July Inflation Stress Test: PPI, CPI and the Fed’s September Window

Tlapchik

Intro

The market is entering the July inflation stretch in a familiar mood: calm on the surface, alert underneath. Traders are watching PPI and CPI not as isolated statistics, but as the next checkpoint for the whole autumn rate-cut story. Consensus is centered around PPI near 2.5% year over year and CPI near 2.4% year over year, which is a narrow runway for expectations that have already become fairly demanding. The market looks a bit like a guest standing at the Fed’s door with a hat in hand, polite smile ready, but still unsure whether the cheap-money party invitation is real.

📊 Inflation Data: The Bar Is Already High

The key issue is not simply whether PPI comes in around 2.5% year over year and CPI around 2.4% year over year. The real question is whether those numbers are soft enough to convince traders that inflation is moving in a direction the Fed can tolerate before September. A clean inflation print would support the rate-cut narrative; a hotter print would force the market to reprice that confidence quickly. That is why this data block matters more than a normal macro release. Producer prices can hint at pipeline pressure, while consumer prices tell the Fed whether that pressure is still reaching households. If both reports behave, risk assets get a reason to breathe; if either report surprises on the upside, the market may have to put its optimism back on a shorter leash.

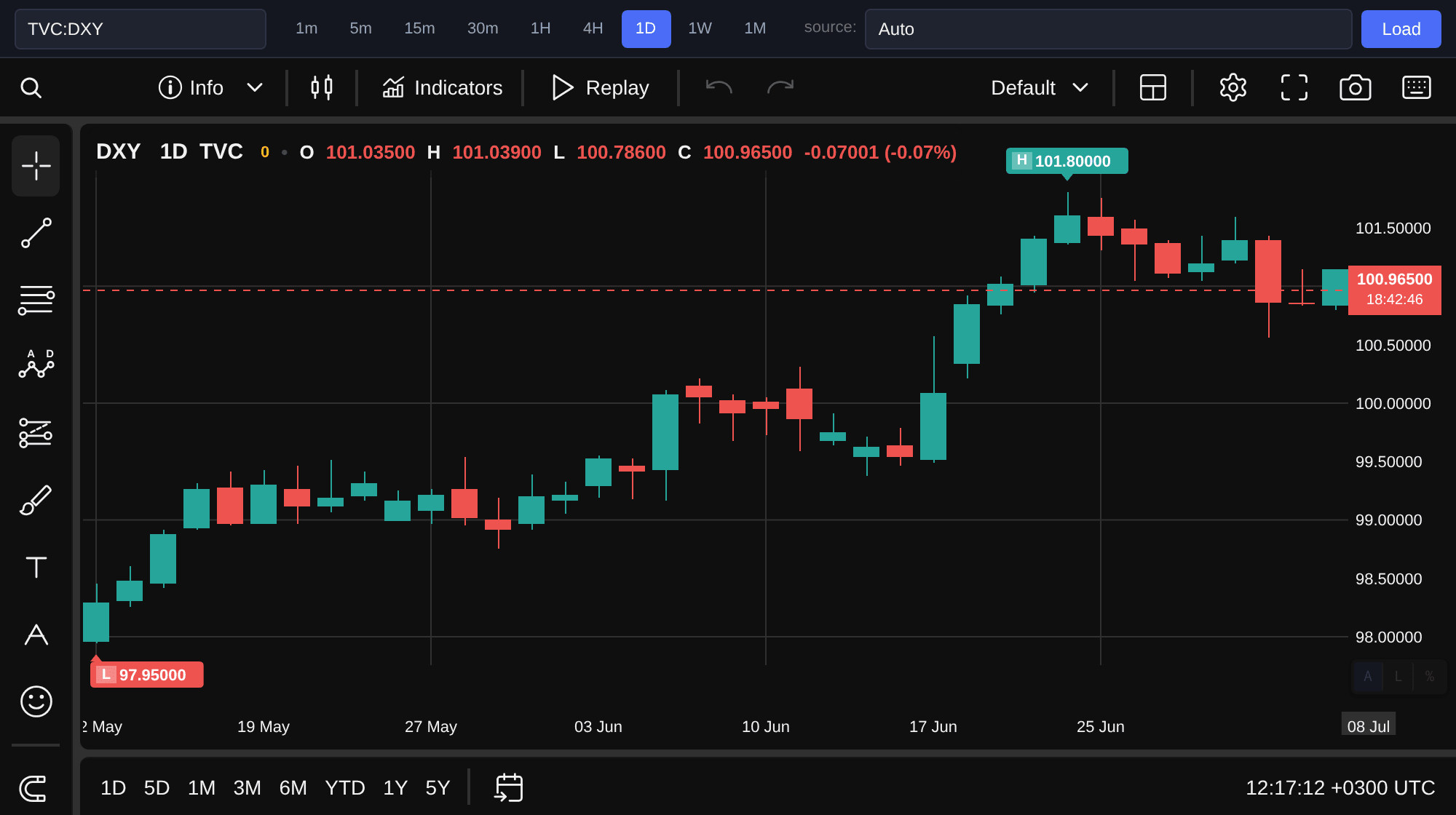

💵 Dollar: Quiet Weakness Before the Numbers

The dollar is not showing panic, but it is leaning softer before the inflation releases. The DXY dollar index is at 101.0 USD, down -0.08% on the day, which suggests traders are not aggressively buying protection through the greenback ahead of the data. A softer dollar fits the idea that the market still sees room for the Fed to move toward a September rate cut. Still, this is a fragile signal rather than a verdict. If CPI or PPI comes in hotter than expected, the dollar can recover quickly because higher-for-longer rate expectations usually make U.S. yields and the dollar more attractive. If the data cools, the current weakness in DXY could extend as traders lean further into the easing scenario.

📉 S&P 500: Risk Appetite Takes a Breath

Equities are also showing caution rather than stress. The S&P 500 is at 7,483 USD, down -0.28% on the day, so the index is giving back some ground without sending a dramatic warning signal. This looks more like pre-data risk management than a full rejection of the bullish scenario. For stocks, the cleanest positive setup would be inflation that is soft enough to help rate-cut odds, but not so weak that it raises questions about demand. That balance matters because equity investors want lower discount rates, but they do not want a growth scare attached to them. A mild inflation print could keep the broad market supported, while a hot print would put pressure on rate-sensitive sectors first and then test the wider index.

🏦 Fed Expectations: September Remains the Market’s Main Question

The Fed does not need one perfect number; it needs enough evidence that inflation is moving sustainably toward target. That is why the market is treating the July PPI and CPI block as a stress test for September expectations. The September cut scenario survives best if both inflation reports confirm moderation without reopening doubts about sticky price pressure. The tricky part is that traders have already priced in a fairly optimistic path. When expectations are high, even an in-line report can produce a mixed reaction if positioning is crowded. Today’s setup is therefore less about guessing one headline number and more about watching how rates, the dollar and equities respond together after the data lands.Conclusion

The day’s main story is not the small move in any single index, but whether inflation gives the market permission to keep believing in a softer Fed by September. DXY at 101.0 USD and -0.08% shows cautious dollar softness, while the S&P 500 at 7,483 USD and -0.28% shows equities trimming optimism without breaking the broader risk mood. If PPI near 2.5% year over year and CPI near 2.4% year over year are confirmed or undershot, the rate-cut case gains support. If the data runs hot, risk appetite can cool quickly and the Fed’s September window will look less comfortable. Practical Forex takeaway: test the rule on a demo account, write it into the trading plan, and apply it consistently before every trade. Practical Forex takeaway: test the rule on a demo account, write it into the trading plan, and apply it consistently before every trade. Practical Forex takeaway: test the rule on a demo account, write it into the trading plan, and apply it consistently before every trade. Practical Forex takeaway: test the rule on a demo account, write it into the trading plan, and apply it consistently before every trade.#US inflation data#July PPI#July CPI#Fed rate cut#September rate cut