Calendar Spreads: A Horizontal Options Structure

Calendar spreads (also known as horizontal or time spreads) are one of the most popular and relatively safe options trading strategies.

It is ideal for new traders who want to understand how the Greeks (especially theta and vega) work without risking large sums or making large bets on the direction of the market. Unlike vertical spreads (where the difference is in strikes), here the emphasis is on the difference in expiration dates for the same strike.

In other words, a calendar spread allows you to make a profit even in sideways price movements, using the difference in time until the options expire.

In this article, we will look in detail at what a calendar spread is, how it works, what types there are, and how to apply it in practice.

What is a calendar (horizontal) spread?

A calendar spread (also known as a horizontal or time spread) is an options strategy in which a trader simultaneously buys and sells two options of the same type (call or put) on the same underlying asset (stock, index, futures, cryptocurrency) with the same strike price, but with different expiration dates. Typically, a front-month option is sold and a back-month option is bought.

The basic idea is to profit from the difference in time decay rates between options with different expirations.

Unlike vertical spreads, where options have different strike prices but the same expiration date, calendar spreads use different expiration dates with the same strike price. That is why they are often called “horizontal” - in the chain of options the expiration dates are located horizontally.

How does a calendar spread work?

The strategy is based on two key factors: time decay (theta) and volatility (vega).

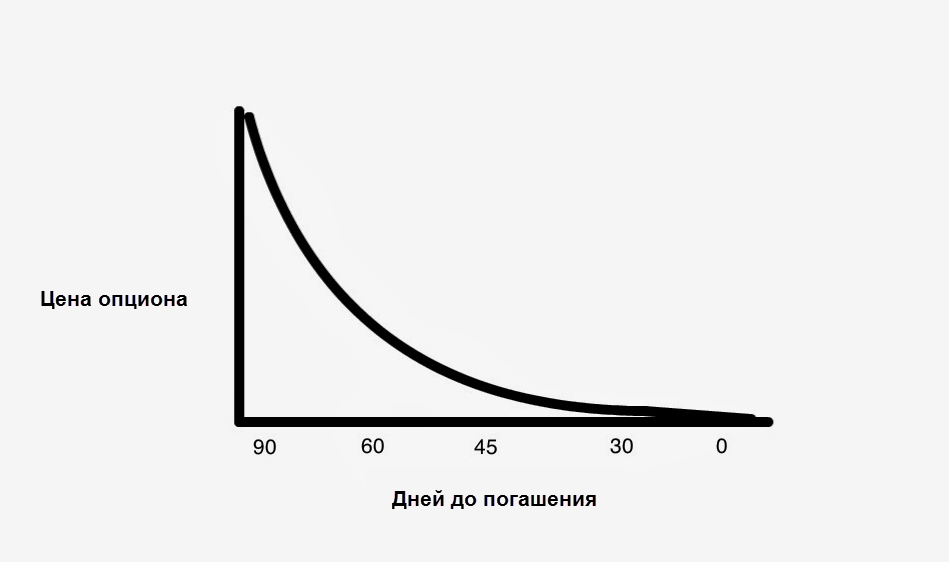

Time decay (Theta). The value of an option consists of intrinsic value and time value. Time value decreases as the expiration date approaches, and this process accelerates in the final weeks before expiration. In a calendar spread, the trader sells a short-term option that loses time value faster than the long-term option they bought. The difference in the decay rate is the source of potential profit.

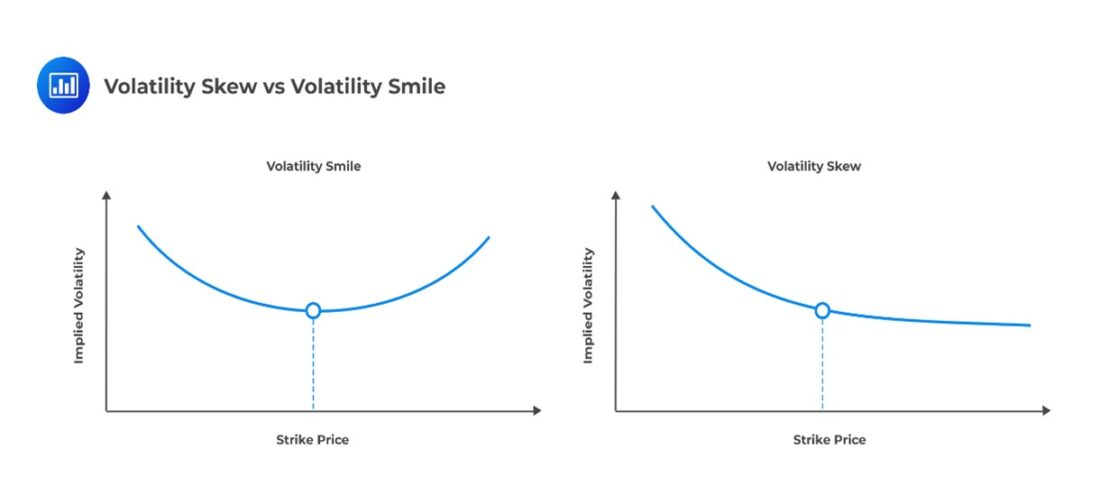

Volatility (Vega). Long-term options are more sensitive to changes in volatility than short-term options. If volatility increases, the value of the long-dated option rises more, which benefits the holder of a long calendar spread. That is why the strategy is often used during periods of low volatility, with the expectation that it will increase.

Comparison with other spreads

| Column 1 | Column 2 | Column 3 |

|---|---|---|

| Characteristic | Calendar (horizontal) spread | Vertical spread |

| Strikes | Identical | Different |

| Expiration dates | Different | Identical |

| Main source of profit | Difference in Temporal Decay Rate | Difference in execution price |

| Impact of volatility | High | Moderate |

| Directional forecast | Neutral | Bullish or bearish |

A calendar spread is also different from a diagonal spread, which uses different strike prices and different expiration dates.

Types of calendar spreads

There are several main types of calendar spreads, each suited to specific market conditions.

Long Calendar Spread. A trader buys a long-term option and sells a short-term option with the same strike price.

This is a debit strategy: the trader pays a net premium when opening the position. A long calendar spread works best when the price of the underlying asset remains near the strike until the short-term option expires. Since the strategy is long volatility, it benefits from rising volatility.

For a long calendar spread, the maximum loss is limited to the net debit paid to open the position, and the maximum profit is theoretically unlimited, but in practice it is achieved when the price of the underlying is exactly equal to the strike at the time of expiration of the short-term option. After this, the trader can close the position with a profit or leave the long-term option for further growth.

Short Calendar Spread. A trader sells a long-term option and buys a short-term option with the same strike price. This is a credit strategy that involves receiving a premium when opening the position. A short calendar spread is used when significant price movement is expected before the short-term option expires or when volatility is expected to decline. This is a more advanced and riskier strategy.

For a short calendar spread, the maximum loss can be significant because the trader has sold a long-term option that could greatly appreciate in value, and the maximum profit is limited by the credit premium received.

Both long and short calendar spreads can be divided into call and put spreads.

Call Calendar Spread. Involves buying and selling call options with different expiration dates. It is used with a neutral or moderately bullish outlook, when the trader expects the price to remain near the strike in the short term but may rise later.

Put Calendar Spread. Involves buying and selling put options with different expiration dates. It is used with a neutral or moderately bearish outlook, when the trader expects the price to remain near the strike in the near term but may decline later.

Sources of earnings in horizontal option structures

In the previous section, I briefly talked about what lies at the heart of making money on calendar options. In this section, we will try to understand more deeply where and why income is generated in long calendar spreads.

In a long calendar spread, the trader earns mainly from the difference in the rate of time decay (theta decay) between the short-term option sold and the long-term option bought. A secondary but important source of profit can be an increase in implied volatility (vega).

1. The main source is theta asymmetry (Time Decay Arbitrage)

The strategy is based on a mathematical fact: The time value of an option decays nonlinearly. It melts slowly when there is a lot of time before expiration, and accelerates sharply in the last 30 days of the contract's life.

The general design of a long calendar spread looks like this:

- Selling a near-term option (for example, expiring in 2 weeks)

- Buying a longer-dated option (for example, expiring in 2 months)

The mechanics of earnings are justified by the fact that the value of options decreases daily due to the time factor.

- The sold near-term option loses value quickly. The trader wants this option to fall to zero (OTM).

- The purchased longer-dated option loses value slowly. It serves as a form of "insurance" and as an asset that will retain value after the near-term option expires.

If the price of the underlying asset remains near the strike at the time of expiration of the near option:

- The short option expires out-of-the-money (OTM)—the trader keeps the entire premium received for selling it.

- The long option, although it has lost some time value, is still worth money.

At this point, the trader can close the entire position (buy back the near-term option for $0 and sell the longer-dated one). The difference between the sale price of the longer-dated option and the initial cost of creating the spread (the debit) will be the net profit. The trader earned money by "renting out" the right to sell an option for a short period while owning a longer-term asset.

2. An additional source of profit is increased volatility (Vega Exposure)

A long calendar spread has positive vega: the position becomes more valuable when the market gets nervous and implied volatility (IV) rises. This works because the longer-dated option has more time value and much greater sensitivity to volatility (vega) than the near-term option.

For example, news creates uncertainty, but the price remains in place. The near-term option rises only slightly in value (there is little time left, and vega is small). The longer-dated option becomes much more expensive (there is much more time left, and vega is high). The trader can close the spread early at a profit, even if the price has not reached the strike.

3. Rolling as a way to extract cash flow

Experienced traders do not always close the position after the near-term option expires. They use the rolling technique (Rolling the Front Month).

Imagine that the near-term option expired worthless. The trader still holds the longer-dated option they bought. They can:

- Sell another option with the same strike, but with the next expiration date (for example, the following month).

- Receive a new credit premium for it (cash into the account).

If the asset price continues to fluctuate around the strike, the trader can sell one short-term option after another (for example, 6 times in a row). The total premium collected from the short-term options sold will exceed the cost of the long-term option originally purchased. This is pure profit.

| Column 1 | Column 2 | Column 3 |

|---|---|---|

| Component of the Long Calendar Spread Strategy | Trader action | Source of income |

| Sold option (near) | Collects bonus | Rapid burning of someone else’s value (it is beneficial for the trader to see this asset depreciate to zero). |

| Bought option (long) | Pays a premium | Slowly retaining its value (protection against unexpected volatility, loss limited by premium). |

Case Study: Long Call Calendar Spread

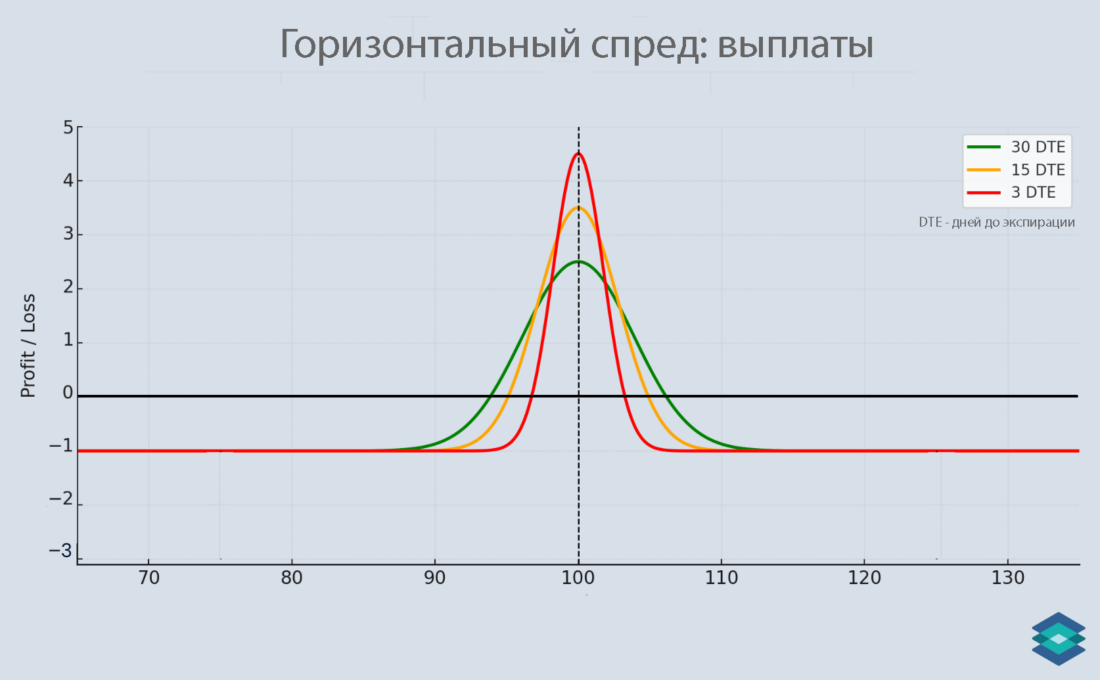

Let's say XYZ Company's stock is trading at $100. The trader expects the price to remain around $100 over the coming month, but could rise in the long term. He decides to open a long call calendar spread with a strike price of $100:

- Sells 1 XYZ call option with a strike price of $100 expiring in 1 month for a premium of $3.

- Buys 1 XYZ call option with a strike price of $100 expiring in 3 months for a premium of $6.

The net debit (cost of opening the position) is $3 per share ($6 – $3 = $3).

Scenario 1: The price remains around $100 when the short-term option expires. The short-term option expires worthless, and the trader keeps the profit from selling it. The long-term option still has time value, which means it can be sold at a profit.

Thus, in this case, the maximum profit usually occurs if the price at the time of expiration of the near option is as close as possible to the strike and IV has increased.

Scenario 2: The price moves significantly away from the strike. If the price falls sharply, the value of both options may change unpredictably. The maximum loss is limited to the net debit paid when opening the position.

Here's an example of such a scenario:

| Column 1 | Column 2 | Column 3 |

|---|---|---|

| Strike 100, price 130 | Short call (sold) | Long call |

| Intrinsic value | 30 | 30 |

| Time value | 0 | 1 |

| Total cost (no fees) | 30 | 31 |

| Lesion | -27 | 0 |

| Profit | 0 | 25 |

| Total loss | -2 |

Benefits and risks of calendar spreads

The advantages of calendar spreads include:

- Limited risk. The maximum loss is known in advance and is limited by the premium paid.

- Independence from market direction. The strategy can be profitable even in sideways movements if the price remains near the strike.

- Capital efficiency. Less margin is required than when selling naked options.

- Flexibility. Ability to select different strikes and expiration dates to adapt to market conditions.

The risks of horizontal spreads are as follows:

- Impact of volatility. A decrease in volatility could negatively impact the value of a long calendar spread.

- Significant price movement. If the price of the underlying asset deviates significantly from the strike, the strategy may cause a loss.

- Management complexity. Active position management is required, especially as the short-term option approaches expiration.

- Risk of early assignment (AssignmentRisk). A short-term American-style option may be exercised early, especially if it is in the money (ITM) and the ex-dividend date is approaching.

Conclusion

A calendar spread is a powerful tool for traders who want to diversify their strategies, avoid depending on market direction, profit in low-volatility and sideways conditions, and use options time decay to their advantage.

When trading calendar spreads, a trader does not make money from price rises or falls. The trader makes money when the price stays in place in the near term and as time passes (time decay).

If the price suddenly moves far away from the strike, then the near-term and longer-dated options will lose their usefulness (or the longer-dated one will not offset the loss on the near-term one), and the trader will take a loss limited to the premium originally paid.

Thus, a calendar options trading strategy requires an understanding of the Greeks (especially theta and vega) and active position management.