Funding Arbitrage of Cryptocurrency Futures

The list of arbitrage strategies available to the average user of popular crypto platforms is quite broad. Funding arbitrage holds an honorable second place in popularity among beginner arbitrage traders.

In this article, we will explain what funding arbitrage is, show where to find a bot to get acquainted with the strategy for educational purposes, and share a list of platforms and indicators that help better understand the concept of this strategy. And no investment recommendations, only food for thought.

A market-neutral position as the basis of funding arbitrage

The main idea of funding arbitrage is extremely simple. It is about receiving funding payments regardless of whether the price goes north or south.

How does a trader reduce risks? The only available method actively used by professionals and, to a lesser extent, by amateurs is creating a market-neutral (also called delta-neutral) position. To do this, the trader simultaneously opens two opposite trades on the same asset that hedge each other.

In practice, this means the following: if the price goes up, one position will bring a loss, while the second will bring a profit. In an ideal neutral structure, these profits and losses cancel each other out. Thus, the only source of income (or loss) remains the funding rate.

I hope everything is clear here.

Main funding arbitrage strategies and their variations

Classic spot-futures arbitrage (Spot-Futures Arbitrage)

The most common way to create a neutral position is a combination of the spot market and the perpetual futures market. It looks like this: the trader buys the coin on spot and simultaneously sells a perp for the same volume, and vice versa.

As a result of opening opposite positions, profit and loss mutually offset each other. Overall, the position is, if not breakeven, then with a very small floating loss within a narrow range.

At the same time, the trader receives funding payments: with a positive rate, longs pay shorts (the futures seller is in profit), and with a negative rate, sellers pay buyers (here the perp buyers are in profit).

Thus, the profitability of this arbitrage strategy directly depends on whether the trader manages to enter the position when the funding rate is favorable (positive for a short or negative for a long) and hold it long enough for the collected funding to cover all costs.

This strategy is considered the most reliable in terms of minimizing risks, since the spot position is a real asset and is not subject to such phenomena as liquidation (unless the trader uses borrowed funds to buy on spot). However, it requires the trader to have enough capital to fully buy the asset on the spot market, which reduces capital efficiency.

Cross-exchange funding arbitrage (Cross-Exchange Arbitrage)

This strategy does not require a spot asset. The trader looks for discrepancies in funding rates for the same asset but on different exchanges. For example, on exchange A the funding rate for BTC is positive and equals +0.02%, while on exchange B it is negative, -0.01%.

In this case, the trader can open a short position on exchange A (to receive funding from longs) and simultaneously open a long position on exchange B (to receive funding from shorts). Both positions hedge each other by price, and the trader receives both payments.

The profit here is the sum of the absolute values of both rates minus commissions and taking into account the potential difference in entry/exit prices. However, this method is more difficult to execute, requires funds on several exchanges, and increases operational risks.

We should also note that this method requires an automatic monitoring system with the right to open positions, if such an option is available.

Arbitrage using deliverable futures

Another method of funding arbitrage is opening opposite positions in the perpetual futures market and in the market for traditional deliverable futures (quarterly or monthly). In essence, this is the same classic funding arbitrage, but without working with spot.

The price of a deliverable futures contract usually differs from the spot price due to market expectations (contango or backwardation). If the funding rate on the perpetual futures is high, the trader can buy the deliverable futures instead of spot and sell the perpetual, locking in the spread and receiving funding.

Among the advantages of this method, we note significantly lower capital requirements compared with buying spot. The risks include stronger discrepancies between the futures than separately with spot.

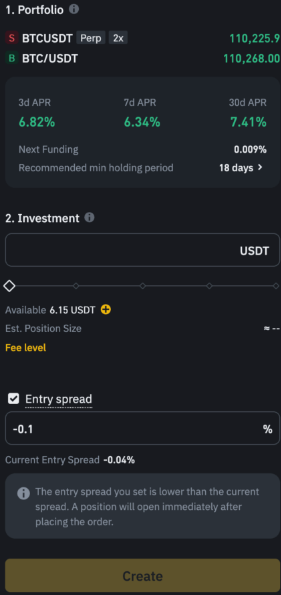

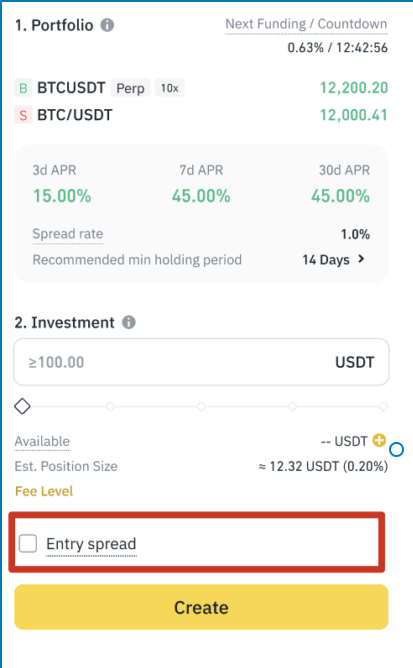

Funding arbitrage bot on Binance

On the Binance exchange, you can find a bot that offers to work with funding arbitrage. It is called exactly that: Funding Rate Arbitrage Bot.

What is worth paying attention to? First of all, the currency component.

- The investment asset for positive arbitrage on USDⓈ and COIN-M futures is USDT.

- The investment asset for reverse arbitrage is the base asset (for example, BTC, ETH, BNB).

The exchange provides a special buffer mechanism that makes it possible to avoid unexpected unplanned losses. Under this mechanism, the exchange reserves 10% of the initial investment amount as a buffer in case of a margin check and market fluctuations.

The most interesting thing is the ability to manage the spread when opening a position. The default spread is -0.1%.

Thus, when simultaneously buying spot and selling a perp, the entry spread is calculated by the formula: (futures price - spot price) / spot price. The reverse formula, (spot price - futures price) / futures price, is used when buying the futures and selling the coin.

Before launching the arbitrage bot, traders need to review the recommended minimum holding period. This is the estimated breakeven period calculated on the basis of the average funding rate over the past 30 days.

You can read more about how to create a Funding Rate Arbitrage Bot and what to do with it on this page.

Funding arbitrage indicators on Tradingview

There are not many indicators on the Tradingview platform for studying the features of the type of arbitrage we are discussing.

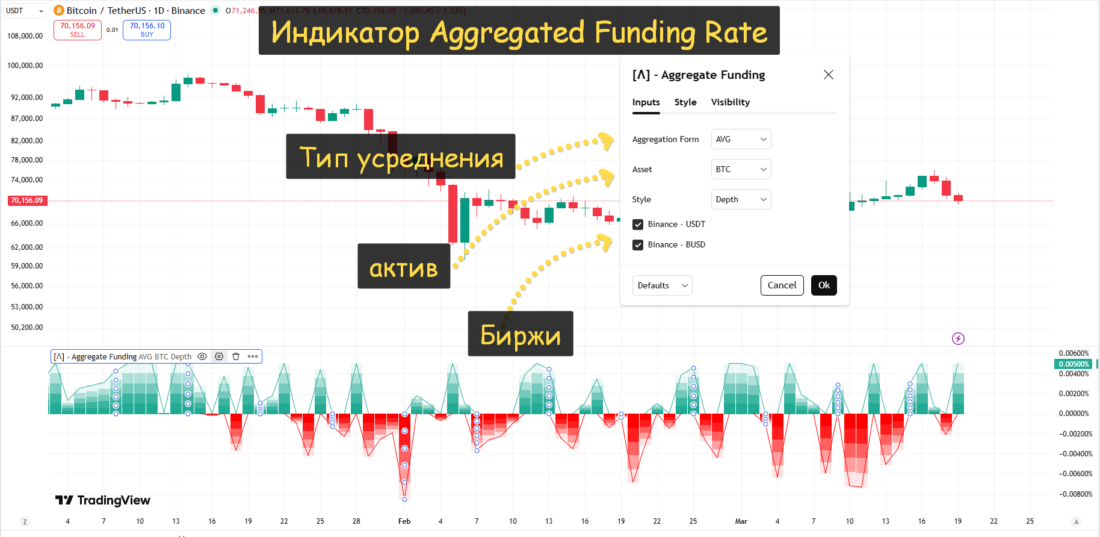

For a quick assessment of funding rates, we recommend taking a look at the Aggregated Funding Rate indicator. The indicator is almost three years old (released in May 2023), and during that time its page has been visited just under 28 thousand times.

The indicator combines data from BitMex and Binance and supports pairs with USDT and BUSD (31 assets in total). The aggregated value is calculated by determining the funding rate of the cryptocurrency for each perpetual chart (Binance - USDT and BUSD, BitMex - USDT and USD).

The calculation itself is based on the official formula of each exchange. As a result of the calculation, the values are summed or averaged depending on the user's choice. In addition, the user can independently choose which of the four sources will be included in the report.

The indicator has not been updated for a long time, but overall it looks quite good for a quick assessment of the situation on Binance without visiting the exchange itself.

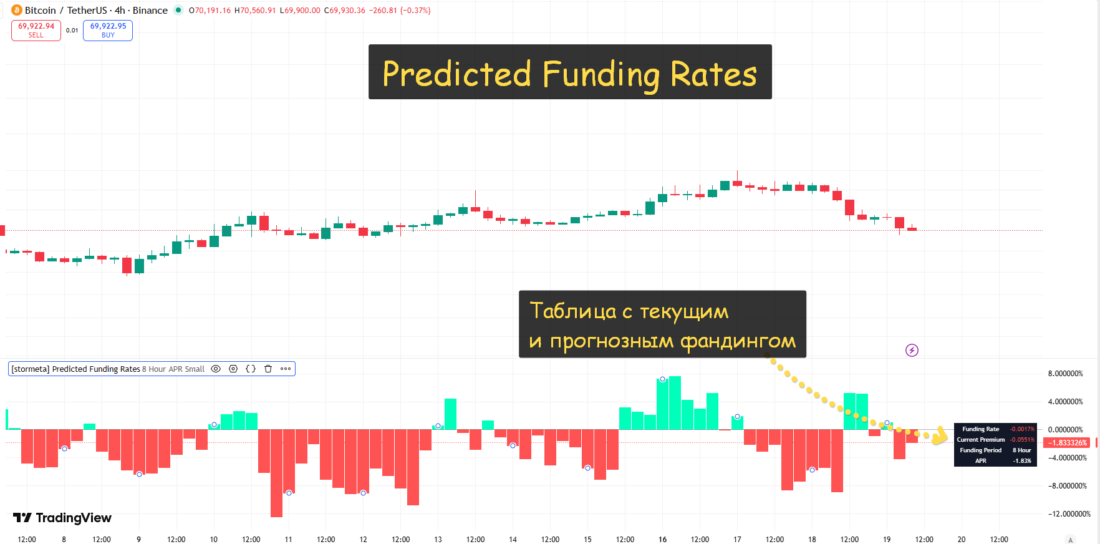

The Predicted Funding Rates indicator seemed much more interesting to us. It was released not so long ago, on September 30, 2025. During that time, its page has been viewed more than 6.7 thousand times. This is several times more than other similar indicators.

This indicator calculates funding rates for perpetual futures contracts on Binance in real time. To ensure forecast accuracy, triangular weighting algorithms are used across several timeframes.

The author reports two methods for estimating future funding.

Method 1. Collecting 1-minute premium data using triangular weighting over 8 hours. This detailed method makes it possible to forecast funding on the basis of data from the past 4 hours and more.

Method 2 involves using several timeframes. When calculating funding values for the daily timeframe, 1-hour data is used; for timeframes from 4 hours, 15-minute data is used. This dynamic method makes it possible to use higher timeframes and those sections where 1-minute data is not available.

The most important information provided by the indicator is located in the table at the bottom right. It includes the following data.

- Funding rate: the forecast funding rate as a percentage

- Current premium: the current premium (the difference between the perpetual futures price and the price of the underlying asset) as a percentage

- Funding period: you can choose between a 1-hour period (usually on HyperLiquid) and an 8-hour period (on Binance)

- APR: annual percentage rate.

Aggregators for viewing funding rates

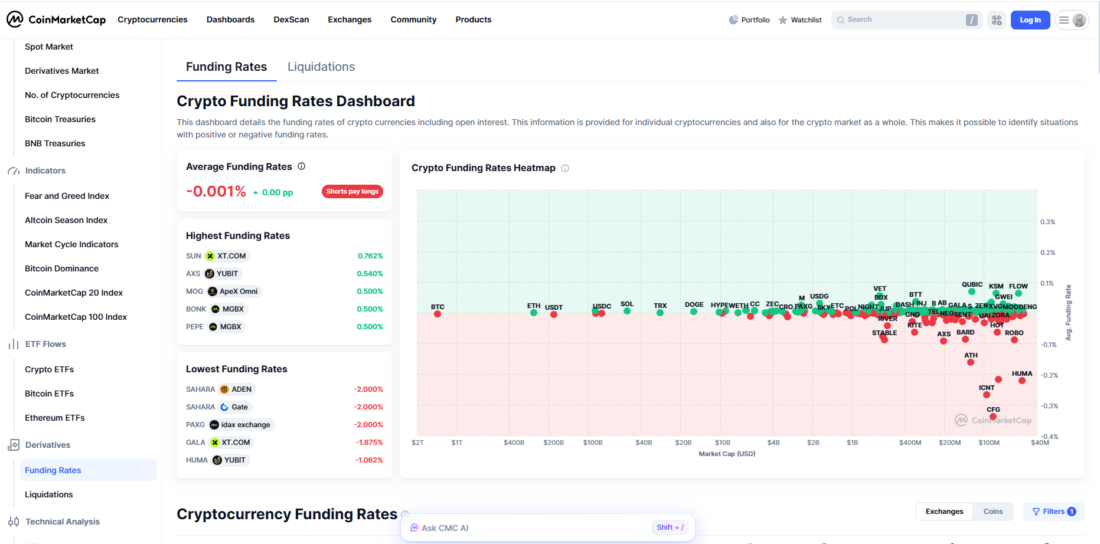

First, let us mention Coinmarketcap. On the page, you can immediately see which instruments currently have the highest and lowest funding rates. In addition, you can compare funding rates on the major crypto exchanges, which makes it possible to consider opening opposite positions on different platforms.

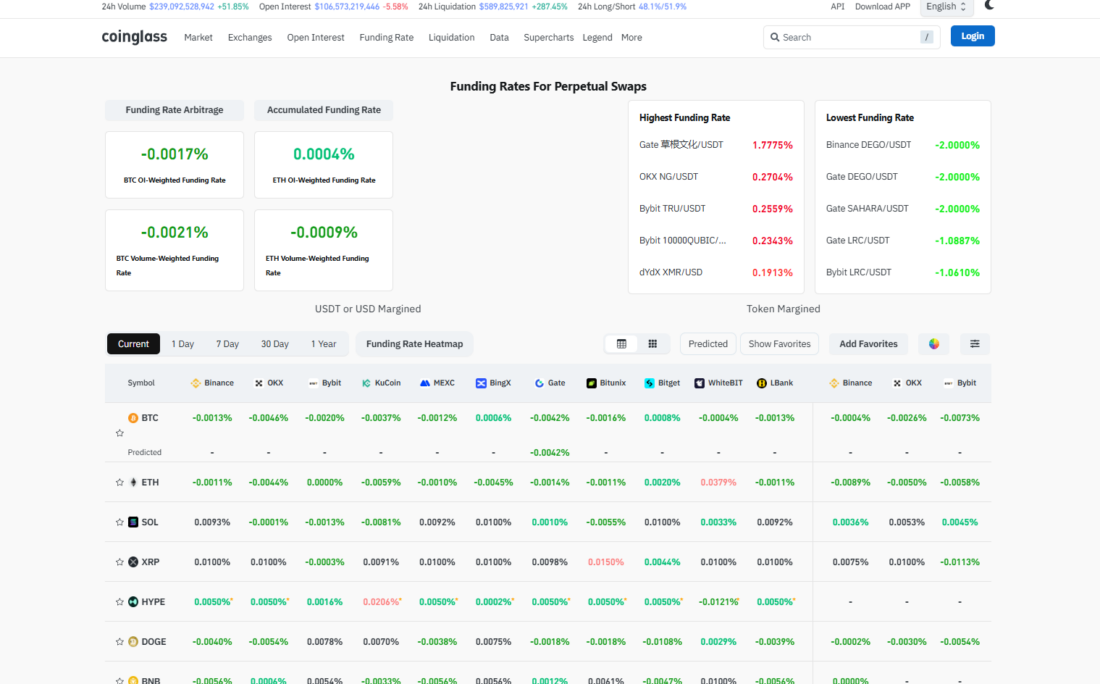

Coinglass provides similar information as well.

It is worth noting that on this resource you can view an indicator showing the relationship between funding and open interest. It is currently at its minimum value.

The historical funding rate is also well visualized.

In our humble opinion, a valuable resource is Coinalyze. The reason is that it really shows both current and forecast funding rates in tabular form.

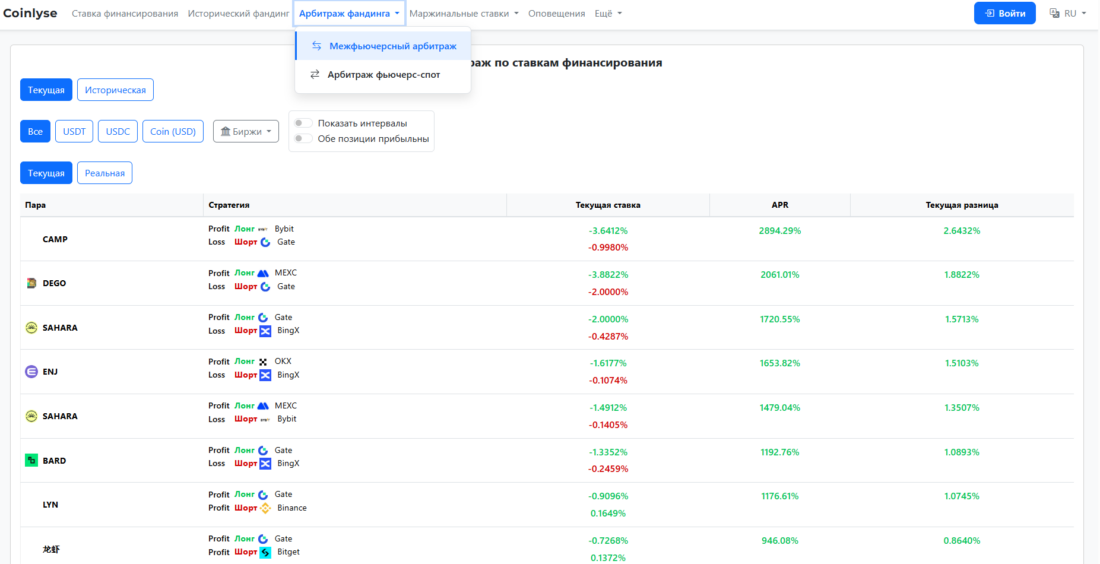

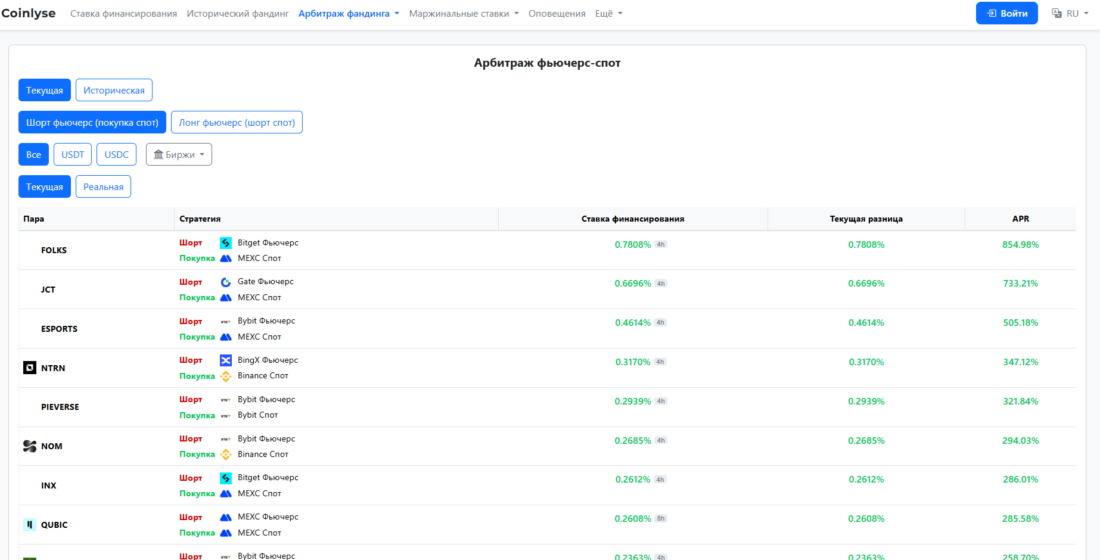

The last resource worth mentioning is Coinlyse. It is fully focused on analyzing funding rates. Its main feature is the real-time search for spot-futures and cross-exchange arbitrage opportunities.

The page for cross-exchange arbitrage (they call it inter-futures arbitrage) looks like this.

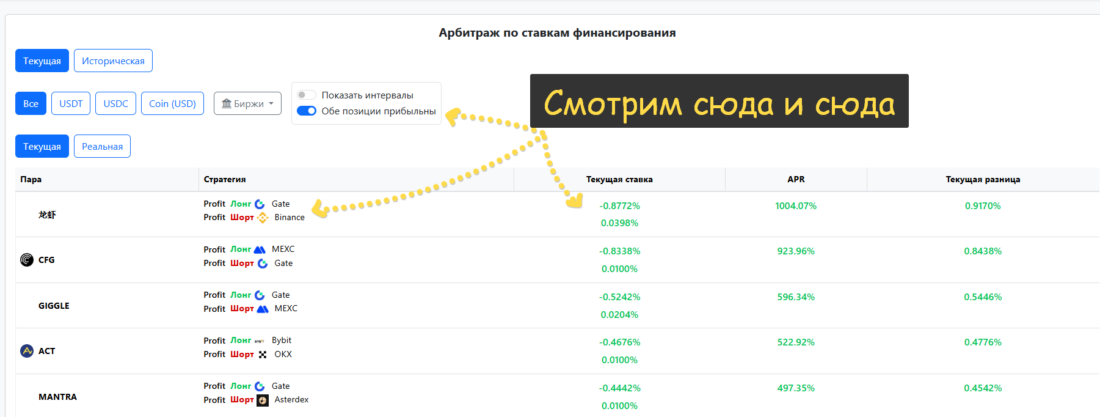

On the cross-exchange arbitrage page, we recommend studying the situations that sometimes appear on certain instruments when both selling and buying a perp on different exchanges make it possible to receive funding.

The spot-futures arbitrage page is not very different from the previous one. On this page, you can switch long/short strategies by spot or futures.

Thus, Coinlyse shows in the most visual form the aggregated information needed to study funding arbitrage.

Thus, Coinlyse provides the most visual representation of the aggregated information needed to study funding arbitrage.

Conclusion

If you want to go further (this is not investment advice), you should definitely remember the accompanying risks, because the strategy is not risk-free.

This includes the risks of position liquidation in the event of an incorrect margin calculation, the risks of a funding-rate change after which the trader turns from a recipient into a payer, and the risk of a spread change.

Besides this, one should not forget the possible delisting of perps, especially on second- and third-tier crypto exchanges. There is also an extremely high risk of unexpectedly large slippage and increased commissions there.

In addition, we must not forget about the possible delisting of perps, especially on crypto exchanges from the second and third echelons. There is also an extremely high risk of unexpectedly large slippages and increased commissions.