How to Increase the Profitability of Your Trading Strategy?

Hello, fellow forex traders!

The average trading book is rather useless, focusing mainly on choosing the point and time of entry, and as a result its readers lose money by applying all of this. Of course, there are books that, along with the usual nonsense, get to the far more important topic of mathematical expectation. However, most of these books again present this aspect incorrectly. Either they understate its importance, which makes them similar to the books already mentioned. But more often they even teach a completely wrong way of looking at the expected profit of a system, causing you to take yet another step in the wrong direction, giving their readers confidence and at the same time forcing them to lose money because of financial shortsightedness. In this article, we will try to fix this problem once and for all.

One saying goes as follows: "Losers focus on their profitable positions, while winners focus on winning." The same position can be viewed differently: if we change the point and time of entry, they matter, but if we use a consistent approach with adding to profitable positions, then the point and time of entry are almost irrelevant in the long run.

The Concept of Expectation in Trading

Although every trader should be familiar with the concept of mathematical expectation, we will briefly discuss this aspect once again.

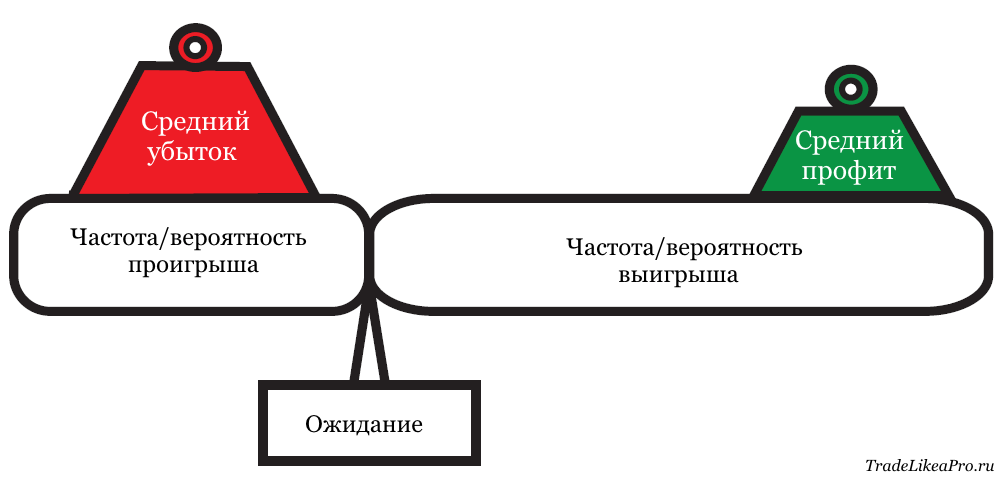

Look at the figure below. After all, total net profit (or loss) comes both from the frequency of profitable and losing positions (no matter how many there are) and from their average size. The goal of any market analysis, of any strategy, is to try to have more profitable positions (and, consequently, fewer losing ones). And although entry-point analysis may have its advantages, in the end, we cannot predict the future.

The average size of profitable and losing positions, on the other hand, gives us much more information and, in fact, a very large degree of control. For if we risk, say, three percent on our position, then our average loss will not exceed minus three percent. And the only thing we have to do for this is to close positions when the risk reaches three percent or less. No forecasts or analysis are needed at all. Likewise, we can also increase the average size of our profitable positions simply by holding them (i.e. not closing them) and adding to them (i.e. opening more positions in this direction), since they will bring us large profits. Thus, in the end, all this implies minimizing losses and maximizing profits. Returning to the figure, this means that we should focus on the mass of the weights.

Being profitable in trading in the long run comes down to minimizing losses and allowing profits to grow. The point is not whether you act correctly or not, the point is how you manage your profits and losses.

Problems with Expectation in Trading

Mathematical expectation is not difficult to understand. And to help explain it, very simple analogies are often used, for example, gambling: dice, roulette, or even the lottery. Thanks to expectation, it is easy to prove that all such games, in the end, are losing ones if you play for a fairly long time (if this topic interests you, google for example "roulette mathematical expectation").

So there is no point in gambling except for entertainment.

Someone who has just won several million in the lottery may be hard to convince of this. Just ask him to spend all his winnings on lottery tickets next week, and he will understand everything.

And now we come to the core of the problem. The concept, or, one could say, the myth of the "expectation of your system." A more popular term among traders is "edge." The legend says that you must have a positive expectation from your trading system. But this is a useless pursuit, because, unlike gambling, a system may not have, and probably does not have, a constant percentage of profitable positions. After all, markets do not move randomly. Thus, in financial markets, we know only our historical frequency of profitable and losing positions, unlike a dice game, where we also know the forthcoming expectation.

The myth of needing to have positive expectations from your system before entrusting it with our money has serious consequences. It fuels the belief that you need an edge (in terms of mathematical expectation) to be profitable in the long run. In addition, it fuels the useless need for backtesting. Any system that has negative expectations and is, naturally, supported by backtesting is discarded. Good systems are criticized because they may, for some time, be out of sync with the markets, i.e. fail to generate profit for a while. And it goes as far as fitting the equity curve to historical data, i.e. over-optimization.

What do traders do in search of a system with positive expectations? The very same thing: they do not take into account the probability distribution in the area of measurement. And if Nassim Nicholas Taleb's "Black Swan" taught us anything, it is that we simply cannot do that.

We cannot apply measurements beyond the interval in which those measurements were made. And we certainly must understand that we should look at expectation as a whole. It is not probabilities that kill us, but results themselves. And again, even probabilities (and perhaps similar distributions) are not stable in financial markets. Markets have a chaotic, fractal nature, with exponentially changing behavior (and even that not always).

What Should Be Done to Improve Mathematical Expectation?

The good news is that when a trader starts thinking with his own head rather than hoping on expectations, he does not need to do anything with his "system." Trading expectations (as opposed to expectations from your system) are a simple use of the knowledge that we have much greater control over the size of our profit/losses (the average size of profitable and losing positions) than we have over probability (the frequency of profitable and losing positions). And because we do not focus on historical expectations, trading expectations can work for us. By keeping losses small and increasing our profits (and adding to profitable positions), we gain true advantages.

The following experiment was conducted: a simulator opened random positions, from which mathematical expectation and net profit were calculated.

In this model, several million sets of 30 long positions during a bear market were averaged. The average net loss was -12 percent, and only about one third of all positions were profitable. Now, by simply opening the same positions, cutting losses to minus three percent (using a stop-loss) and at the same time adding to profitable positions, we achieved an average net result for those same positions of 1.8 percent profit (on average in a falling market). So, by using expectation to our advantage, we actually changed the expectation values! Traders who believed that initially negative expectations were useless would never have been able to do this, because they abandoned this system from the very beginning.

This does not mean that losses can be turned precisely into profits, but in the long run expectation works thanks to closing losing positions and adding to profitable ones. But when looking at a possible trade history on a chart in the past, traders often deceive themselves. Thus, no trading system is either profitable or unprofitable, they only look that way in relation to the applied position sizing method and money management.

In Conclusion

In conclusion, the following should be said: looking at how a forex strategy behaved in history is one thing, but expecting it to behave the same way in the future is another.

Traders should focus less on historical testing and more on the current situation: cutting losses and, to an even greater extent, maximizing their profits and adding to profitable positions. Follow this rule for a sufficiently long time, and you will feel the true power of mathematical expectation in Forex trading.

Another important point in choosing a strategy is its logical justification, but about that some other time, keep an eye on the publications on the site ;)

Best regards, Pavel Vlasov

TradeLikeaPro.ru