The wonders of fixed fractions: how to never drain your deposit

Greetings ladies and gentlemen traders!

Today we are going to continue the topic of capital management of your accounts and talk about the most common and most often recommended method of capital management for leveraged instruments, i.e. traded on margin – the fixed-fraction method. The fact is that small improvements to the classic method will allow you to almost never drain your accounts.

In fact, this is probably the only money management method we know from various books and resources on the web. That said, most trading books tend to devote only one chapter to money management, with recommendations on what to use. And there is no explanation of the possible consequences, pros and cons of this or that approach.

Meanwhile, there is no ideal method of money management, which would be perfectly suitable for use with a wide range of trading systems. Today we will continue to talk about the methods of money management and get acquainted with the most widespread of them, as well as consider the advantages, disadvantages and different variations of the fixed-fractional method of money management.

Classic variant of the fixed-fractional method

The classic variant tells us that each trade can be risked with an amount not exceeding X% of the balance or equity of the account. This is the most widely used money management technique, both among professional financial managers and ordinary private traders. It is also often referred to as the fixed share method because it is the percentage of capital that is used.

Under this method, you simply risk X % of your money in each trade. For example, you are trading the fixed-fraction method, using 2% of your deposit in each trade. Your deposit is $1,200 and your stop loss (maximum loss) is 100 pips or 1,000 pips. For simplicity, let’s assume that the price of a pip is equal to $1 with a lot of 1. Then our lot, which we will enter the deal, will be 1200*2%/(1000*1) = 0.024 or 0.02 lot.

There is also often a modification where the maximum loss is taken instead of the stop loss value. The point is that many trading systems have rules for exiting trades in the loss zone and it often happens that getting a full stop-loss is extremely unlikely. Therefore, in order not to underestimate the risks and not to limit artificially the growth of capital in the system, they take the maximum loss according to the results of testing (for example, according to the results of 1000 deals, the maximum loss on a deal was 80 points) and use it in calculations. And the real stop-loss is either not used at all, or put it with a decent reserve.

It is always worth remembering that the market is the market and even when something seems extremely unlikely, it is still bound to happen sooner or later. Therefore, even if you decide to use such a variant of lot calculation, do not artificially increase the size of stops and certainly do not remove them altogether. At the critical moment, albeit with a large slippage, but your deal will be closed and at adequate risk levels you will not lose much.

Lot rounding rules for the fixed-fraction method

In the above case, as a result of rounding we could not set the risk at exactly 2% and we use the risk (0.02*1000/1200)*100% = 1.67%. When the account increases up to 1500$ with our set risk of 2% – we will be able to enter the market with 0.03 lot. In this case the risk will be exactly 2%. But from the deposit level of 1300$ we could round the resulting lot according to standard rounding rules (i.e. at 0.025 we would round up to 0.03), but in this case the actual risk would be already 2.31%, which is much higher than the specified 2%. Therefore, in my opinion, it is more correct to always round down, so as not to risk unnecessary money.

Classical fixed-fraction method and trading statistics

As you understand very well, the calculation of risk for the next trade in this approach is made without any reference to the account statistics. No matter how the market is at the current moment, no matter how effective or ineffective your strategy is, the risks for the next trade remain unchanged. This is the essence of this method and despite the fact that almost every trader uses it in his trading, it is difficult to call this approach effective.

One lot for every X units of currency on the account

This method is just a slightly modified variation of the classic method. It is called pure fixed fraction. The idea here is that for every, for example, one hundred dollars on your balance, you add a minimum lot unit. For example, your balance is $1,200, and you add 0.01 lot for every $500 in your account. Then you would enter each trade with 0.02 lot until the account grows to $1,500. Then you will work with 0.03 lot all the way up to the $2,000 balance mark.

Below you can see the chart of the trading system with 58% profitable trades and a 1 to 1 ratio of profit to loss (excluding trading costs):

Same system with a risk of 3% of deposit per trade:

Same system, but with a risk of one minimum lot for every $200 of deposit:

Despite the slightly more modest profit margins of the last option, its maximum drawdown is significantly lower and the yield curve is smoother.

This can be more clearly appreciated when trades generate different amounts of profit or loss:

If you examine these two charts more closely, you will see the advantages of the second method. This is especially evident in the drawdown around trades 900-950 – it really is decently less than with the classic fixed-fraction method.

Nevertheless, the method of one lot for every X units of currency on the account also has a number of disadvantages. It also does not take into account trading statistics at all and prescribes to always calculate the lot based only on the size of the account. Also, this method does not take into account the fact that the value of profits and losses can be different from one trade to another.

Also, this method of lot calculation does not take into account the real value of the possible maximum loss. That is, if when selecting the lot size according to the test results, it does not include cases of closing by stop-loss, you still have a chance to get this very stop-loss in the future and it will be sad if it will be four times higher than the average loss.

It is quite real situation when your average loss is, for example, 2%, because you close usually on the signal of the system without waiting for a full stop, but there comes a moment when due to, for example, too fast reaction of the market to the fundamentals, the deal is closed exactly on a full stop and you get a loss of 10%.

Well, the last but very important disadvantage is that you need to get 100% profit to switch from one to two minimum lots at the initial stage. For example, you need to have $500 to trade 0.01 lot to keep the maximum drawdown around 20%. Then you need to make $500 or 100% of your initial deposit to trade 0.02 lot. The next move will happen already at 50% profit. Then at 33%. In the end, after each trade you will have to increase the lotness by several minimum lot units. But the very first transition requires 100% profit.

The big problem will arise if you try to reduce the huge period of time it takes to switch from 0.01 lot trading to 0.02 lot trading. The only way to increase the speed here is to increase the risk percentage (which is especially dangerous with a small account size).

Disadvantages of both methods

The main disadvantage is the need to work with the same lot for a very long time before moving “to the next level”. This disadvantage applies to both methods, but it is more obvious in the latter one. For example, if you trade 0.01 lot for every 500$ on your deposit, you can trade 0.01 lot for a whole year until your deposit is equal to 1 000$. During this entire period between moves to new levels you are essentially working with a fixed lot and deprive your account of the effect of “geometric growth”, or at least, greatly stretch this effect.

When increasing the risk level, this disadvantage can be mitigated a bit, but here another significant disadvantage comes out. If you think that the rate of account growth under the geometric model corresponds to the rate of decline, you are mistaken. Unfortunately, the rate of decline exceeds the rate of growth.

For example, in order to grow your account as fast as possible, you decide to use the optimal f method, which involves trading with a high percentage of risk, usually 10 to 20% per trade. Let’s assume that your system will always produce either a profit of 10% of your deposit or the same loss. Then with a deposit of $1,000 and a risk of 10%, you will win $100 in the first trade and get $1,100 on deposit. In case the next trade will be unprofitable, you will risk $110 and get $990 on your account as a result.

Thus, in both deals you risked ten percent of the account and received a loss of 10$, but not 0$. At the same time, the higher the risk, the stronger this effect is. This is called leverage asymmetry, which is characteristic of all instruments traded on margin. All this sadness can be clearly demonstrated by this table:

As you can see, already at a risk of 5% this effect starts to affect your account. That is why you need to decide at once what is more important for you – to strengthen the effect of geometric growth (and at the same time the account drawdowns will increase significantly), or to preserve and maximize the safety of your initial capital.

Unfortunately, there is no method that would allow you to reliably realize both of these goals, but there are some techniques that will allow you to take a small bite from both of these pies. But we’ll talk about them a bit below, and now let’s break down these two basic approaches – increasing the effect of geometric growth and protecting profits.

Modifications to the decline rate method

But, again, it should be understood that this approach shows itself best with a large number of losing trades in a row, otherwise the effect of this method is almost imperceptible. Therefore, its modifications are often used.

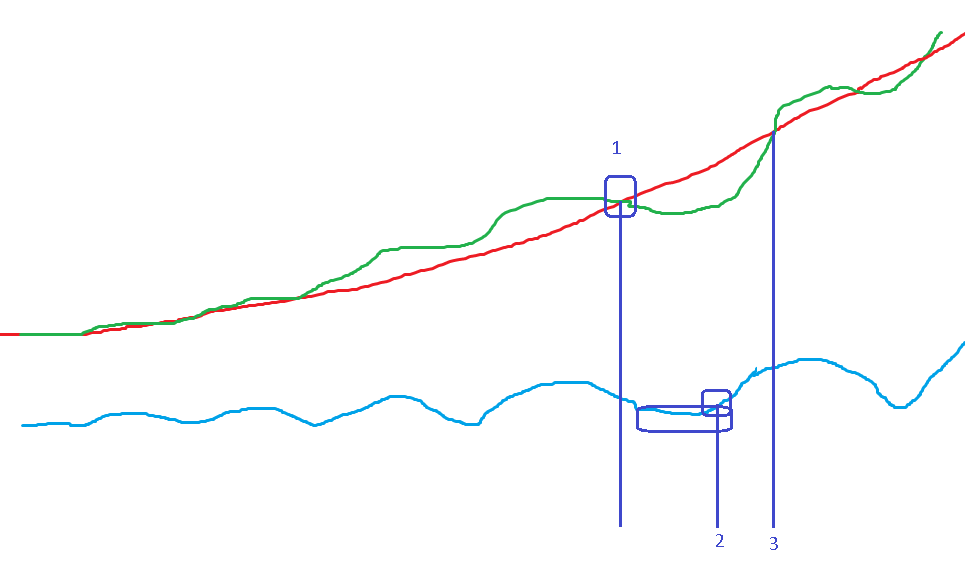

One of such modifications is the system balance curve. A moving average of the deposit balance is built and when the current balance is below the moving average, the rate of decrease is applied until the balance is above the curve. When the balance crosses its moving average, you can again switch to the standard calculation of the lot rate. There is a disadvantage here too – the further we have managed to deviate from the moving average, the more difficult it will be to return back to the moving average if the lot is decreasing. That is why it is worth adding a balance oscillator to the moving average, thus obtaining a trend system:

At point 1, when the balance line (green line) crosses the moving average line (red line), we start applying a decreasing bet until we are at point 2. At point 2, the oscillator calculated by the balance line readings comes out of oversold condition and we gradually start to increase the lot until we are at point 3. At point 3, the balance chart is again above the moving average and we again calculate the lot based on the usual logic accepted in the system.

This approach allows us to reduce drawdowns during periods of balance reduction (unfavorable market conditions for our system), as well as to return to the initial lot faster. With this approach, a high drawdown rate is not only not harmful for getting back to the initial lot, but even turns out to be useful – we can set the drawdown rate, for example, 0.7, and the upside rate (increase in the lot size when the oscillator grows) at 1.5.

Thus, we will reduce balance losses quite rapidly and get out of drawdowns even more rapidly. This is true when the oscillator continues to grow from the oversold level, but if the breakdown of the level was false and the next trade turns out to be unprofitable, we will find ourselves in an even greater drawdown, because we entered with an increased lot. Therefore, it is worth to apply the betting method with caution and thoroughly test the system on history.

Acceleration of geometric progression growth

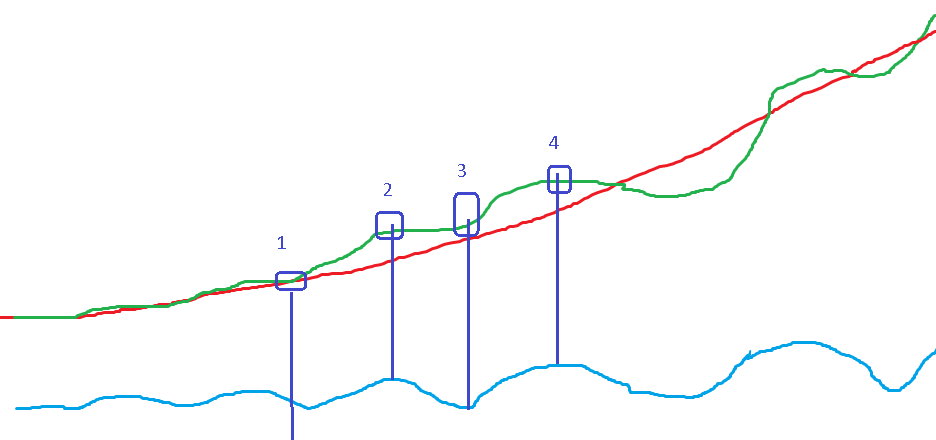

In the previous example, we decreased the lot rate faster than it would have been with a normal money management method, for example, using 2% of the deposit in each trade. But who will stop us from increasing the lot rate when the balance line is above its moving average and the oscillator is rising? So, for example, according to our system we should risk 2% in each trade. At the same time, under the right conditions (moving average and oscillator growth, for example), we can say that at the moment our system is in “good shape” and works in harmony with the market conditions. Then why not increase the lot after each profitable trade in such conditions? All this will increase the effect of geometric progression on the account without a significant increase in drawdowns, because we will act in this way only at favorable market phases for the trading system:

That is, as long as the balance line is above its moving average and the oscillator is growing (sections 1-2 and 3-4) we can increase the lotness in excess of the system. In the periods of oscillator decline we can trade with the basic lot, the one that is laid down in the classical rules of the system. Thus, in the most favorable periods we will risk a little more.

Trading for profit

As it is known, the very first task of correct mani management is to protect the initial capital. Trading is not a sprint, but a marathon, and the most important thing here is not to get off the track.

I understand people who first try to increase their deposit and then trade more calmly. Not every trader is able to afford a deposit, trading on which would fully cover his living expenses. That is why many traders want to reach this level as soon as possible and try to take big risks at the very beginning. This seems to be the right decision, because this way you can really quickly start to fully earn only from the market, and a small deposit is not so miserable to lose. But, unfortunately, not everyone manages to endure this sprint with increased risks and such a decision, as a rule, leads to opening a new account. This method is especially dangerous when a trader opens an account for a new strategy, for which he has no or very little statistics.

Hence, the rule follows – in order not to open a new account every new month, when you get an advance payment on your card, you should trade with a minimum lot on new accounts for some time. It does not matter how many zeros your balance contains – it is always worth trading with the minimum lot for one or three months. Firstly, it will give you an idea of how good your system is and will not drive you into a big drawdown. Secondly, if the system is able to bring profit in principle, it will be clear after the expiration of this period, as it will create some growth, which you may still be useful in case your TS suddenly falls into a period of drawdown after increasing risks. This way you will lose the accumulated profit, not the initial deposit, which will be psychologically a little easier – you have already seen how the system works and know that it is just a drawdown and the system works.

The second task of mani management is to make profit. This is where the most interesting part starts. If you have properly protected your initial capital, you have a very good chance of staying in the game long enough to finally extract some income from your trading. I’m assuming you’ve read everything above and understand how to properly increase your risk. If the increase in risk is done correctly, chances are that the amount of income that will be generated during a favorable trading period could surprise you. However, you must protect this income as there is always the possibility of a drawdown that could corner you.

Therefore, if the protection of the received profit is more important for you than continuing to build up your account as fast as possible, then the most important step at the moment of drawdown will be to reduce your risk per trade at a faster pace than the rate at which the risk was growing in a favorable period. And we have already analyzed this technique in detail above, when we used the moving average on the balance.

Conclusion

Today we have analyzed in detail such a popular method of money management as fixed-fractional. Hopefully, knowing the advantages and bottlenecks of using fixed-fractionation will help you avoid many mistakes when managing your capital. Instruments such as the cut rate and the cut rate allow you to level out the disadvantages of the fixed-fraction method and, as you have seen, reliably protect your initial capital and the profits made in the process of trading.

Nevertheless, it is worth remembering that there is no ideal method of money management and not the trading system is selected for the “ideal”, in your opinion, method of money management, but on the contrary – for a particular trading system is selected such a method, which will hide all the shortcomings of the strategy as effectively as possible and highlight its advantages in the best way. A money management system is first of all a system and it is quite normal that a money management system will be no simpler than the trading strategy itself.

Good luck and see you soon!