to the data center.

In 2014, the management of the Moscow Exchange decided to move to the DataSpace1 data center. The data center was commissioned in July 2012. Its total capacity is 1,062 rack spaces across 12 machine rooms, each with an area of up to 255 square meters.

In 2014, the management of the Moscow Exchange decided to move to the DataSpace1 data center. The data center was commissioned in July 2012. Its total capacity is 1,062 rack spaces across 12 machine rooms, each with an area of up to 255 square meters.

The data center has 6 independent power supply circuits, each computer room is supplied with electricity from 2 independent circuits.

Chillers and dry air coolers are installed according to a N+1 distributed redundancy scheme, cold air is supplied under the floor.

Chillers and dry air coolers are installed according to a N+1 distributed redundancy scheme, cold air is supplied under the floor.

The building's perimeter and interior spaces are equipped with an 8-level security system that includes various access control and surveillance components.

The building's perimeter and interior spaces are equipped with an 8-level security system that includes various access control and surveillance components.

Exchange platforms and HFT traders pay great attention to building their own trading infrastructure. Today, in the stock market, success and failure are often separated by a fraction of a second, so both the software and hardware that powers financial applications must work extremely reliably.

Exchange platforms and HFT traders pay great attention to building their own trading infrastructure. Today, in the stock market, success and failure are often separated by a fraction of a second, so both the software and hardware that powers financial applications must work extremely reliably.

The load level is so high that it is difficult to cope with and requires significant investment on the part of data center service providers. Otherwise, situations such as the one may arise happened in August 2015, in the CenturyLink data center - during a serious movement in the market, the infrastructure for HFT trading was working in an increased mode, which the ventilation system (HVAC) could not cope with. As a result, many servers not only overheated, but physically burned out.

Types of HFT platforms

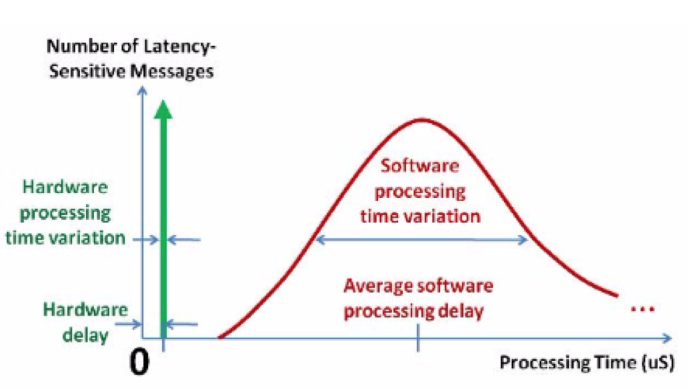

Currently, most traders and brokers build their HFT systems using popular software and hardware technologies. This allows algorithms to be described in high-level programming languages familiar to many developers, and changes can be made to them quite quickly if necessary. However, the pursuit of speed means that the unpredictable response times of software systems become an obstacle to successful trading. Let's look at the existing software and hardware approaches to building HFT systems.

Software high-frequency platforms

There are quite a large number of companies offering software for high-frequency trading (for Western exchanges these are, for example, Mantara, Ulink and QuantHouse). When using them, most of the delays occur in the operation of the operating system on which the software is running, as well as the network stack. To combat this, users can use high-performance network cards (such as those from Solarflare or Myricom) that speed up certain parts of the network stack.

Custom hardware HFT platforms

The relatively high latency of software trading platforms has forced the industry to look for alternative approaches to reducing latency using custom hardware. Generally, things like ASICs are not considered in HFT trading because they lack the flexibility to be reconfigured or handle new protocols. GPUs also cannot offer significant performance. FPGA (Field-Programmable Gate Arrays) technology has become a suitable tool for obtaining flexibility and achieving the required performance.

FPGAs can be used to accelerate financial applications in a variety of ways. One of them is called Hybrid Computing and is used, for example, in models risk management, option pricing and portfolio modeling. When using it, the speed of the system can increase by three orders of magnitude.

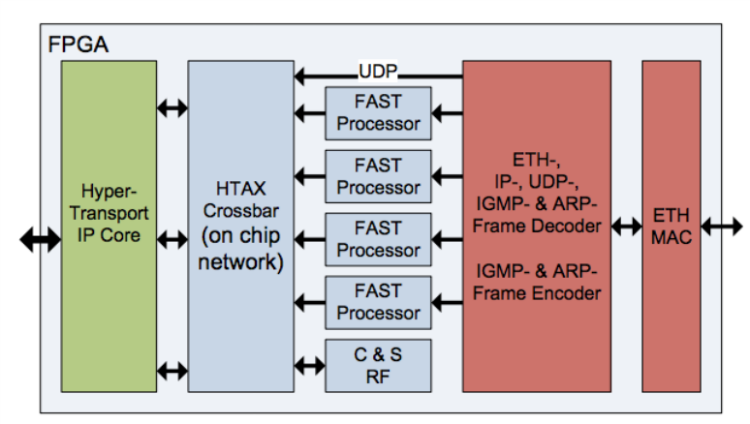

FPGAs are often used to create modern online trading systems. The tasks of processing Ethernet, IP, UDP connections and decoding the FAST protocol are transferred to this hardware. FPGA parallelism allows for significant speed gains compared to software-only tools. The architecture of the system described in this work looks like this:

This approach complements conventional multi-core processors with FPGA coprocessors. Typically, communication with the CPU is carried out using high-speed connectors such as FrontSide Bus (FSB), PCI Express or QPI. In this case, the trading modules themselves are written in high-level programming languages.

This approach complements conventional multi-core processors with FPGA coprocessors. Typically, communication with the CPU is carried out using high-speed connectors such as FrontSide Bus (FSB), PCI Express or QPI. In this case, the trading modules themselves are written in high-level programming languages.

Another way to use programmable logic for acceleration is through the use of so-called Smart NICs. Typically this refers to a combination of high-speed network interfaces, host PCI interfaces, memory and FPGAs. Here, the FPGA acts as a NIC controller, acting as a bridge between the host computer and the network and allowing software logic to be integrated directly along the data path. Thus, Smart NIC can operate as a trading platform controlled by the host machine's CPU.

Modern FPGAs can implement any aspect of HFT applications. Incoming market data can be processed entirely on the FPGA without having to be sent to the processor. Incoming network data is fed directly to a customized, highly optimized system via the MAC and PHY hardware. Moreover, in fact, the necessary information can be extracted even before the packet is fully received. Thus, the use of FPGA allows for a significant reduction in overall latency.

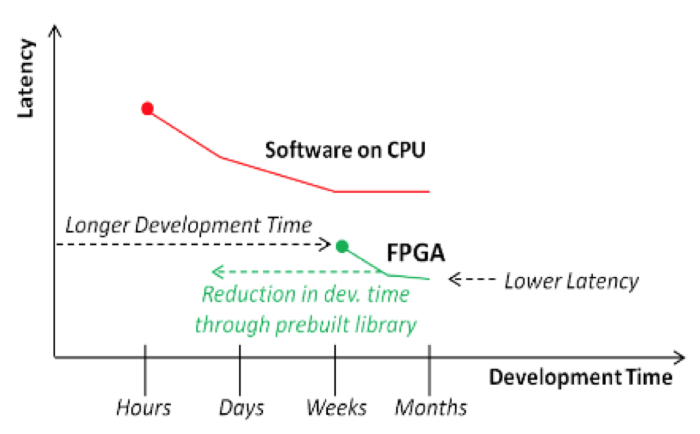

The use of FPGAs also has its disadvantages compared to traditional approaches to developing trading systems. The root of the problem is the higher complexity of the FPGA development flow. A significant portion of financial system developers and traders are not familiar with this technology and lack the knowledge and expertise to implement hardware-oriented development.

The use of FPGAs also has its disadvantages compared to traditional approaches to developing trading systems. The root of the problem is the higher complexity of the FPGA development flow. A significant portion of financial system developers and traders are not familiar with this technology and lack the knowledge and expertise to implement hardware-oriented development.

Due to the lower level of abstraction, developing and testing new hardware solutions is a more complex and time-consuming process compared to the usual writing of a trading robot. All this is illustrated in the figure below:

To avoid this, some FPGA-based HFT platforms have special high-level environments that allow you to create trading systems without the need to use hardware description languages (HDL).

To avoid this, some FPGA-based HFT platforms have special high-level environments that allow you to create trading systems without the need to use hardware description languages (HDL).

The architecture of modern graphics cards is based on a scalable array of streaming multiprocessors. One such multiprocessor contains eight scalar processor cores, a multi-threaded instruction module, and shared memory located on the chip (on-chip).

When a C program using CUDA extensions calls a GPU kernel, copies of that kernel, or threads, are numbered and distributed to available multiprocessors, where their execution begins. For this numbering and distribution, the core network is divided into blocks, each of which is divided into different threads. Threads in such blocks execute simultaneously on available multiprocessors. To manage a large number of threads, the SIMT (single-instruction multiple-thread) module is used. This module groups them into “packs” of 32 threads. Such groups are executed on the same multiprocessor.

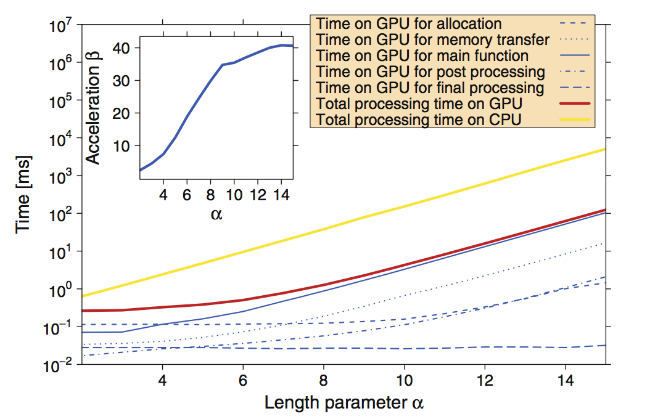

Financial analysis uses many measures and indicators, the calculation of which requires serious computing power. A measure called the Hurst exponent is used in time series analysis. This value decreases if the delay between two identical pairs of values in the time series increases. The concept was originally used in hydrology to determine the size of a dam on the Nile River in conditions of unpredictable rainfall and drought.

Subsequently, the Hurst exponent began to be used in economics, in particular, in technical analysis to predict trends in the movement of price series. Below is a comparison of the speed of calculating the Hurst exponent on the CPU and GPU (acceleration indicator β = total calculation time on the CPU / total calculation time on the GeForce 8800 GT GPU):

Experiments show that the use of GPUs can lead to significant improvements in financial analysis performance. At the same time, the speed gain compared to using a CPU architecture can reach several tens of times. At the same time, you can achieve an even greater increase in performance by creating GPU clusters - in this case, it grows almost linearly. That is why GPU and FPGA technologies are widely used when building HFT systems.

Experiments show that the use of GPUs can lead to significant improvements in financial analysis performance. At the same time, the speed gain compared to using a CPU architecture can reach several tens of times. At the same time, you can achieve an even greater increase in performance by creating GPU clusters - in this case, it grows almost linearly. That is why GPU and FPGA technologies are widely used when building HFT systems.

What Is the Order Book

The order book (DOM, Depth of Market) is a list with a numerical display of current buy and sell orders for a given asset on the stock market at the prices set by participants. This indicator reflects the sentiment of market participants and is one of the trader's most important tools. It also has other names: the book of orders, Order Book, market depth (Depth of Market), Level 2, and the trading terminal's order book (Open Book). In simple terms, it is a table that displays information about the orders currently submitted by sellers and buyers.

During the trading sessions The exchange platform collects thousands of applications from all participants every second and brings them together. At the same time, the order book is just a form of visualization of the limit orders closest to the current price.