Options: Basic Trading Strategies

Every year, options attract more and more attention from crypto traders. Crypto options make it possible to profit not only from a rise or fall in the price of an asset, but also from changes in volatility or the time value of contracts.

Options trading combines high profit potential with a complex risk structure. Therefore, even experienced investors start with basic strategies that make it possible to understand market mechanics and learn to manage risks. In turn, many of the complex strategies are based on combinations of standard options positions: buying and selling Call and Put contracts.

You can read about options and the specific terminology in the article "What Are Options and Why Are They Needed." In this article, we will look at the key basic strategies for trading crypto options: directional trading and trading synthetic futures.

Directional Options Trading: Basic Call and Put Positions

The simplest form of working with crypto options is opening a single position. Despite the apparent simplicity, even such trades can be considered separate strategies.

There are four basic variants:

| Column 1 | Column 2 | Column 3 | Column 4 |

|---|---|---|---|

| Strategy | Description | Profit Potential | Risk |

| Long Call | Buying a Call Option | Unlimited | Limited by premium |

| Long Put | Buying a Put Option | Significant | Limited by premium |

| Short Call | Selling a Call Option | Limited by premium | Theoretically unlimited |

| Short Put | Selling a put option | Limited by premium | Significant |

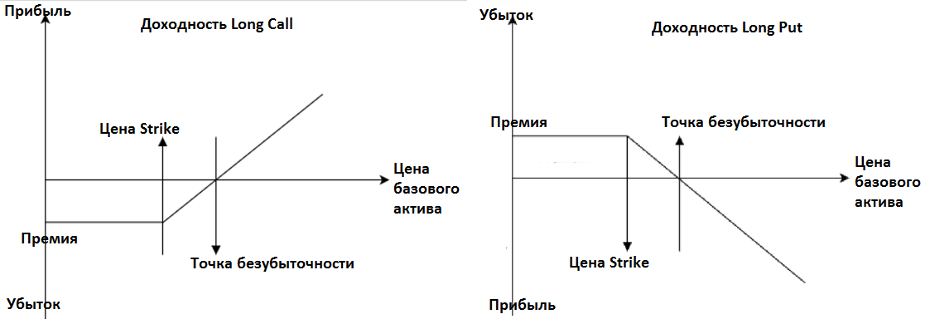

The payoff diagrams for buying Call and Put options look as follows.

Long Call

Buying a crypto Call option is used when a trader expects a significant rise in the price of the underlying asset. If the forecast is correct, the profit can be practically unlimited, since the price of the asset can rise without a formal upper limit. The risk in this case is limited to the amount of the premium, the cost of the option.

Example. The trader expects BTC to rise. Trade parameters: the option price and strike are $80 000, the premium is $10 000, and expiration is 1 month. The maximum loss is the premium, while the profit is unlimited.

| Column 1 | Column 2 |

|---|---|

| Bitcoin price, $ | Result,$ |

| 80 000 | −10 000 |

| 70 000 | −10 000 |

| 90 000 | 0 |

| 100 000 | +10 000 |

Long Put

Buying a crypto Put option is used when a price decline is expected. The theoretical profit is limited, since the price of an asset cannot fall below zero. However, the strategy makes it possible to profit effectively from strong downward market moves.

Example. The trader expects BTC to decline. Trade parameters: the option price and strike are $100 000, the premium is $8 000, and expiration is 1 month. The maximum loss is the premium, while profit grows as the price falls.

| Column 1 | Column 2 |

|---|---|

| Bitcoin price, $ | Result,$ |

| 120 000 | −8 000 |

| 100 000 | −8 000 |

| 90 000 | +2 000 |

| 60 000 | +32 000 |

Selling Options

Selling options is a much riskier strategy. The trader receives the premium, but takes on potential obligations to fulfill the contract. At the same time, the seller of a Call faces unlimited losses if the price rises sharply, and the seller of a Put is obliged to buy the asset if the price falls hard.

Example Short Call. The trader sells a Call on BTC. Trade parameters: the option price and strike are $100 000, the premium is $8 000, and expiration is 1 month. The trader immediately receives a profit of $8 000, but if the price rises above $108 000, a direct loss begins to form.

Example Short Put. The trader sells a Put on BTC. Trade parameters: the option price and strike are $100 000, the premium is $8 000, and expiration is 1 month. The trader immediately receives a profit of $8 000, but if the price falls below $92 000, a direct loss begins to form.

Such positions require substantial collateral, and, in essence, earning from the premium is a strategy for institutions and market makers that hedge their risks in other ways.

We do not recommend selling crypto options within a directional strategy.

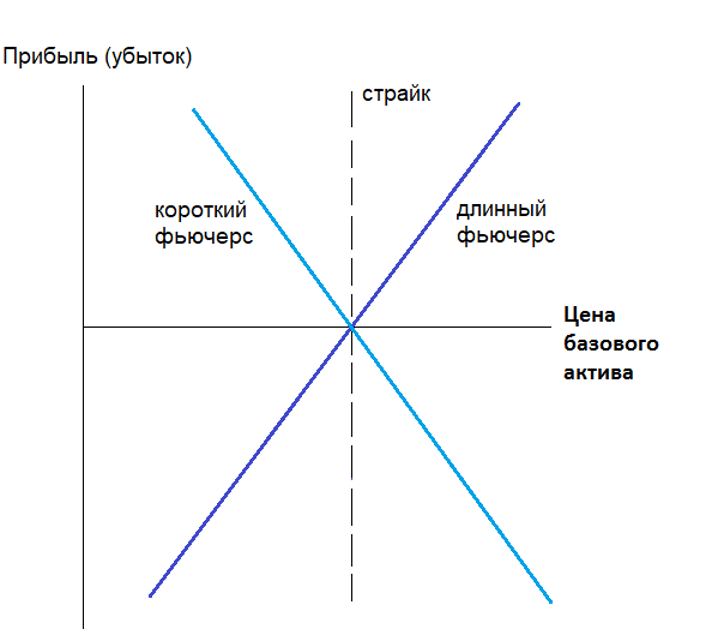

Synthetic Positions: Creating an "Artificial" Future Using Crypto Options

A more complex construction is a synthetic future, which is created by simultaneously opening two positions at the same strike. The main advantage is margin that is 20-40% lower than a future or even no margin requirement at all.

Because the contracts are entered into at the same strike, the premiums of the buyer and seller offset each other, so the breakeven point equals the strike, just as in ordinary trading.

The payoff diagrams for synthetic futures look as follows.

Bullish (long) synthetic future:

- buying a Call

- selling a Put

Example. The current price of ETH and the strike are $2000, and the option expires in 1 month. The premium for buying the CALL is $120, and for selling the PUT it is $110. Thus, the cost is only $10.

At expiration, the following will occur.

| Column 1 | Column 2 |

|---|---|

| ETH price | Result |

| $2500 | +$490 |

| $2200 | +$190 |

| $2000 | −$10 |

| $1800 | −$210 |

Thus, the position behaves like buying an ETH future.

Bearish (short) synthetic future:

- buying a Put

- selling a Call

Example. The current price of ETH and the strike are $2000, and the option expires in 1 month. The premium for selling the CALL is $120, and for buying the PUT it is $110. Thus, the initial income is $10.

At expiration, the following will occur.

| ETH price | Result |

|---|---|

| $2500 | −$490 |

| $2200 | −$190 |

| $2000 | +$10 |

| $1800 | +$210 |

Where to Open a Synthetic Future

Note that, for maximum correspondence to a regular future, it is customary to create a future by buying and selling ATM options (At The Money, at the money). In other words, the strike matches the current price of the cryptocurrency.

ATM options usually have the narrowest spread and trade more often, which reduces entry cost. In addition, an ATM synthetic has a delta of ≈ ±1, almost like a future. Therefore, the position reacts to price almost identically.

If the strike differs greatly from the asset price, the options will be deeply ITM or OTM. In this case, the premiums become imbalanced, and the synthetic replicates the future less accurately.

Example. ETH is worth $2000. Synthetic long: Sell Put 2200, Buy Call 2200. In this case, the position will start earning only after 2200, and the behavior will not be exactly like that of a future.

The main advantage of creating an at-the-money synthetic is the ability to obtain an analogue of a futures position without the need for full margin collateral.

Important: for crypto options (Deribit, Bybit, etc.), put-call parity holds closely, but deviations and arbitrage constraints are possible.

Advantages of Synthetic Futures

Funding Rate in Perpetual Futures

On crypto exchanges, most futures are perpetual contracts (perpetual futures). When the market is strongly bullish, traders actively buy futures, and positive funding arises.

Example. The price of ETH is $2000, while the price of perps is $2080. Longs pay funding to shorts every 8 hours. In such a situation, a regular future becomes more expensive, while a synthetic future through options remains closer to fair value.

Demand for Options and Implied Volatility Skew

In the crypto market, there is often strong demand for downside protection, so traders buy Put options for hedging. This leads to the price of the Put rising, while the price of the Call becomes relatively cheaper.

The formula for a synthetic synthetic future: Synthetic future = K (strike) + (Call − Put).

If the Put becomes expensive, then the Call - Put difference decreases, which makes the synthetic future relatively cheaper. This effect is called volatility skew.

Instead of a Conclusion

The options trading strategies described above, despite their simplicity, can, but do not have to, bring substantial profit even to beginners in options trading.

Which crypto exchanges should you look for options on? First of all, Deribit, then Binance, Bybit, etc.