Fundamental Analysis for 2016

Hello, fellow forex traders! Today I would like to discuss what we should expect from the major currencies in 2016. And while we will take a technical look at the pairs in the New Year webinar, fundamental analysis deserves separate attention.

How do you use fundamental analysis? Very simply: look at the conclusions and take them into account when opening more or less medium-term positions. On our forum, we have individual traders who, after studying the fundamentals, open positions and hold them for months. The result? They catch long trends. Be that as it may, you should not forget about fundamentals, so let us look at the current situation at the end of the year and also forecast the ruble exchange rate (USDRUB).

Fundamental Analytics for 2016

According to statistics, in 52 of the last 53 years the global economy showed continuous growth, and only the period of the Great Recession showed a slight decline in global GDP. According to estimates by the International Monetary Fund, the period from December 2007 to June 2009 had the greatest impact on the global economy since World War II.

Today the economy is at the stage of restoring the growth rates of past years, with both advanced and developing countries contributing to this. Thus, European countries promise to feel a little better, while Asia faces a more difficult time.

The most difficult period is being experienced by resource-dependent countries, whose economic well-being strongly depends on the condition of the commodities market. The share of countries dependent on the extraction and export of minerals is constantly growing, and by 2011 they already accounted for 26% of the global economy, while in 20 years this figure may exceed 50%. On average, in terms of economic development rates, resource-dependent states lag far behind those that do not rely on resources.

In its September report, the IMF provided an overview of the world economy that offers an intermediate view of the global situation. The IMF forecasts an expansion of the global economy in 2016, with inflation at 3.6%, versus 3.1% at the moment.

In turn, North America is expected to roughly match last year’s growth figures, while neighboring Canada is preparing for a slowdown in growth, given the country’s focus on commodities. Growth in the Mexican economy also promises to remain stable, with low inflation and low unemployment.

The Future of the Eurozone

Next year, the European Union expects moderate GDP growth of 1.9 percent. Given the minimal population growth on the continent, this is a fairly decent figure, though not one that inspires great enthusiasm. Earlier this year, the industrial sector showed a significant decline, but by now it has already recovered most of its losses. In addition, the problems with Greece hardly affected the overall fundamental indicators, and the leading economies remained unharmed.

Despite the English press pushing the idea that the European Central Bank had no intention of lowering the interest rate in December, the decision was nevertheless made in favor of easing by 10 basis points (or 0.1%). As a result, the incorrect interpretation of the rumors triggered a large-scale rally of the European currency against the dollar.

What is even more surprising is that the movement continued in the same direction even after the actual rate data were released. As a result of the bank’s disappointing statements, the bears found themselves squeezed into an awkward position while awaiting the results of the upcoming press conference.

Apparently, the ECB sent buyers into a state of excitement with its statement about extending the quantitative easing plan by at least 6 months. The market reaction was as if the bank had actually raised rates: the euro is rising, the German DAX index is falling, and bond yields are increasing. In part, such a reaction may be due to reduced inflation expectations for 2016; however, in the future this can only bring more problems rather than prove to be a good and far-sighted decision.

Indeed, it seems more like the ECB does not fully understand exactly what measures are needed to stimulate the level of inflation and economic growth in the coming year. And given that the overall economic situation is currently closer to its peak than to its bottom, the way out of the crisis largely depends on the further steps taken by the central bank.

Most likely, already at the beginning of 2016 the EURUSD pair will finally come to parity.

The Crisis in the United Kingdom

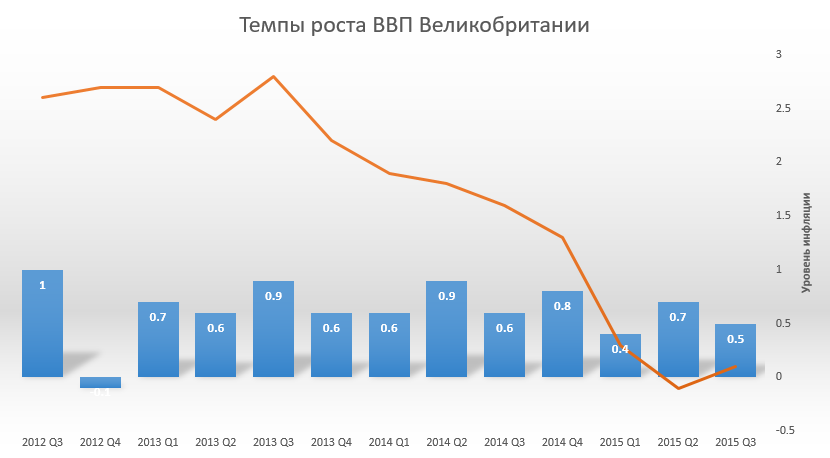

The recent weakening of the pound sterling against the US dollar (GBPUSD) is testing traders’ expectations regarding an early rate hike in 2016. Economic data support easing, with losses in both the industrial and construction sectors. On the other hand, the business activity index in the services sector exceeded expectations with a reading of 55.9. However, it is safe to say that the negative consumer price index data more than overshadow the figure that only slightly exceeded expectations.

The chart below shows inflation figures compared with GDP growth dynamics. Both indicators showed a decline in 2015 and, apparently, before making a decision on raising rates we will first have to see a reversal in the trend of both indicators. This is also confirmed by comments from the bank’s chief economist Andy Haldane, who states that the next interest rate decision will most likely favor easing rather than raising. In any case, no increase should be expected at least until the second half of 2016.

In the end, the decision to keep rates at the same level and the strong divergence between the policies of the Bank of England and the Fed will be the main factors influencing the weakening of the pound next year.

North America

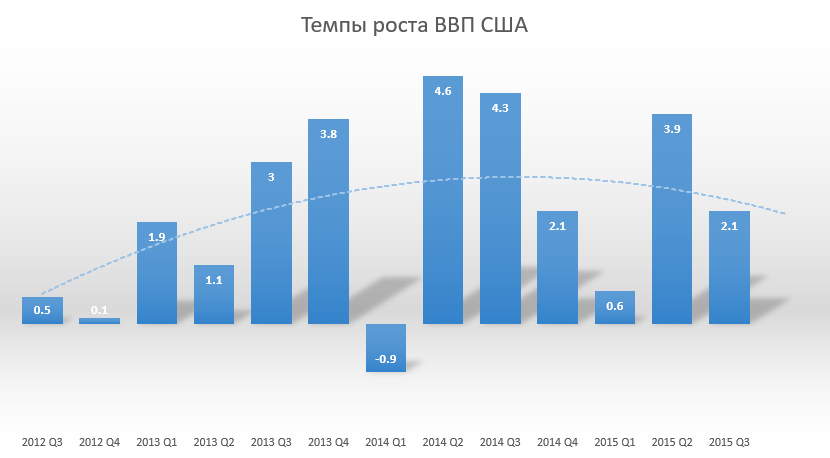

On Wednesday, December 16, the Federal Reserve System raised interest rates, something that had not happened for almost a decade. We can now say with confidence that the US economy has fully healed all the wounds inflicted on it by the financial crisis of 07-09. The Fed raised rates by a quarter of a percent, to 0.50%, thereby ending the debate over whether the US economy was strong enough to withstand higher borrowing costs.

Investment bank Credit Suisse forecasts US economic growth of 2.5% in 2016, along with rising employment and wage levels, which in turn could stimulate inflation. However, while the Swiss bank's forecast is quite optimistic, the dynamics of US GDP growth rates in recent years have been unstable and overall show a downward trend.

Of course, the scale of the domestic American economy will help shield the country from a global recession, since more than half of US companies' revenues are domestic. On the other hand, a third of US corporate revenues are generated abroad, which makes it impossible to fully insure companies against the effects of a global slowdown in growth. However, the national currency still has enough strength left to put substantial pressure on the exchange rates of countries with weaker economies, and the dollar reaching parity with the euro is no longer far off.

Asia

The Asian region remains a phenomenon of unpredictability for the global economy. In particular, it is difficult to say what exactly is happening in the middle of China's giant economy. According to official data, GDP growth in the last quarter was 6.9 percent, compared with 7 in the previous one. But who trusts official statistics? We know that the volume of US exports to China declined earlier this year, but recovered somewhat over the past few months. Consumers are helping the economy, and low capital expenditures are good news.

Japan, meanwhile, has fallen into recession, continuing a decade-long decline after the bursting of the economic bubble of the eighties and early nineties. Although unemployment remains very low, the shrinking population and labor force prevent any significant growth, while interest rates stay near zero or even below it. The demographic issue continues to have a negative impact, and it is becoming obvious that the Bank of Japan is not continuing its quantitative easing program simply because it no longer has such an opportunity. In the end, it is already by far the largest holder of Japan's government debt.

The revision of Japan's GDP data showed growth in the third quarter, but the continuing decline in China's trade balance leaves room for doubt for all Asian exporters, of which Japan is one of the largest. It is unlikely that in the current economic situation one can expect a positive outcome for USDJPY, whose rate, according to many experts, will reach 130 per dollar by the end of the first half of 2016.

India, in turn, is showing steady growth, but capital expenditures have declined this year. Consumer spending and low commodity prices are the strengths of the Indian economy and will stimulate its further expansion.

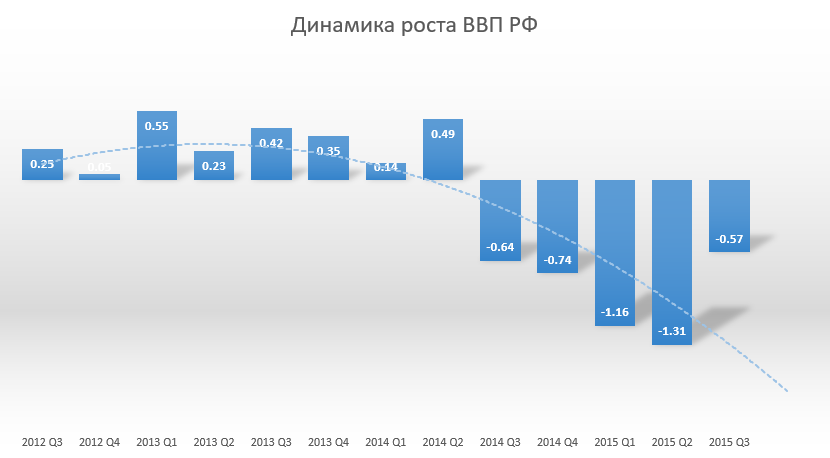

The Threat of Ruble Devaluation

As of today, the ruble exchange rate is more dependent than ever on external factors. First of all, the condition of the Russian economy is influenced by the state of the global commodities market, since oil still makes up a significant share of the country's exports. The slowdown of economic growth in China also indirectly affects the commodities market to some extent. Given the fact that China remains the largest consumer of raw materials on the global market, the slowing pace of growth in the Celestial Empire's economy can directly affect the price level of black gold.

The Russian Ministry of Finance allows for a short-term decline in oil prices to the level of $20 per barrel next year. In theory, such a situation could lead to a reduction in market supply and prices would begin to rise again. However, despite the fact that the Ministry of Finance had forecast a recovery in GDP growth by the end of the current year, the further decline in oil prices forced it to revise the forecast. Specialists from Morgan Stanley also point to this, expecting a recovery in indicators no earlier than 2017.

US policy also plays quite a large role, including changes in the Fed rate. First Deputy Chairman of the Central Bank Sergey Shvetsov allows for the possibility of a decline in the dollar exchange rate immediately after the decision to raise interest rates is made. As a result, taking temporary stabilization into account, foreign specialists promise that the fluctuation range of the national currency will be limited to around 65-75 rubles per dollar next year. However, an expansion of the sanctions program against Russia could well send the currency to 90-100 rubles per dollar.

Lagging Players

Resource-dependent countries are going through hard times. These are mainly countries in much of Latin America, Africa, and some parts of Asia. Commodity prices are on average 30 percent below their 2011 peak, which is leading to cuts in the mining and oil industries, as well as agriculture. On the other hand, the current price level is still above pre-2007 levels, but that does not justify the lack of growth in the manufacturing and construction sectors.

Brazil is in the worst situation. First, this is a decline in economic activity, and nothing other than a period of depression awaits the country in 2016. GDP fell by -4.5%, and the interest rate stands at 14.25%, while inflation is just beyond the ten percent level. The Brazilian real fell by more than 30% over the year, and this trend is expected to continue in 2016.

Most likely, global indicators will grow somewhat more slowly than the IMF forecast, primarily because of the situation in China and its neighbors. But on the other hand, 2016 is unlikely to differ greatly from what we have seen in recent years, and the main difference will be in the texture of future growth, with greater gains in Europe and smaller ones in the Asian region and in countries heavily dependent on resource extraction.

Sincerely, Alexey Vergunov TradeLikeaPro.ru