TWAP: a professional algorithm for placing large orders

The foundation on which the discipline of large capital rests has remained unchanged for several decades. We are talking about a strategy without which large-scale trading is impossible: TWAP.

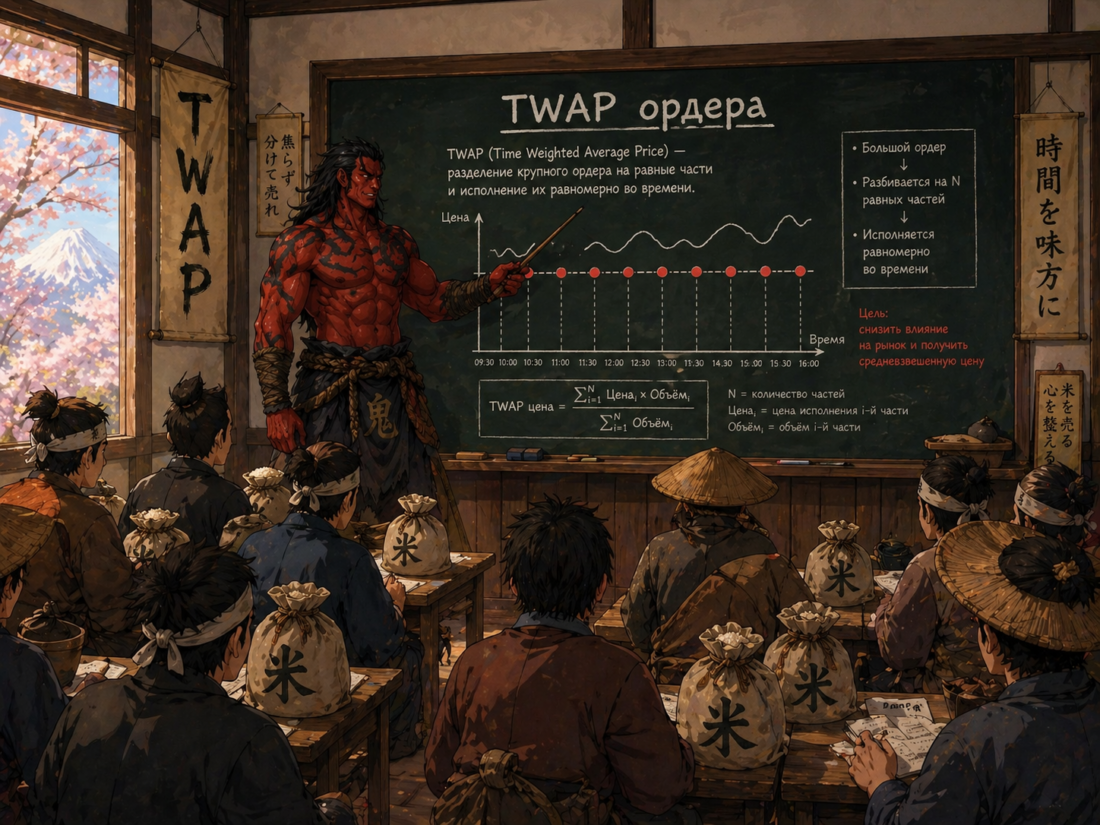

TWAP stands for Time-Weighted Average Price. The point of the strategy is to split a large order into several small ones and execute them at equal time intervals.

For example, a trader wants to buy 1000 shares. Instead of buying them all at once, he can:

- split the volume into 10 parts,

- buy 100 shares every 5 minutes,

- stretch the execution over 50 minutes.

This approach makes it possible not to "spook" the market and not to cause a sharp price jump with a single large order.

Simply put, TWAP is not a "magic indicator" that shows where price will go. It is an order execution algorithm. Its task is much more practical: to buy or sell a large volume not in one blow, but evenly over time, in order to reduce the trade's impact on the market.

For a beginner trader, TWAP is especially useful as a way to understand an important thing: not only what to buy or sell, but also exactly how to execute a trade so as not to ruin your entry with one large market order.

This material is for informational purposes, cannot and should not be regarded as a consultation or advice.

What TWAP is in simple terms

TWAP as a concept arose from the need of institutional market participants to execute large orders carefully and unobtrusively.

In practice, TWAP began to be actively used with the development of:

- electronic trading systems,

- algorithmic trading,

- high-liquidity markets,

- infrastructure where orders can be quickly split and sent automatically.

In other words, TWAP is a product of modern market mechanics, not a classic indicator from a technical analysis textbook.

TWAP is not a single patented indicator, but rather an execution method that developed together with electronic markets and algorithmic trading.

To understand TWAP, let us imagine a situation in which a trader wants to buy a large block of shares (for example, 1000 units), where:

- The stock price changes every second.

- The DOM book is "half-empty," and the total volume of sellers' limit liquidity in the book over the next 50 ticks is exactly 1000 shares.

If you buy everything at once with a single order, the price will rise sharply by 50 ticks. At the same time, the average position may shift closer to the highs, since there is more limit supply there.

If you buy evenly instead (in portions), the probability of a strong market impact is lower. This is exactly the problem TWAP solves, aiming to make the average execution price of the trade close to the average market price over the selected period (VWAP).

For example, if the price stayed within a range for an hour, the TWAP order placement algorithm does not try to guess the top or the bottom. It tries to execute the order evenly so that the result is "fair" and predictable.

Therefore, it is important to watch the cluster zones of the greatest demand and supply (cores), since that is exactly where large capital places its medium-term and long-term liquidity.

How a TWAP order works

The mechanics of TWAP orders are simple:

- The total trade volume is determined (for example, 5000 contracts need to be sold).

- A time interval is set (execution time is 100 minutes).

- The volume is divided into equal parts (500 contracts are placed every 10 minutes).

- The order is executed in parts at equal time intervals.

In a more advanced version, the algorithm may take into account:

- allowable price deviation,

- minimum volume in the order book,

- pauses during high volatility,

- limits based on the trading session time.

But the basic logic always remains the same: an even distribution of execution over time.

TWAP is most often used where there is large volume and careful execution matters: stocks, futures, cryptocurrencies, currency pairs, and less liquid instruments if the trade volume is noticeable.

Advantages of TWAP orders

Minimization of market impact. A large order split into 50-100 micro-orders is executed almost invisibly to the market. This allows institutions to enter positions without provoking a price spike that would worsen the average execution price.

Reduction of slippage. Slippage is the difference between the expected trade price and the actual execution price. Algorithmic order splitting and time-based execution significantly reduce this spread, especially on low-liquidity instruments.

Simplicity of implementation and use. Unlike VWAP, which requires complex forecasting models for the intraday liquidity curve, TWAP can be implemented with a few lines of Python code. In exchange interfaces, to create a TWAP order it is enough to specify the volume, side, and duration - the system does everything else by itself.

Strategy masking. No one will notice your real volume. The market sees only a series of small orders, and competitors cannot determine whether accumulation is continuing or whether it is just retail noise.

Disadvantages and risks of TWAP orders

The main risks of the TWAP order placement strategy are as follows:

Risk of adverse price movement. While the order is being executed in parts, the market may move against the trader. This is especially dangerous on news or during bursts of volatility.

Risk of incomplete or prolonged execution. The longer the execution lasts, the more factors can interfere: news, volume spikes, sharp impulses, and changes in market sentiment.

Risk of a false sense of safety. A beginner may think that TWAP "smooths everything out." But it does not protect against a bad idea. If the entry is wrong from the start, splitting the order will not save it.

Risk of missing a favorable moment. If the market moves sharply and quickly, even execution can make the average price worse than a single fast entry.

Technical risks. If the strategy is automated, the risks of terminal failure, execution delays, errors in the algorithm logic, and problems with the exchange or broker API are added.

The main disadvantages of TWAP include:

Ignoring volume. TWAP does not see how much is actually traded at each moment in time. If the algorithm executes orders during a period of low liquidity (for example, the Asian session for BTC), even a small sub-order can cause a noticeable price shift.

Does not take market context into account. TWAP simply executes orders by time. It does not "understand" that the price has sharply moved in the right direction or, on the contrary, is about to fall. Because of this, the algorithm may buy more expensively than it could have or sell more cheaply than the trader would like.

Not the best choice in a strong trend. If the market moves quickly in the right direction, stretched execution may worsen the result. For example, when buying, the price may keep moving upward, and later parts of the order will be more expensive.

Can lose to smarter algorithms. There are more advanced execution methods that analyze liquidity, volatility, and order book behavior. Against their background, TWAP looks rough and straightforward.

When you should not use TWAP orders

TWAP is not universal. It is not suitable if:

- instant entry or exit is needed,

- the market is extremely volatile and speed matters,

- the trade is small and splitting makes no sense,

- a strong impulse is expected after the news,

- liquidity is high enough to execute the order immediately without noticeable slippage.

Sometimes a simple market or limit order will be better than any splitting algorithm.

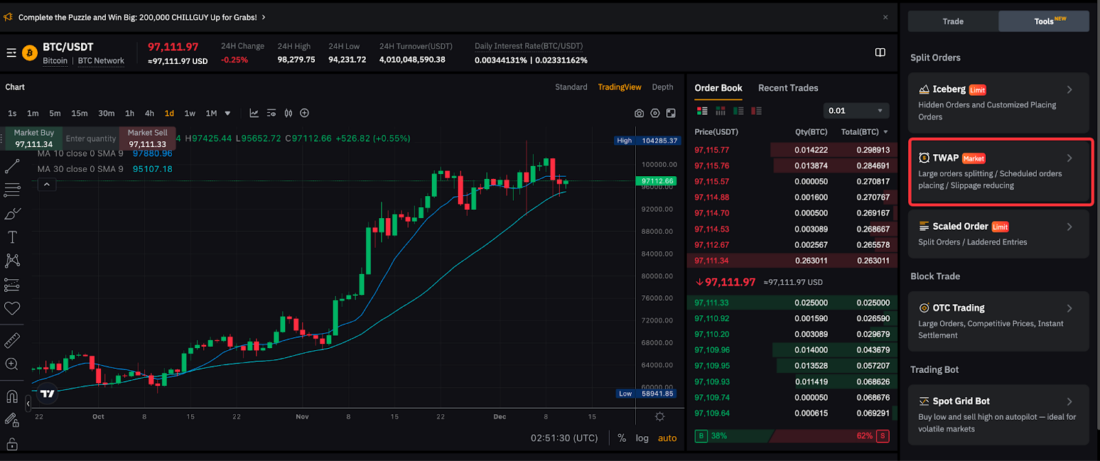

Setting up TWAP orders on Bybit

On the Bybit crypto exchange, every trader can set up the placement of TWAP orders.

First, you need to click "Tools" in the order area and select TWAP.

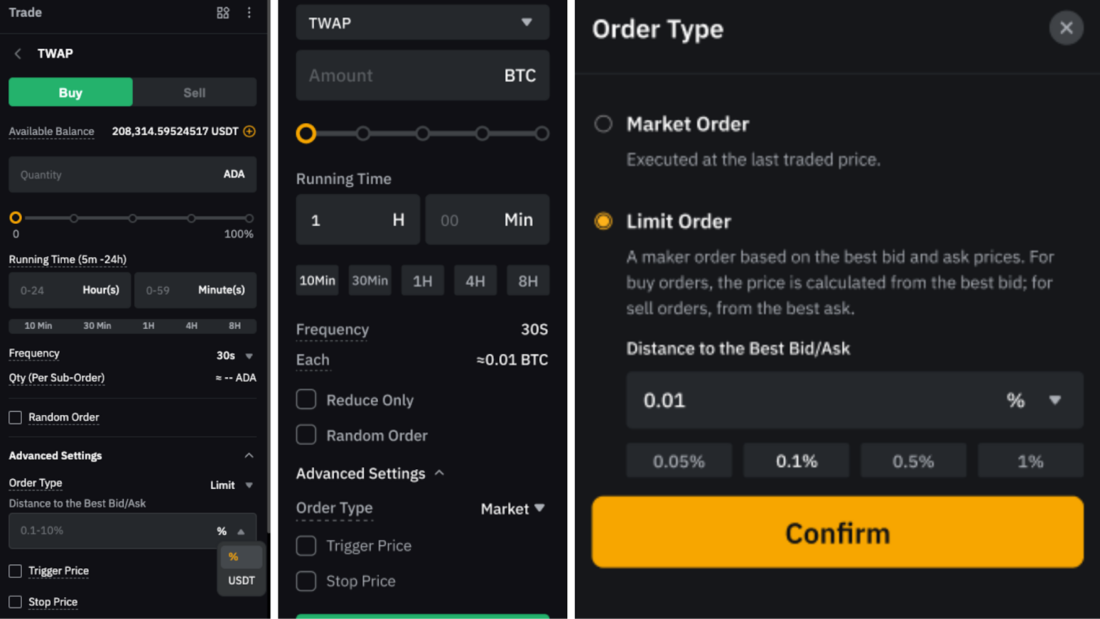

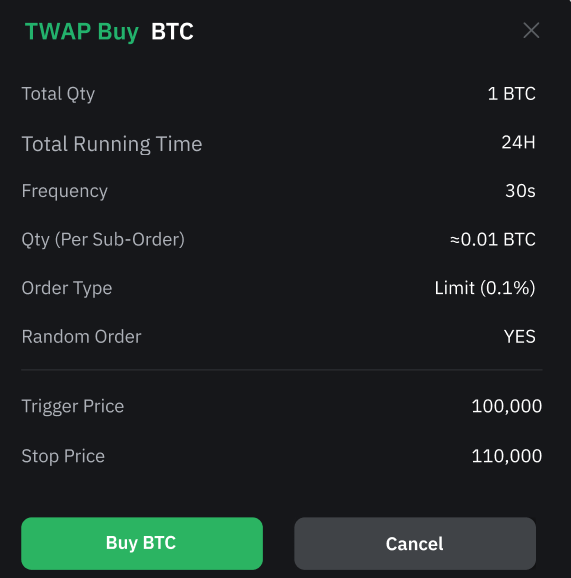

After that, you need to create a TWAP order by specifying the parameters: time interval, order type (market or limit), frequency, quantity, and so on.

After that, you need to confirm the settings, check the parameters once again, and place the TWAP order on Bybit.

Methods of applying TWAP: from institutional execution to retail trading

Method No. 1: Algorithmic execution of large orders

This is the main method of using TWAP to open orders.

If an institutional investor needs to enter or exit a position without crashing the market, the TWAP algorithm splits the order into many micro-orders.

On modern crypto exchanges, this is implemented directly in the interface: you only need to choose TWAP, specify the parameters, after which the system itself will place limit or market sub-orders at the specified periodicity.

An important tactical technique is randomization. Experienced algo traders never use strictly identical intervals and sub-order volumes. The algorithm is programmed to randomly vary the order size and the pauses between them within set limits. This is needed so that competitors and high-frequency robots cannot "read" your strategy and get ahead of you.

Method No. 2: Accumulation/distribution strategy

This method is called "quiet accumulation." Instead of placing noticeable limit orders at specific levels, the trader uses TWAP to gradually distribute the position over several hours or even days.

For example, in 2025 the DeFi project World Liberty Financial acquired $4.7 million worth of cryptocurrency using TWAP orders specifically. The goal was not simply to "buy the market," but to build a position with surgical precision while remaining unnoticed by other large players until the very last moment.

Another example. In May 2025, on-chain analysts recorded how Binance accumulated BTC and ETH through TWAP orders with minimal market impact, while at the same time Bybit, through the same mechanism, exited positions in HYPE and DOGE and rotated into SOL.

Method No. 3: TWAP as a filter in trading systems

This is a method for retail traders. A daily or weekly TWAP is used as a dynamic filter to determine trend direction and search for entry points:

- If the price is above TWAP, the trend is considered upward, and we look only for longs;

- If the price is below TWAP, the trend is downward, only shorts;

- A break of TWAP from top to bottom is a signal of a possible trend change.

For example, in crypto trading the "TWAP filter" is popular: entering a position is allowed only if the asset price is more than 20% below the weekly TWAP, which automatically filters out entry points at peaks of hype and market overheating.

Conclusion

An ordinary trader often thinks like this: "I'll buy now while it's cheap." The TWAP algorithm "thinks" differently: "I need volume, and I want to take it in a way that minimizes slippage and market footprint."

TWAP is more about execution than forecasting.

On most instruments, TWAP is interesting only to large traders, but if we are talking about illiquid and inexpensive crypto coins, then the TWAP algorithm will also suit an ordinary trader who wants to place a position that is relatively large for that instrument without being noticed by other participants.

Strengths and weaknesses of TWAP

| Advantages | Disadvantages and risks |

|---|---|

| Minimizing market impact | Ignores trading volumes |

| Reduced slippage | Predictability for HFT robots |

| Simplicity and speed of setup | Sensitivity to volatility |

| Disguise from competitors | Risk of incomplete execution |

| Resistance to manipulation | Slow execution - lost profits |