Weak payrolls pressure the dollar, but the Fed is not yet free to maneuver

Introduction

The market received weak June payrolls and again took up its favorite activity: trying to read the Fed through macroeconomic coffee grounds. At first glance, everything is simple: employment is weaker, easing expectations are higher, the dollar is lower. But reality, as usual, carefully puts a paw on the chart: inflation remains stubborn, FOMC minutes and CPI are ahead, and regulators are not yet rushing to turn one weak report into a ready-made policy pivot.

🏦 The Fed between employment and inflation

June payrolls came out noticeably weaker than expected, and this quickly brought back market talk that the Fed will sooner or later have to ease policy. The dollar index TVC:DXY at the time of writing is at 100.9 USD and is losing -0.52% on the day, which clearly shows that traders are already repricing the probability of a softer rate path. But for the Fed, a weak labor market is not an automatic pass to a rate cut. The regulator still needs to take into account persistent inflation, the possible impact of tariffs on prices, and the risk of premature easing if core price pressure has not cooled convincingly enough. Therefore, the market's base case now looks cautious: in July, most likely no move, while sensitivity to every new CPI and to the wording in the FOMC minutes rises sharply. A weak labor market pressures the dollar, but one employment report is not enough for the Fed to sharply change course. For traders, this means the main focus is shifting from the fact of weak payrolls itself to how the Fed explains the balance between employment and inflation. The next CPI and FOMC minutes become key triggers for rates, bonds, and currencies, because they will show whether the regulator sees the start of sustained economic cooling or only one unpleasant statistical episode.

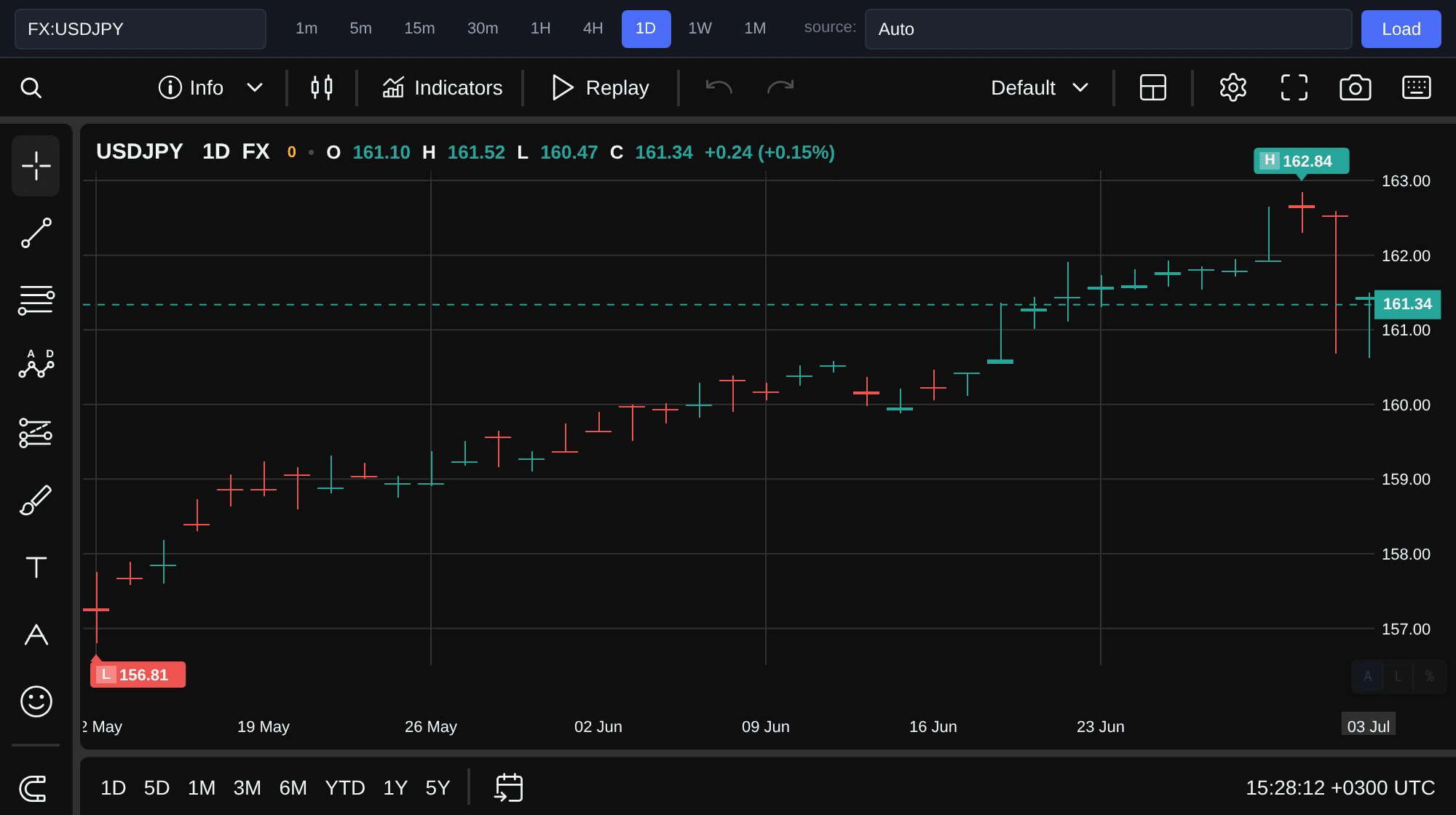

💴 Yen and carry trade: a thin wire above rates

USD/JPY remains in a tense zone: the pair is trading around 161.3 JPY, with a daily change of -0.07%. At the same time, the DXY dollar index fell to 100.9 USD and is losing -0.52%, meaning the dollar has generally softened, but the yen has not received strong relief. The reason is the same: the rate differential continues to support the carry trade. As long as the yield on dollar assets looks more attractive and Japanese rates remain significantly lower, the market keeps an incentive to hold long dollar positions against the yen, even if nervousness around these positions is growing. But at such USD/JPY levels, it can no longer be viewed only as a calm story about rates. The carry trade remains alive, but with USD/JPY at 161.3 JPY, the market is already trading not only rates but also the risk of a sudden administrative signal. This does not mean intervention is inevitable: confidently promising it would be too bold even for the most self-confident terminal. But the longer the pair stays in the zone of heightened attention, the stronger the reaction to a tough comment from Japan's Ministry of Finance or to any shift in Fed expectations that can quickly knock leverage out of carry positions.

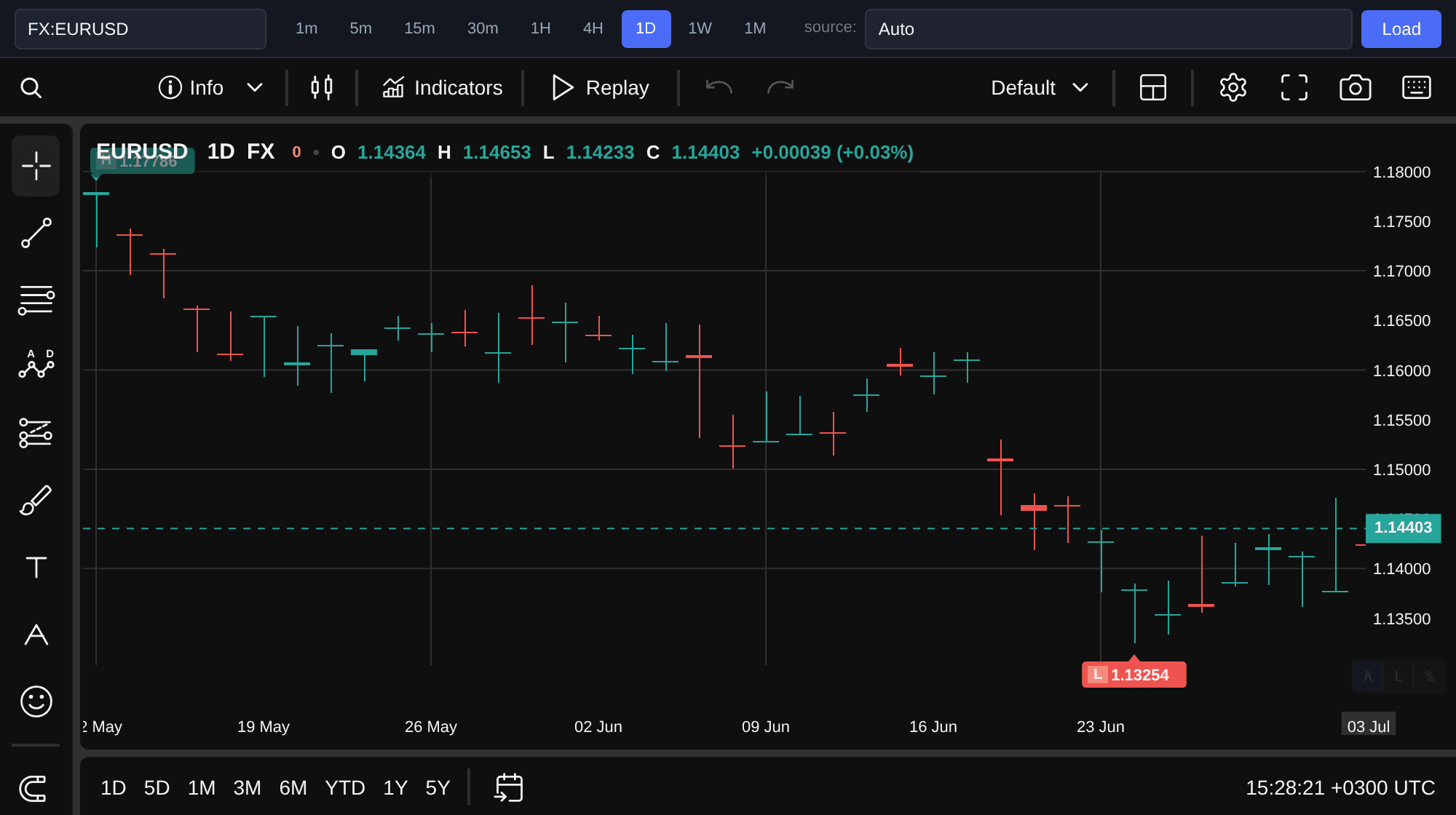

💶 EUR/USD: the euro uses dollar weakness, but without euphoria

EUR/USD rose to 1.14 USD, adding +0.15% on the day, and this move logically fits into the overall reaction to weak U.S. employment data. When the market starts pricing in a softer Fed, the euro often becomes a convenient instrument for bets against the dollar. However, the pair's rise so far does not look like the unconditional start of a new sustainable trend. For the move to become stronger, the market needs to see confirmation of slowing U.S. inflation and more convincing European macro statistics; otherwise, buying the euro will remain primarily a mirror of selling the dollar. EUR/USD is getting support from the weak dollar, but euro buyers still need confirmation from CPI and European data. Without this, the pair may look confident on the chart, but the fundamental base under the move will remain thin. If the nearest U.S. inflation statistics again force the Fed to speak cautiously, EUR/USD may quickly lose part of its momentum. Therefore, the current rise is important for the short-term picture, but for now it is more reasonable to interpret it as a constructive rebound rather than the market's final transition into a sustained euro-buying phase.

📌 What the day really changed

The main change of the day is not that the dollar capitulated, but that the market rebuilt expectations for the Fed's further actions. DXY at 100.9 USD and a daily decline of -0.52% show real pressure on the U.S. currency, but inflation risks still prevent the regulator from quickly moving to easing. The yen remains the most nervous part of the currency picture, because USD/JPY around 161.3 JPY still keeps the risk of verbal or real signals from Japanese authorities on the agenda. At the same time, the pair's daily change is only -0.07%, which underlines the resilience of the carry trade even against a weaker dollar. EUR/USD at 1.14 USD and up +0.15% reflects dollar weakening after payrolls, but does not yet prove independent euro strength. The market has entered a phase of heightened sensitivity to every new inflation and labor signal. Until CPI, the FOMC minutes, and new regulator comments, sharp moves may be noisy and emotional, but not necessarily sustainable. For a trader, this is an environment where it is more important not to guess the headline of the next news item, but to understand which scenario is already priced in and exactly what can break it.

Conclusion

The day's result is quite practical: weak payrolls made the dollar more vulnerable, but did not give the market a clean signal for immediate Fed easing. DXY fell to 100.9 USD and lost -0.52%, EUR/USD rose to 1.14 USD, while USD/JPY remained around 161.3 JPY, maintaining tension around the carry trade and the risk of intervention signals. Until inflation and Fed communication confirm a pivot, moves in the major currency pairs should be seen as an important repricing of expectations, but not as the final verdict on the next trend. Practical takeaway for a Forex trader: the rule should be tested on a demo account, written into the trading plan, and applied consistently before every trade. Practical takeaway for a Forex trader: the rule should be tested on a demo account, written into the trading plan, and applied consistently before every trade. Practical takeaway for a Forex trader: the rule should be tested on a demo account, written into the trading plan, and applied consistently before every trade. Practical takeaway for a Forex trader: the rule should be tested on a demo account, written into the trading plan, and applied consistently before every trade. Practical takeaway for a Forex trader: the rule should be tested on a demo account, written into the trading plan, and applied consistently before every trade. Practical takeaway for a Forex trader: the rule should be tested on a demo account, written into the trading plan, and applied consistently before every trade. Practical takeaway for a Forex trader: the rule should be tested on a demo account, written into the trading plan, and applied consistently before every trade. Practical takeaway for a Forex trader: the rule should be tested on a demo account, written into the trading plan, and applied consistently before every trade.