Who and How Supplies Liquidity to Forex - Liquidity Providers and Aggregators

Beginning traders face the question of choosing or changing a broker. Quite a few articles have been written on the topic of choosing a company for trading, and our website has an entire service devoted to this issue. The purpose of this article is to explain in detail one of the criteria worth paying attention to.

It will be useful for a trader to know who the broker's liquidity provider is and to understand the subtleties of order execution through Forex liquidity aggregators. Today you will learn about these providers (you have surely already heard of some companies), and we will examine how liquidity is distributed in Forex, as well as talk about some non-obvious but important points.

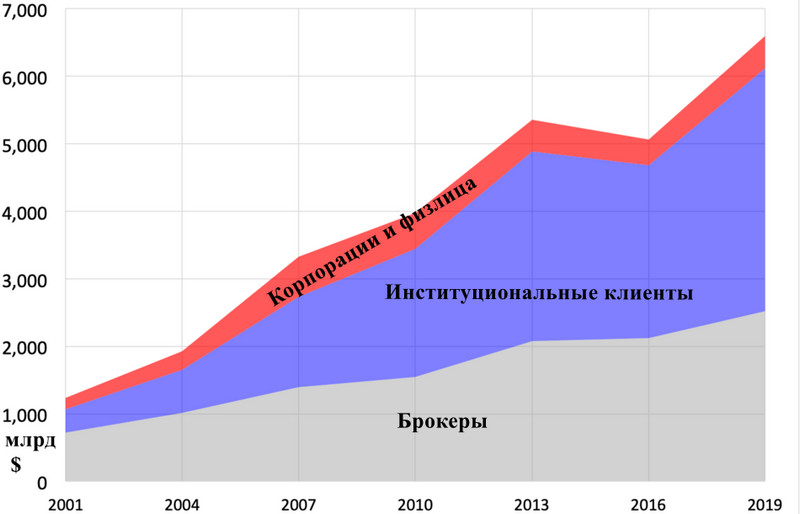

In 2020, the daily turnover of the currency market may reach the $10 trillion mark. Demand for currency trading in 2019 amounted to $6.6 trillion according to data from the Bank for International Settlements (the central bank above central banks).

For example, the US stock market trades with a turnover of $50 billion a day, which is greater than the annual volume of the Russian stock market. Any trader trading on the Moscow Exchange has practically never heard about price "slippage" even with such low trading liquidity compared with Forex.

Why then does it arise with currency brokers, while its absence is considered a distinguishing feature and an advantage of the company? It all comes down to liquidity providers or aggregators.

Distribution of Liquidity in the Forex Market

Despite the enormous liquidity of the currency market, its distribution is very uneven. The largest share of volume, about 30% of turnover in the main national currencies, is traditionally handled by the Chicago CME exchange, which has been trading currency futures since 1971.

In the US, currency derivatives were traded long before the historic decision at the Jamaica Conference, which predetermined the decentralization of Forex. Instead of a rigid peg, the exchange rate became a matter of free convertibility.

Theoretically, any financial company could offer its own rate, but in practice supply and demand were formed by large banks under the supervision of the national regulator. In this role stood the central bank, which itself often became an active player in Forex for the purpose of directly manipulating the exchange rate of the national currency.

Often for these purposes the Regulator created a national exchange; such exchanges became yet another place where currency liquidity was distributed. Large commercial banks also formed their own local markets, financing clients' conversion and trading operations.

Without having a central venue, financial organizations had to orient themselves somehow to global supply and demand. Currency futures did not provide such an opportunity because of the specifics of derivatives trading.

Thomson Reuters acted as the intermediary for collecting and processing financial information on Forex rates. The agency supplied real-time information on currency rates based on large trades by many international financial organizations, giving banks a reference point for buy and sell prices.

Thomson Reuters became one of the first suppliers of Forex quotes, later turning into a currency liquidity aggregator.

Liquidity Providers and Aggregators in the Forex Market

The second wave of Forex liquidity distribution arose with the development of electronic trading over the Internet. Forex brokers took advantage of the possibility of remotely opening accounts and organizing trading on cloud platforms. They were helped in this by the law on free currency convertibility and offshore Regulators licensing such services.

Some of the companies did not execute trades in real currency, using only the services of quote providers. This allowed brokers to earn excess profits by keeping the deposits of traders ruined by incorrect forecasts. This form of organizing trading inside the company came to be called a "bucket shop" in slang among traders.

More far-sighted companies used banking services as liquidity providers, hedging or passing clients' trades through directly. In this case the company earned on the spread. Many of the early brokers have now gained volumes that allowed them to become liquidity providers or prime brokers themselves.

Banks and prime brokers began to independently form the exchange rate for their clients, and the business of quote providers became a "rudiment," so they found a new niche. Thomson Reuters offered small clients a way around the monopoly of banking structures by pooling orders on a single online platform.

An analogue of a currency exchange was created on cloud servers, where depersonalized orders aggregated by levels were collected through gateways into the Order Book (depth of market). The liquidity of such a market was determined by the volumes of all participants. Cloud service platforms came to be called liquidity aggregators.

Brokers gained the opportunity to offer clients trading without slippage at the prices they see in the order book. Order execution was guaranteed by a third-party company, which excluded any manipulations in the interests of the forex broker.

At the current moment, two forms of access to currency liquidity have developed in the Forex market:

In this case, the broker does not send the trader's order to the interbank market, but sends it as a request to a financial institution. It is executed or adjusted at a new price, which is sent back to the trader for approval. This is slippage, and to avoid it, brokers conclude agreements with several banks or prime brokers.

The problem is that banks try to work with large firms and volumes, but small forex brokers can route orders through intermediaries, liquidity aggregators;

In effect, liquidity aggregators open a currency exchange with clearing, anonymity rules, and transparency for trading participants. The software undergoes the necessary security certifications, and currency trading is necessarily licensed by Regulators.

Additional advantages:

It is the platform's brand that helps attract the currency liquidity of large corporations;

Most modern Forex brokers operate on the NDD system in its various forms. The most common is ECN networks (Electronic Communication Network). Such platforms can be called a pure "interbank." The trader's order is sent directly into the order book and mixed there with the rest of the orders. The trading spread is determined by market supply and demand, and the broker's earnings are only the commission on trading volume.

Among them are three brokers, and this is the first nuance of the liquidity provider's work. It may offer STP accounts. In this case, all client orders will be automatically hedged by opposite trades in a narrow pool of liquidity providers, usually other brokers.

The nuances of working as a liquidity aggregator and broker in the Forex market

Most modern Forex brokers work using the NDD system in its various variants. The most common is ECN (Electronic Communication Network). Such platforms can be called “interbank” in its purest form. The trader's order is sent directly to the order book and mixed there with other orders.Spreadtrading is determined by market supply and demand, the broker’s earnings are only a commission on the trading volume.

The highest Forex liquidity is on the Chicago CME exchange. Its owners actively bought up currency liquidity aggregators for several years in a row and now own one of the largest ECN networks. Thomson Reuters also combines the liquidity of companies, banks, and brokers for currency transactions. Many prime brokers entered this business after offshore regulators began licensing ECN networks.

Despite the development of aggregators, liquidity providers will also remain in this business. Many banks have their own Forex brokers, and primes are developing a dealer network with an obligation to hedge trades.

In essence, it does not matter which of the above forms of access to currency liquidity a broker chooses; the main thing for the client is automatic order execution without company intervention. The problem arises when the dealing center's website does not provide specific information about who stands on the other side of the trade (except in cases when the size of the company allows the broker itself to be the aggregator). Assurances from a forex broker that orders go to large banks without naming them - may indicate the opposite.

Conclusion

Highest Forex liquidity onChicago CME exchange. Its owners have been actively buying currency liquidity aggregators for several years in a row and now own one of the largest ECN networks. Thomson Reuters also brings together the liquidity of companies, banks and brokers for foreign exchange transactions. Many prime brokers entered this business after ECN networks began to be licensed by offshore regulators.

Despite the development of aggregators, liquidity providers will also remain in this business. Many banks have their own Forex brokers, primes are developing a dealer network with an obligation to hedgedeals.

In fact, it does not matter which of the above forms of access to foreign exchange liquidity the broker chooses, the main thing for the client is the automatic execution of orders without the company’s intervention. The problem arises when it is impossible to find specific information on the DC website about who is on the other sidedeals(except in cases where the size of the company allows the broker to be an aggregator himself). Assurances from a forex broker that orders are sent to large banks without indicating their names–may say the opposite.

Best regards, Ivan Petrov

Tlap.io