Arbitrage in Crypto Trading: Pros and Cons

Arbitrage in crypto trading is the extraction of profit from temporary or structural price discrepancies of the same asset (or related assets) across different venues or in different instruments.

Different types of arbitrage use different "inefficiencies": spreads between exchanges, the difference between futures and spot, price mismatches in an AMM pool, unsynchronized quotes within a single exchange, and so on. The modern market offers many methods: from mechanical fast strategies (latency / MEV / flash loans) to statistical and pair-based approaches with a longer horizon.

In this article, we will examine what arbitrage trading is and the specifics of its use on crypto exchanges.

What Arbitrage in Crypto Is in Simple Terms

Arbitrage on crypto exchanges is a way to make money from the price difference of the same asset in different markets or in different forms of trading. The essence of arbitrage is very simple: buy an asset where it costs less and almost simultaneously sell it where it costs more, locking in the price difference as profit.

Crypto arbitrage plays an important role for the market as a whole. Arbitrage traders effectively help align prices between venues, increasing market efficiency. Thanks to their actions, strong price imbalances usually do not exist for long.

It is important to understand that an arbitrage trader does not try to guess the direction of the market. The trader is interested only in the fact that at the same moment in time the price differs in different places. Such discrepancies arise because of different liquidity, the speed of order arrival, the specifics of particular exchanges, fees, regional factors, and the behavior of market participants.

In practice, cryptocurrency arbitrage can look different.

The same asset can trade at different prices on two crypto exchanges because one of them has more buyers while the other has more sellers. It also happens that the spot and futures prices diverge more than usual, or through a chain of trading pairs you can obtain an asset more cheaply than directly.

In all these cases, we are talking about one principle: using a temporary or structural market inefficiency.

Despite its apparent simplicity, crypto arbitrage trading is not a way to quickly earn easy money. Arbitrage opportunities exist only briefly, because other market participants notice them quickly and immediately bring the price back into line.

In addition, actual profit depends not only on the price difference, but also on fees, order execution speed, slippage, and technical constraints. If you do not take these factors into account, then a theoretically profitable arbitrage can turn out to be systematically unprofitable.

What You Need to Know to Start Crypto Arbitrage

Implementing an arbitrage idea goes far beyond a visual signal. Even if indicators show a significant spread, network and operational factors must be taken into account.

For inter-exchange crypto arbitrage, the cost (fees) and speed of deposits and withdrawals, the speed of transaction processing (in crypto, confirmations on the blockchain), as well as access to the required volume of liquidity in the exchange order book are important.

For intraday arbitrage within one infrastructure (for example, through different pairs on one exchange or through the spread between futures and spot), the most critical factors are execution speed and configured order routing (the process by which brokers direct investors' orders to various trading venues).

Also, when developing an arbitrage trading strategy, one should calculate not only the theoretical yield of the spread, but also realistically assess slippage and the cost of fees.

Finally, for an experienced trader, an arbitrage indicator with deeper statistical analysis will be useful.

A simple idea is to find a standardized value (z-score) or a normalized spread between two venues and test cointegration and the stability of the mean.

If the spread is stationary and regularly returns to the mean, this makes it possible to apply pair strategies (statistical arbitrage). If the spread often "sticks" at a level, it is important to understand whether this is related to geography, a lack of market makers, or restricted access to the instrument.

Any practical approach must necessarily be accompanied by a strict backtest that takes fees and operational risks into account.

Frequent Mistakes Traders Make When Searching for Arbitrage

The main mistake of a beginner arbitrage trader is to trust the picture without taking execution into account.

Often, a novice arbitrageur sees a large spread and thinks that "there it is, easy profit." But this is a typical trap. In practice, an attempt to execute a large trade on an exchange with low volume will quickly lead to slippage, and the difference will evaporate at best.

The second mistake is connected with underestimating transaction costs and local rules.

Some exchanges charge high withdrawal fees, have limits on withdrawal volumes, or charge additional fees on pairs. If you do not take these costs into account, beautiful arbitrage statistics turn into a loss.

The third mistake is related to the speed of deposit / withdrawal transactions and order execution.

On a crypto exchange, for example, the block confirmation time may change, and different forex brokers have a slight difference in order execution speed.

The fourth mistake is ignoring real liquidity.

An arbitrage indicator may show the "Last price" and volume for some period, but this does not mean that the required volume can be bought/sold at this price. You need to look at the depth of the order book and real volume data before opening a trade.

The fifth mistake is relying only on historical data without a robustness test.

The spread may have been stable in the past, but the market structure has changed: market makers changed their behavior, new derivatives appeared, liquidity flowed into alternative pools.

Therefore, before starting arbitrage trading, it is necessary to check the stationarity of the spread and assess the risk of a change in the market's operating regime.

The sixth mistake is technical and operational miscalculations.

Beginner arbitrageurs often forget about data delays, compare different timeframes or different sources without taking timing into account: the spread value on one exchange may arrive with a delay relative to another.

In arbitrage, milliseconds and seconds decide a great deal, so the absence of latency control leads to falling behind in the moment.

Finally, the seventh, psychological mistake is trying to turn arbitrage into a kind of "passive income button" without continuous monitoring and risk management.

Even stable spread opportunities require supervision, capital management, and an understanding of the scenarios in which a profitable spread can unexpectedly disappear.

Main Types of Arbitrage Strategies in Cryptocurrencies

Strategies for Professionals

Professional arbitrage strategies are always fully automated: algorithms find interesting spreads, calculate mandatory costs and potential income, and with a positive mathematical expectation, robots place instant execution orders. All of this requires a large amount of capital under management and a very high transaction speed.

Cross-exchange (spatial / cross-exchange) arbitrage

The essence of the cross-exchange arbitrage strategy is as follows: the trader simultaneously gives an order to buy an asset on one exchange and sell it on another, using the price difference.

The cross-exchange strategy is generally available to beginners as well, but in the modern market it is difficult to implement because it requires instant order synchronization, available liquidity, and constant replenishment of balances on several exchanges. In reality, most pure "risk-free" opportunities disappear in milliseconds; they are instantly "closed" by low-latency bots.

For professionals, this is a basic tool, but their risk management systems are configured to generate profit over the long run, taking forecast losses into account.

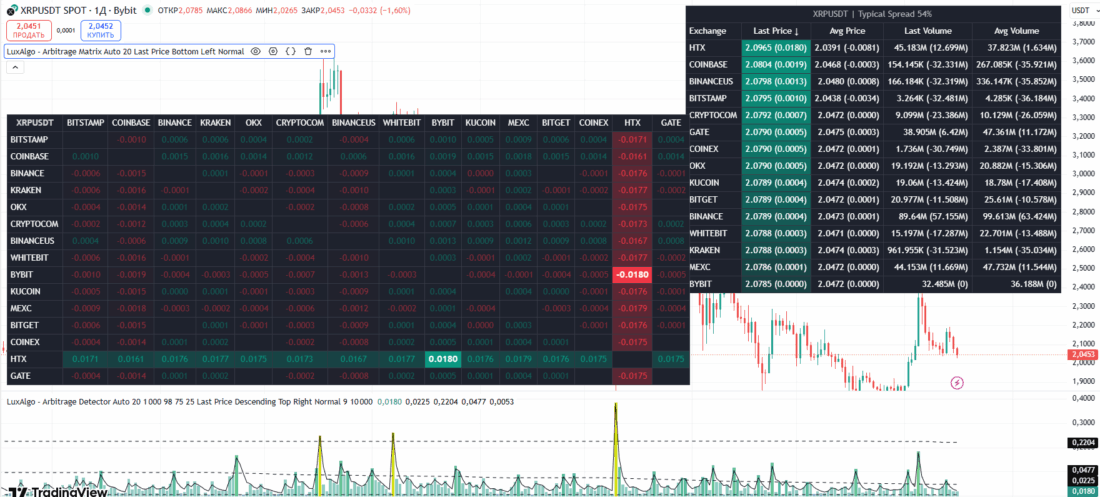

Example. On the Bybit exchange, the closing price on January 15, 2026 of the XRP cryptocurrency (the XRP/USDT pair) is 2,0785. The best closing price on the HTX exchange is 2,0965.

Buying XRP/USDT on Bybit and simultaneously selling the same volume on HTX yields a profit of 0,018 USDT on each coin. The transaction costs for transferring the coin from one exchange to another are not taken into account here, so the potential profit may turn into a loss.

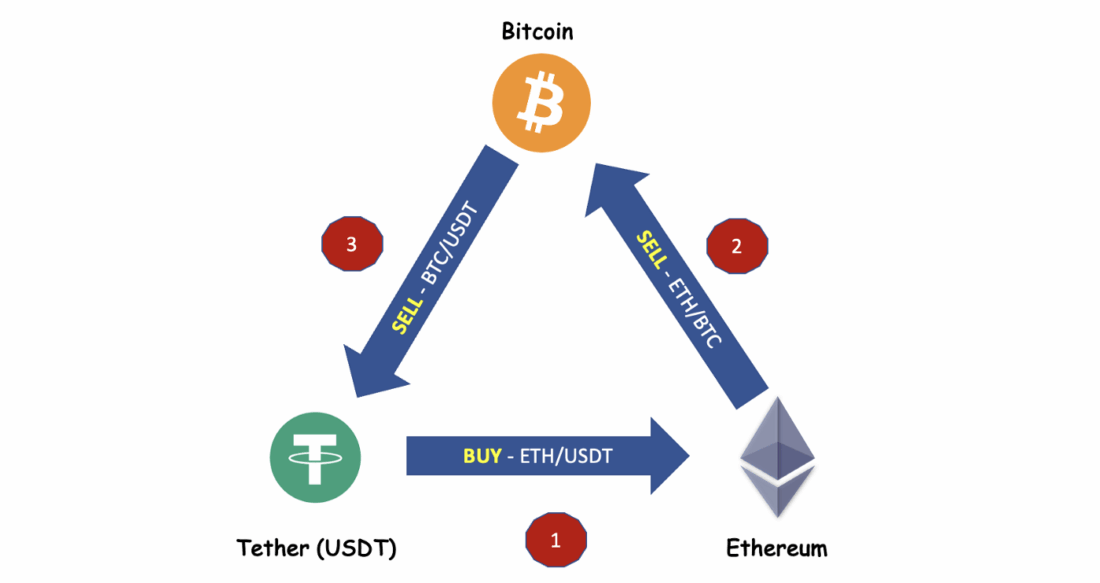

Triangular arbitrage (on-exchange and cross-exchange)

Triangular arbitrage implies using a price mismatch across three instruments/pairs (for example, A→B→C→A). On centralized exchanges, it requires lightning-fast execution.

There are two types of triangular arbitrage: on-exchange (within one exchange) and cross-exchange (between different venues).

If we are talking about an on-exchange triangle, then the bot “drives” liquidity through the chain while the earning opportunity exists. Cross-exchange arbitrage is potentially more profitable, but at the same time more risky because of differences in fees, transaction delays, etc.

For professionals, this is an opportunity, but competition is fierce, and automation is needed.

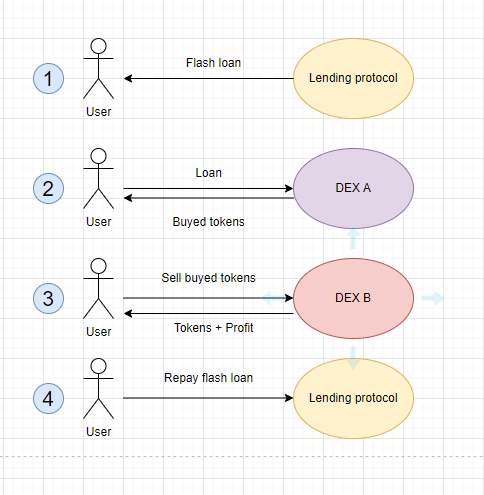

Flash loan (instant loan)

On DeFi platforms, arbitrage within the flash loan scheme was very popular not so long ago: a trader borrows an asset (for example, ETH) from a lending protocol, after which they buy on exchange A, for example, SOL, where it is cheaper, and sell it on the exchange where it is more expensive. After carrying out these operations, the trader returns the debt and interest to the lending protocol.

The main condition of a flash loan is that the debt must be repaid within a single transaction. At the same time, operational risk is minimal.

At the time of writing, this type of arbitrage exists, but it requires lightning-fast execution and is impossible without powerful trading robots.

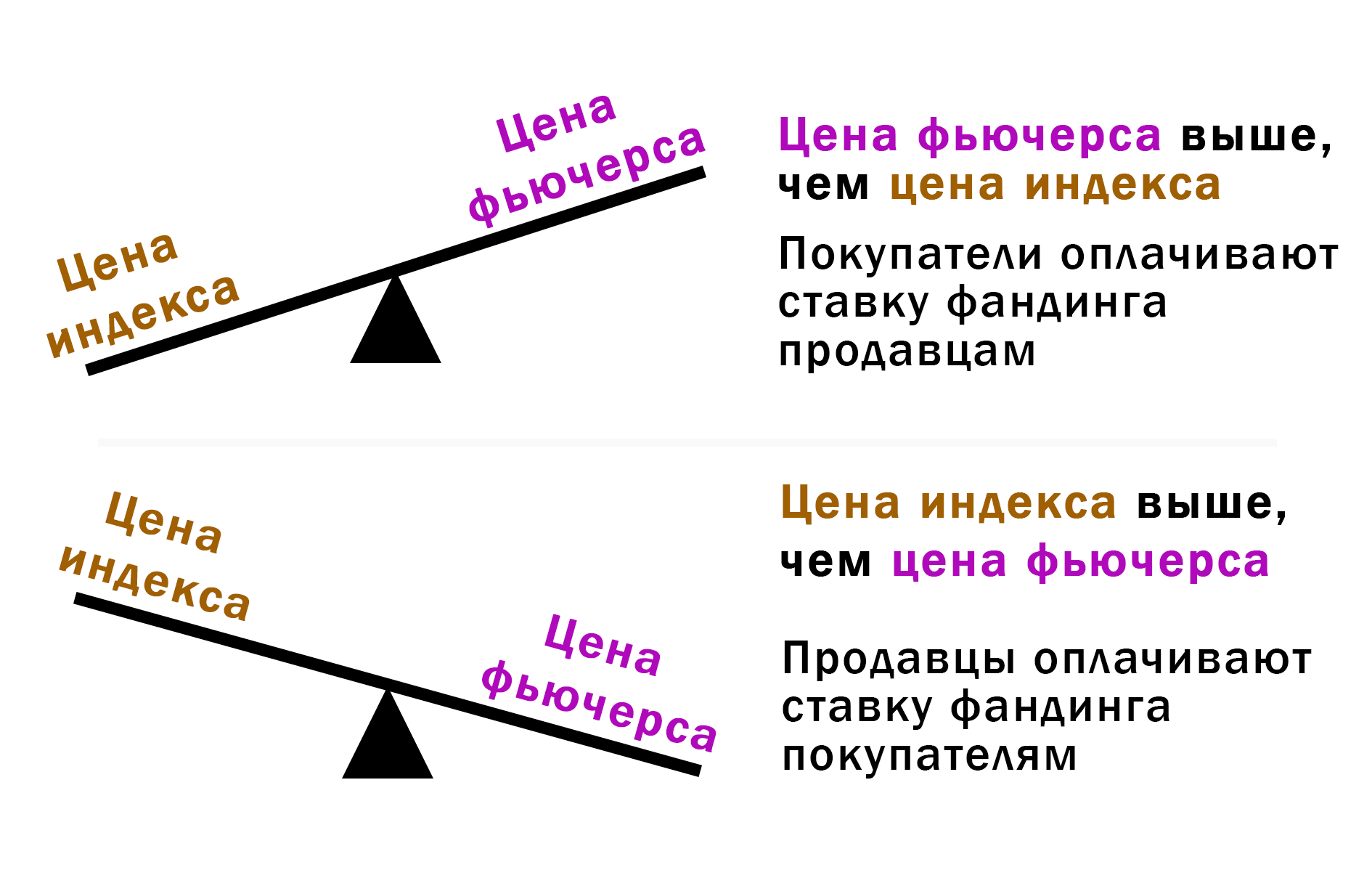

Funding-rate arbitrage on perpetual futures

This type of arbitrage is market-neutral: profit is generated as a result of payments on perpetual futures (perpetuals).

In brief, the funding-rate arbitrage scheme is as follows. Perpetual futures have no expiration date, which means they are “eternal.” Exchanges apply a funding rate to them, which bulls and bears exchange.

If the futures contract is more expensive than spot, then longs pay shorts. In this case, the arbitrageur opens a long on the spot market and a short on the perpetual future. The spot position balances the risk, while the short earns the positive funding rate.

If the futures contract trades below spot, then shorts pay longs. This is called a “negative funding rate.” In such a situation, the arbitrageur sells the spot asset and buys the perpetual future.

Thus, professionals hold opposite positions in the portfolio in order to collect the funding rate. This type of arbitrage requires accurate calculation of expected funding rates and strict leverage management.

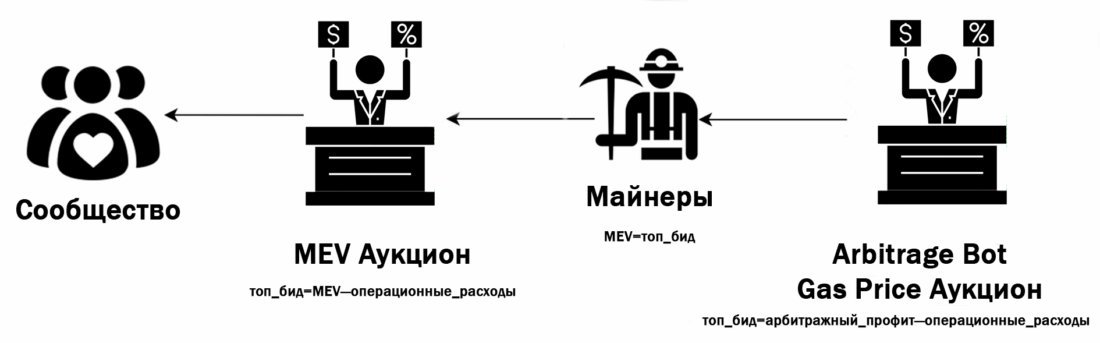

MEV / latency-front-running arbitrage

These types of arbitrage may be incomprehensible to traders without special education and immersion in the technical area of blockchain.

MEV (maximal extractable value) is a range of arbitrage crypto strategies that allow validators and/or miners to manipulate the order and selection of transactions in a block, which makes it possible to extract the maximum possible value.

Latency-front-running arbitrage is based on transaction delays in the blockchain and the process of transaction insertion in order to profit from a subsequent transaction. Such crypto arbitrage is based on exploiting the nonlinearity of transaction execution order and competition between transactions for inclusion in new blocks.

Statistical / market-neutral arbitrage (statistical arbitrage)

The statistical arbitrage strategy is quite simple and is based on price differences between highly correlated assets. Arbitrageurs assume that asset prices will return to their standard historical relationship.

Let us give an example from the world of forex trading. The correlation of the currency pairs EUR/USD and CHF/USD reached one in the past (complete connectedness). This allowed traders to find arbitrage opportunities and buy one pair if the movement on it was delayed for some time.

There are three types of statistical arbitrage: pairs trading, mean reversion, and volatility arbitrage.

Pairs trading is the simultaneous purchase of one asset and sale of a second correlated asset. When profit appears, it is locked in.

Mean reversion arbitrage implies identifying assets that have deviated strongly from their average correlations and buying/selling the asset in anticipation of a return.

Volatility arbitrage means searching for a discrepancy between the implied and expected realized volatility of options.

Professional teams use large samples, complex filters, and risk management, create high-frequency or medium-term pair strategies with backtests, optimization, and robustness monitoring.

For professionals, statistical arbitrage is one of the very reliable ways to extract profit.

Cash-and-carry arbitrage (spot-futures arbitrage)

This strategy is classical and is used in all types of markets.

Spot-futures arbitrage implies that a trader opens a long position in a certain asset, for example, buying a stock or a cryptocurrency coin, and simultaneously sells a futures contract on the same asset. A mandatory condition: the cost of the futures contract must be higher than the price of the underlying asset (for example, BTC costs 100000, and the futures contract costs 104000).

The essence of the strategy is that by the time the futures contract expires, prices often converge. Thus, if the spot price is maintained or even decreases, the trader sells the underlying asset, earning on the futures contract.

If the underlying asset rises before the futures contract expires, the trader either locks in a loss on the futures contract, or at the moment the futures contract is settled sells the underlying asset, effectively receiving a guaranteed profit in the form of the initial difference.

A simple strategy implies fixing the expectation that the prices of the underlying asset and the futures contract will match at expiration. Professionals build complex models that take into account funding, rollover, and the cost of storage/borrowing, which requires infrastructure, the ability to borrow/lend assets, and control over counterparty risk.

By the way, the pure cryptocurrency strategy of funding-rate arbitrage is an evolution of the classical cash-and-carry arbitrage.

Strategies for discretionary traders

Ordinary traders without special programming skills can use manual or semi-automatic arbitrage strategies. Such strategies are limited in their application, but with due diligence they quite allow one to earn from cryptocurrency arbitrage.

Spot-futures arbitrage (simple form)

A discretionary trader can periodically check price discrepancies between the spot market on one exchange and the perpetual contract on another. If the spread is consistently large and volumes allow it, a hedge position can be opened manually.

This is a less fast method compared with the professional version. It is necessary to calculate fees and execution time very carefully.

Cross-DEX arbitrage using ready-made scripts/services

It is easier for a discretionary trader to work with tools that show price mismatches between DEXs (Uniswap, Sushi, Curve, etc.) and then launch pre-prepared transactions (sometimes with a flash loan).

But if the trader has no programming skills, this can be used as a signal for manual checking and only in exceptional cases. An understanding of gas and the risks associated with unconfirmed blockchain transactions is required.

Triangular arbitrage within a single exchange (manual monitoring)

If triangular arbitrage is possible within a single centralized exchange (different pairs, shared order book), a discretionary trader can monitor and execute orders manually, especially during periods of low volatility, when spreads do not disappear instantly.

This requires fast assessment and order-book reading skills, acquired only through experience.

Pair arbitrage in a "slow" form

A trader with experience can apply pair methods not as HFT, but as medium-term positions: find correlated pairs and manually open trades with a longer horizon (several days to weeks) and conservative stops.

This approach reduces competition with HFT and requires careful backtesting and control over changing market regimes.

Funding-rate arbitrage in a simplified form

Discretionary traders can implement "manual" funding arbitrage: hold a long on spot and a short on a perpetual future during a period when the rate is positive and expectations of it remaining so are high enough. This is more accessible, but it requires daily monitoring of the funding rate and an understanding of leverage and liquidation risk.

The Bybit exchange has the tools necessary for this kind of arbitrage.

Conclusion

Arbitrage trading is a way to earn from differences in asset prices in different places at the same time. An example of an arbitrage system using the Arbitrage Detector and Arbitrage Matrix indicators can be studied at this link.

Cryptocurrency arbitrage trading is realistic for a trader with 1-3 years of experience. The work of a discretionary arbitrageur is quite complex and monotonous, and requires perseverance and strict risk accounting in every trade.

With the proper setup of an arbitrage system, the profit from each operation can be small, but quite guaranteed.

Respectfully,

Ivan Rusin