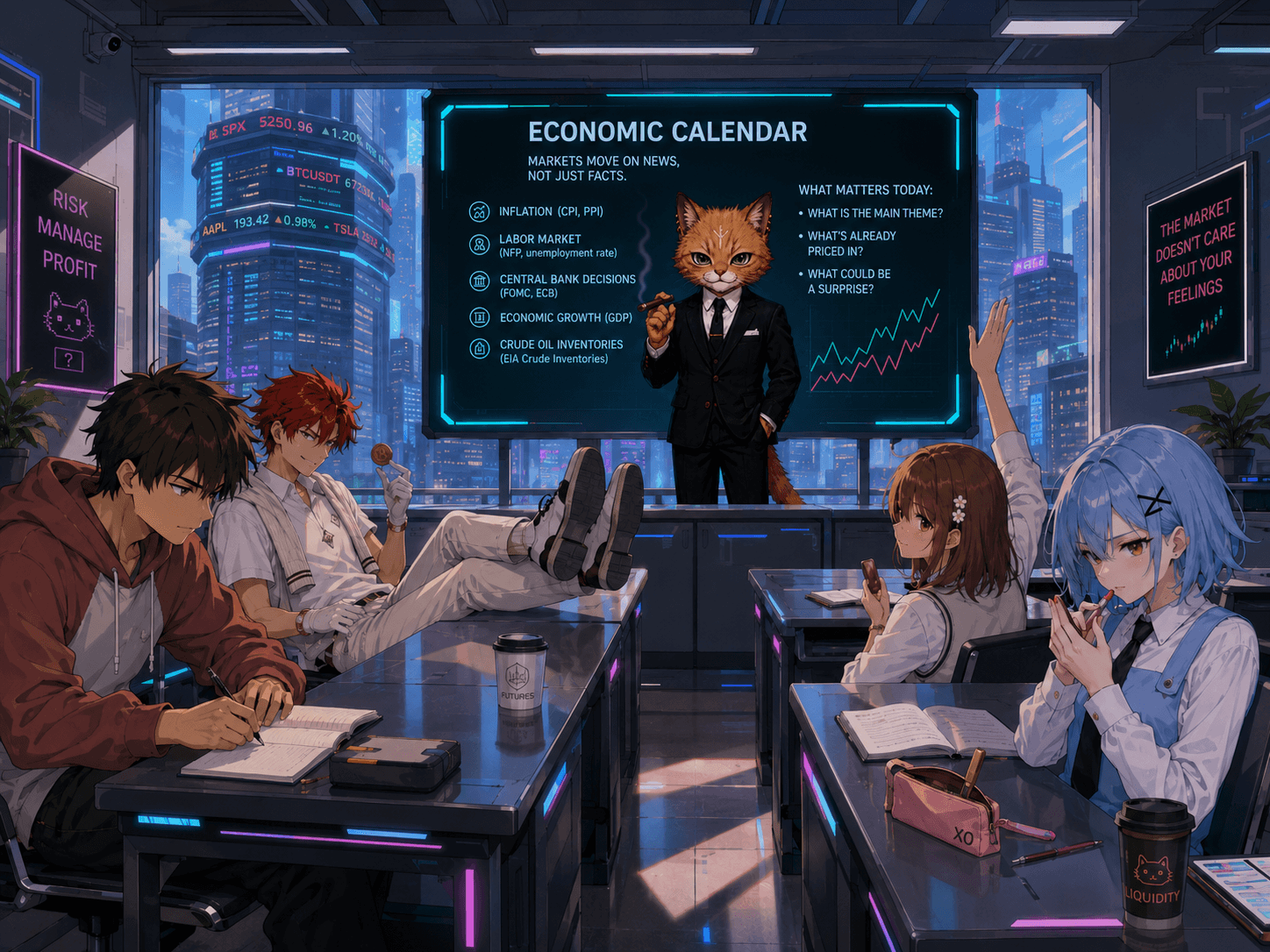

The Economic Calendar as a Trader's Tool

An economic calendar is a structured list of upcoming macroeconomic statistics releases, central bank decisions, speeches by officials, and other events that can affect financial markets. Each calendar entry usually contains: the release date and time, country of origin, indicator name, previous value, analysts' consensus forecast, actual value (after publication), and a subjectively assigned level of importance (usually one to three stars).

Traders use the calendar to assess potential volatility, plan trades, and manage risk. Fundamentally, the market reaction is determined not by the absolute value of an indicator, but by its deviation from the consensus forecast and, no less importantly, from informal "market expectations" (whisper numbers), which may not match the median forecast.

Historically, Russian-speaking retail traders used the economic calendar to trade the Forex market, whereas its influence on the stock market is much more significant.

Key News Groups by Asset Class

Among the key economic calendar news items, the following can be singled out.

The Forex Market and the U.S. Stock Market

For the currency market, priority is given to indicators that directly affect central bank monetary policy and the interest rate differential. The following economic news items are the most significant.

Interest rate decisions: FOMC (U.S. Fed), ECB, BOE (Bank of England), BOJ (Bank of Japan), and other major central banks. Even stronger moves are triggered by accompanying statements, press conferences, and dot plot forecasts.

U.S. labor market data: changes in nonfarm employment (Non-Farm Payrolls, NFP), unemployment rate, average hourly earnings, and job openings (JOLTS). These indicators are a direct reflection of the health of the economy and wage-driven inflationary pressure.

Inflation data (CPI, PCE): consumer price index (CPI), producer price index (PPI), core personal consumption expenditures deflator (Core PCE Price Index, preferred by the Fed).

GDP data: the first, second, and third estimates of quarterly GDP, especially for USD, EUR, and GBP.

Business activity indexes: ISM Services PMI (U.S.), Manufacturing PMI, and composite PMI indexes from S&P Global for key economies. The employment and price subindexes within ISM often provoke a sharper reaction than the headline figures.

Consumer demand data: retail sales in the United States.

Additional volatility is introduced by speeches from central bank chairs and board members if their rhetoric deviates from the policy path already priced in.

Corporate earnings reports (stock market only): formally, they are not part of the macroeconomic calendar, but earnings season creates a parallel stream of events that can both amplify and dampen macro reactions.

Cryptocurrency Market

Cryptocurrencies, especially Bitcoin and Ethereum, in current market conditions show a high correlation with risk assets, above all with the U.S. stock market.

Specific regulatory events: SEC decisions, regulatory statements on ETF products and major blockchain projects. Although these are not macroeconomic data, they make a substantial contribution to volatility and should be monitored in parallel with the classic calendar.

Financial indicators: flows into spot Bitcoin/ETH ETFs also serve as an important internal indicator of demand among speculators.

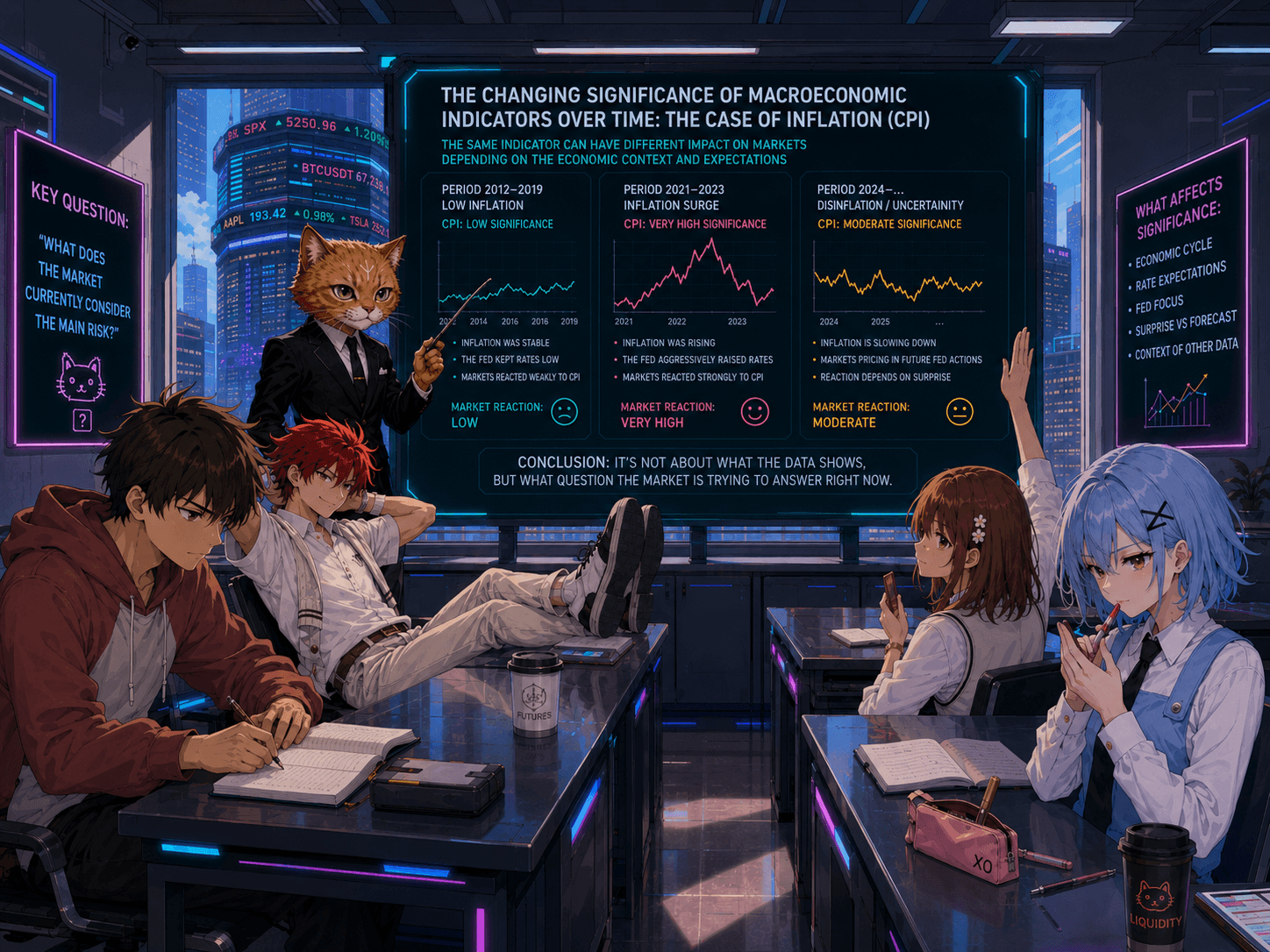

The Changing Significance of Macroeconomic Indicators Over Time

Mechanical use of lists of "important news" without understanding the current market paradigm leads to mistakes: what worked in 2002 does not work in 2022. Indicator rankings are not static; they evolve as the economic cycle changes.

Inflation: From Dominant Driver to Balancing Factor

In 2021-2022, markets were in an "inflation shock" regime. During this period, CPI releases often had a greater impact on the market than many central bank meetings.

Each CPI release triggered extreme moves in currency and stock markets: an above-forecast reading immediately priced in more aggressive Fed policy tightening, leading to a sharp rise in Treasury yields and a fall in stock indexes. At that time, inflation was the absolute priority of the Fed's mandate.

As inflation slowed by 2024-2025, the focus shifted. CPI and PCE remain important now, but their ability to generate an independent long-term trend has declined. The market has moved into a mode where stable or slightly declining inflation is already priced in, while data pointing to recession risk have become fundamentally important.

Today, a CPI release that comes in within expectations may not cause significant moves. By contrast, an unexpected NFP collapse can trigger a broad repricing across the entire range of assets.

Labor Market (Nonfarm Payrolls)

The Nonfarm Payrolls (NFP) report has for decades been considered one of the most anticipated releases of the month. The number of jobs created, the unemployment rate, and wage dynamics made it possible to assess the state of the economy long before quarterly GDP data were published.

When investors try to understand whether the economy faces recession or overheating, it is the labor market that becomes the main source of information.

In the current phase of the cycle (2024-2026), when the balance of risks has shifted from inflation toward an economic downturn, labor market data have become a trigger for volatility.

Weak NFP, rising jobless claims, or a decline in job openings (JOLTS) no longer cause relief, as they did in the era of fighting inflation, but fears of a hard landing. As a result, bad employment news has stopped being “good news” for stocks, the “bad news is good news” concept.

Now they are highly likely to lead to a decline in stock indices and a weakening of the dollar against safe-haven currencies (JPY, CHF), if the market sees the recession threat as stronger than the benefit from a rate cut. Thus, the market has returned to “normality”.

Thus, when inflation moves into the background, the influence of NFP can sharply increase again. Many traders make the mistake of assessing the importance of releases from memory: if CPI was the main driver two years ago, that does not mean it will always be so.

Crude Oil Inventories (EIA): Loss of Influence

There are not many news items in the economic calendar for the oil market.

Historically, the weekly report. The U.S. Energy Information Administration (EIA) report on changes in crude oil inventories was one of the key drivers for WTI and Brent prices. Inventory growth signaled falling demand or excess supply and pressured the price, while inventory declines did the opposite.

In recent years, the influence of these data has been substantially leveled out. The following reasons can be identified among the causes.

Dominance of geopolitical factors (conflicts, attacks on transport infrastructure, sanctions restrictions).

Active supply management by OPEC+, which overrides short-term inventory fluctuations. This should also include the release onto the market of oil accumulated in strategic reserves by the United States, China, Japan, and EU states.

The growing role of algorithmic trading, which parses headlines about geopolitics faster than the EIA report.

Today, the publication of inventory data often passes without a significant price response, unless it comes out extremely far beyond the consensus boundaries and at the same time overlaps with the geopolitical backdrop.

Manufacturing Index (ISM Manufacturing PMI)

For decades, it was considered a leading indicator of the economic cycle, so its role in the calendar cannot be underestimated.

However, as deindustrialization progressed and the share of services in U.S. GDP grew, its significance for the broad market decreased. Today, the main moves are caused by Services PMI (the services sector). Moreover, traders focus not only on the headline value, but also on the components:

The employment subindex as a leading signal for the main NFP.

The prices paid subindex as a proxy for inflationary pressure in the services sector.

A decline in the headline value with stable employment may be ignored, whereas a sharp drop in the employment subindex can provoke a strong reaction.

Central Bank Rhetoric: The Primacy of Expectations

Speeches by central bank heads require interpretation exclusively through the prism of current market expectations for the rate.

Tools such as CME FedWatch make it possible to quantitatively assess the probability of a rate change. If the market is already pricing in easing with a 90% probability, “dovish” comments will not trigger a rally: they are already priced in. By contrast, even a neutral comment will be perceived as a “hawkish” surprise and will lead to a decline in risk assets.

The classic approach of “dovish rhetoric means buy, hawkish means sell” does not work without assessing the current priced-in probability.

Practical Takeaways for the Trader

Identify the current dominant narrative. Analyze quarterly what is in focus within the mandate of the Fed and other central banks: fighting inflation or supporting the labor market. This determines which indicators are the main ones.

Compare the actual value not only with the consensus, but also with the “market whisper.” When there is a substantial divergence, the market reaction can be mixed and rapid.

Study the historical reactions of recent months to a specific release. If the reaction structure has changed (for example, weak employment data is no longer positive for stocks), take this into account in trading.

Do not overestimate calendar “stars.” Three stars almost always lose to a geopolitical headline. Context matters more than formal importance.

Filter out outdated indicators. If data has lost the ability to move the market (as happened with oil inventories), exclude it from active monitoring so as not to add noise to decision-making.

Use the TLAP economic calendar. The economic calendar provides an opportunity to find good trades.

Thus, the data available in the economic calendar is important, but expectations of volatility after its release change over time.

The calendar shows when the news will be released. Profitable trading begins when you understand why this particular news should interest the market today.