Compound Interest — Where Wealth Begins

A truth that beginner traders do not like to hear: no one will earn a million tomorrow. But with high probability, you can become a well-off person in 10-15 years if you start systematically applying profit capitalization today.

Compound interest is the mathematical formula where wealth begins. Understanding the very essence of compound interest allows you to stay in the game, reinvest, and grow rich. Albert Einstein, according to legend, called compound interest the “eighth wonder of the world.”

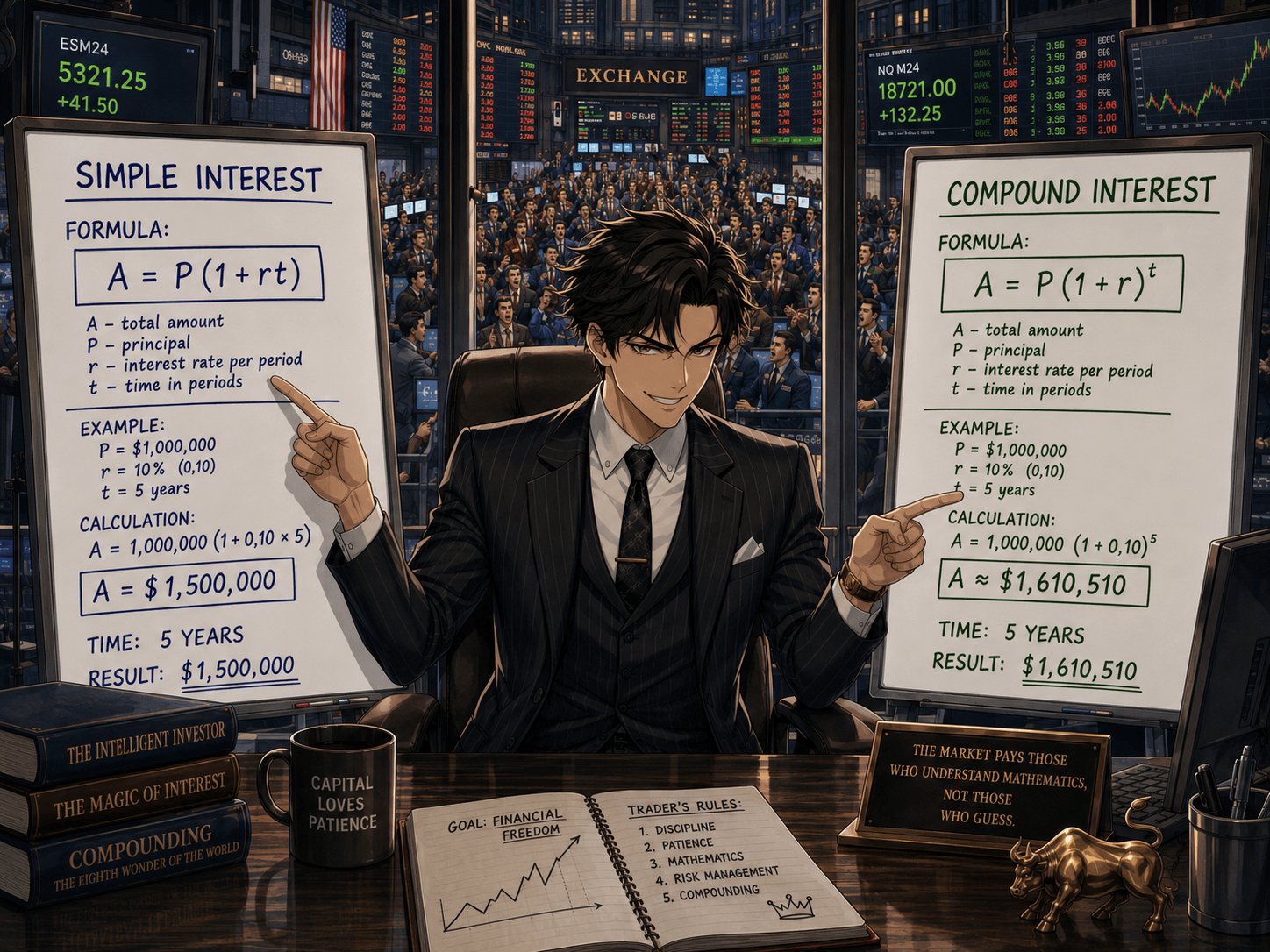

On Simple and Compound Interest

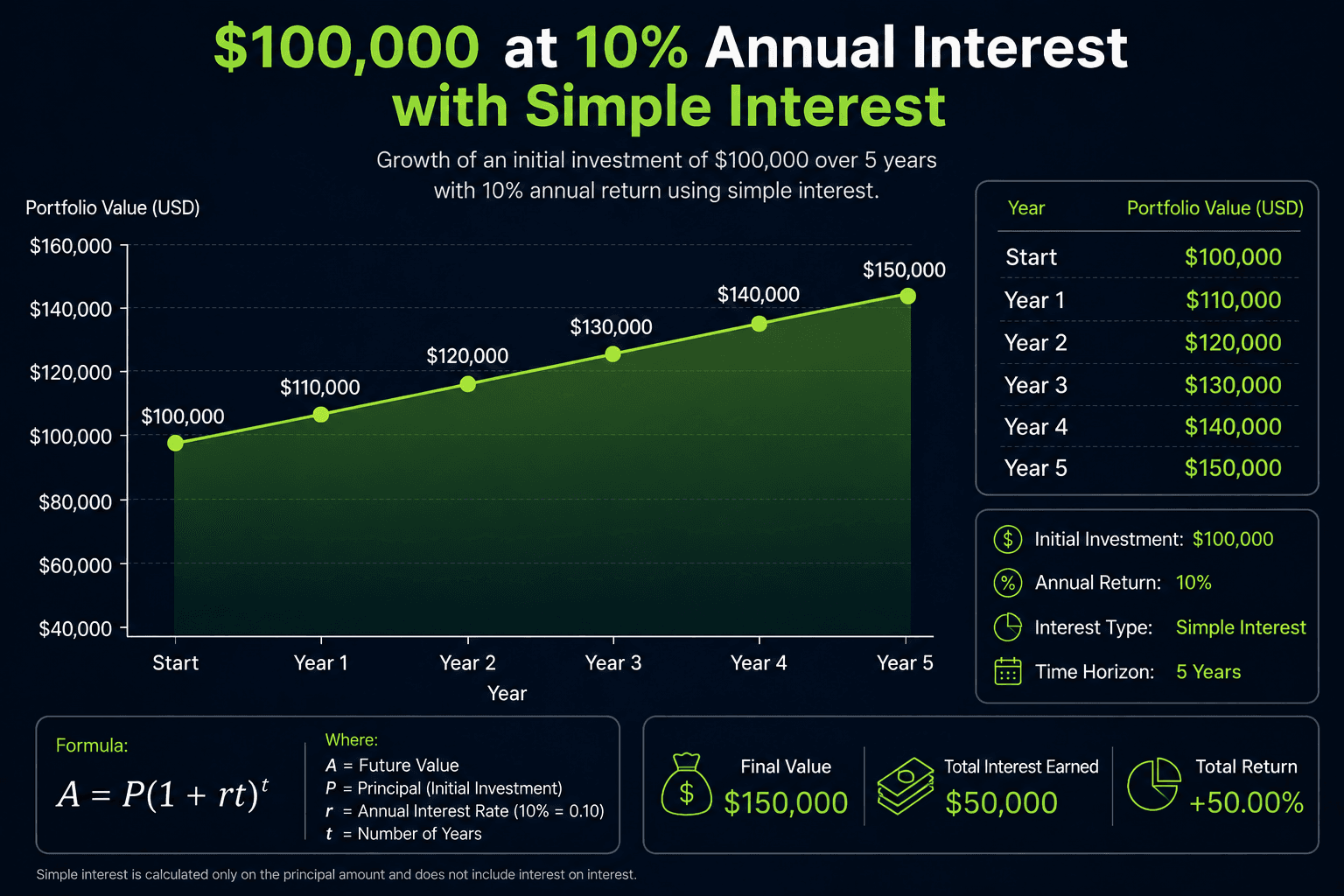

Before considering compound interest, it is necessary to understand the mechanism of simple interest. With simple interest, income is accrued exclusively on the initial investment amount. Interest payments are not added to the principal capital for further income accrual.

For example, an investor places 100,000 $ at 10% per year with simple interest payments. Each year he receives 10,000 rubles of income. After 5 years, his funds will amount to 150,000 $ (100,000 + 5 × 10,000), and after 20 years, 300,000 $. Capital growth is described by a straight line and does not accelerate over time.

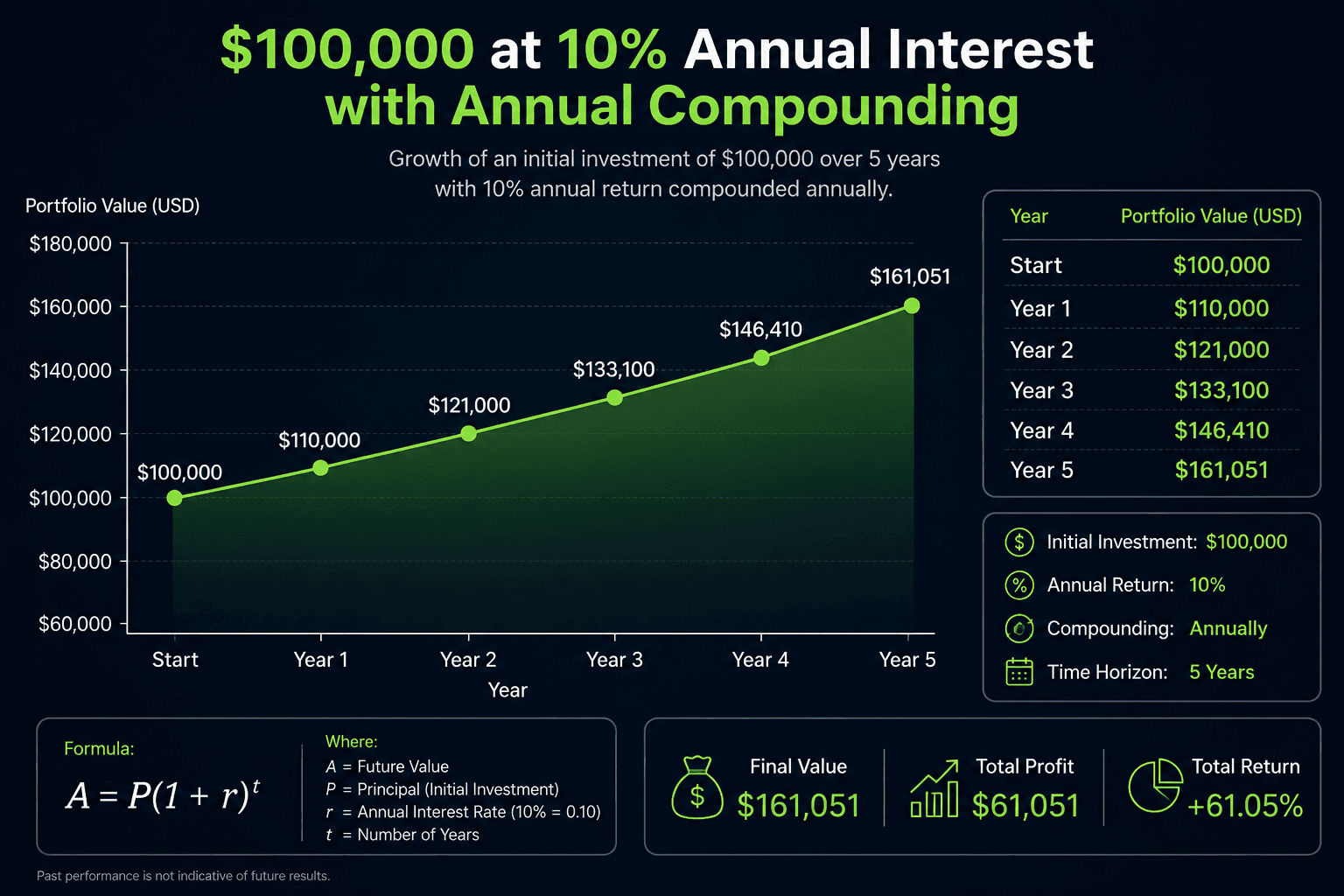

Compound interest is the accrual of interest not only on the initial amount, but also on the interest accumulated over previous periods. This mechanism is called interest capitalization. As a result, capital begins to grow exponentially, because with each period the base for accruing income increases.

- Let us consider the same amount of 100,000 $ at 10% per year, but with annual capitalization. After one year, the investor has 110,000 rubles. In the second year, 10% is already accrued on 110,000, which gives 11,000 $ of income and a total of 121,000 $. In the third year, the increase will be 12,100 $, and the amount will grow to 133,100 $.

Over 20 years, the difference in income will grow by more than two times: in the first case, net income will be 300,000 rubles, in the second, 672,750 thousand $.

Quantitatively, the future value of capital with annual capitalization is determined by the formula:

Where:

S — future amount (final capital);

P — initial capital;

r — annual interest rate in decimal form (for example, 10% = 0.10);

t — term in years.

The expression (1 + r)^t shows how many times one monetary unit will grow over t years at rate r. It is precisely the power dependence that creates the “snowball effect”: each next period adds an ever larger absolute increase.

The expression (1 + r)^t is the growth coefficient. At r = 10% and t = 20, it is approximately 6.73. That is, your ruble turns into 6.73 rubles. With simple interest, the same ruble over 20 years would give only 3 $ (1 original + 2 $ of income). The effect strengthens with each year, because not only your initial money is put to work, but also all accumulated income.

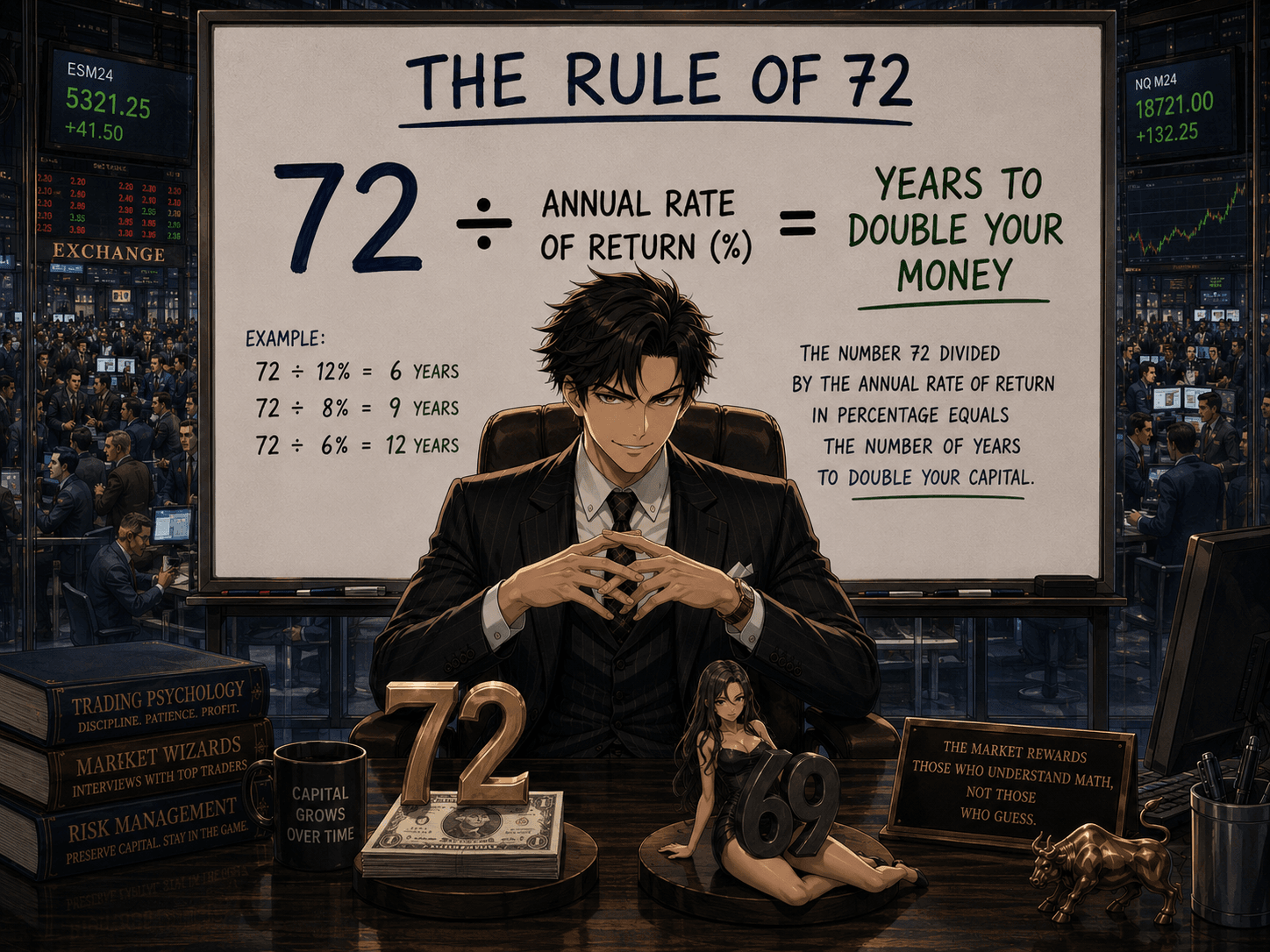

Rule of 72: A Quick Calculator in a Trader’s Head

The main ally of compound interest is a long investment horizon. The earlier the capitalization process begins, the larger the final result turns out to be, even with modest initial contributions.

A professional trader must instantly assess the potential return or the time needed to reach a goal. For this, there is the “rule of 72”:

Examples:

Return of 6% per year → 72 / 6 = 12 years.

12% → 6 years.

24% → 3 years.

This rule also works in reverse: if you want to double capital in 5 years, you need an average annual return of about 72 / 5 ≈ 14.4%.

For a trader, this gives a sobering framework. Expecting 50-100% per month means expecting the account to double almost every month. This is possible over a short stretch, but it is never sustainable. On the other hand, stable 15-20% per year over a distance of 10-15 years makes you rich. This is exactly how the best hedge funds and legendary managers work.

It Is Strange Why Traders Underestimate Compound Interest

Trading by its nature is a game of short moves. We look at charts of minutes, hours, at most days. In this world, the effect of compound interest is almost invisible: a weekly profit of 2% seems tiny against the background of volatility. But let us translate these figures into the language of long horizons.

A trader who earns on average only 2% per week and reinvests all profit will receive after one year (52 weeks):

1.02^52 ≈ 2.80, that is, growth of 2.8 times or +180% per year.

Let us compare two traders.

Trader A (aggressive) makes 20% profit every month, but with a 20% probability in any month he can lose the entire account. Over a year, the probability of preserving capital is: 0.8^12 ≈ 7%. Almost guaranteed ruin.

Trader B (conservative) earns only 3% per month with high stability. After 5 years (60 months), his ruble turns into 1.03^60 ≈ 5.89. That is, $10 000 becomes $58 900.

That is why the key parameter in trading is not a one-time profit, but average annual return taking into account reinvestment and drawdowns. Compound interest brings discipline and risk management to the surface.

Trading as a Business for Extracting Compound Interest

Many professional traders view their activity not as a series of trades, but as a business with its own ROE (return on equity). The goal of the business is to systematically generate profit and reinvest it. Then the trading account begins to grow exponentially.

Let us consider a simple model.

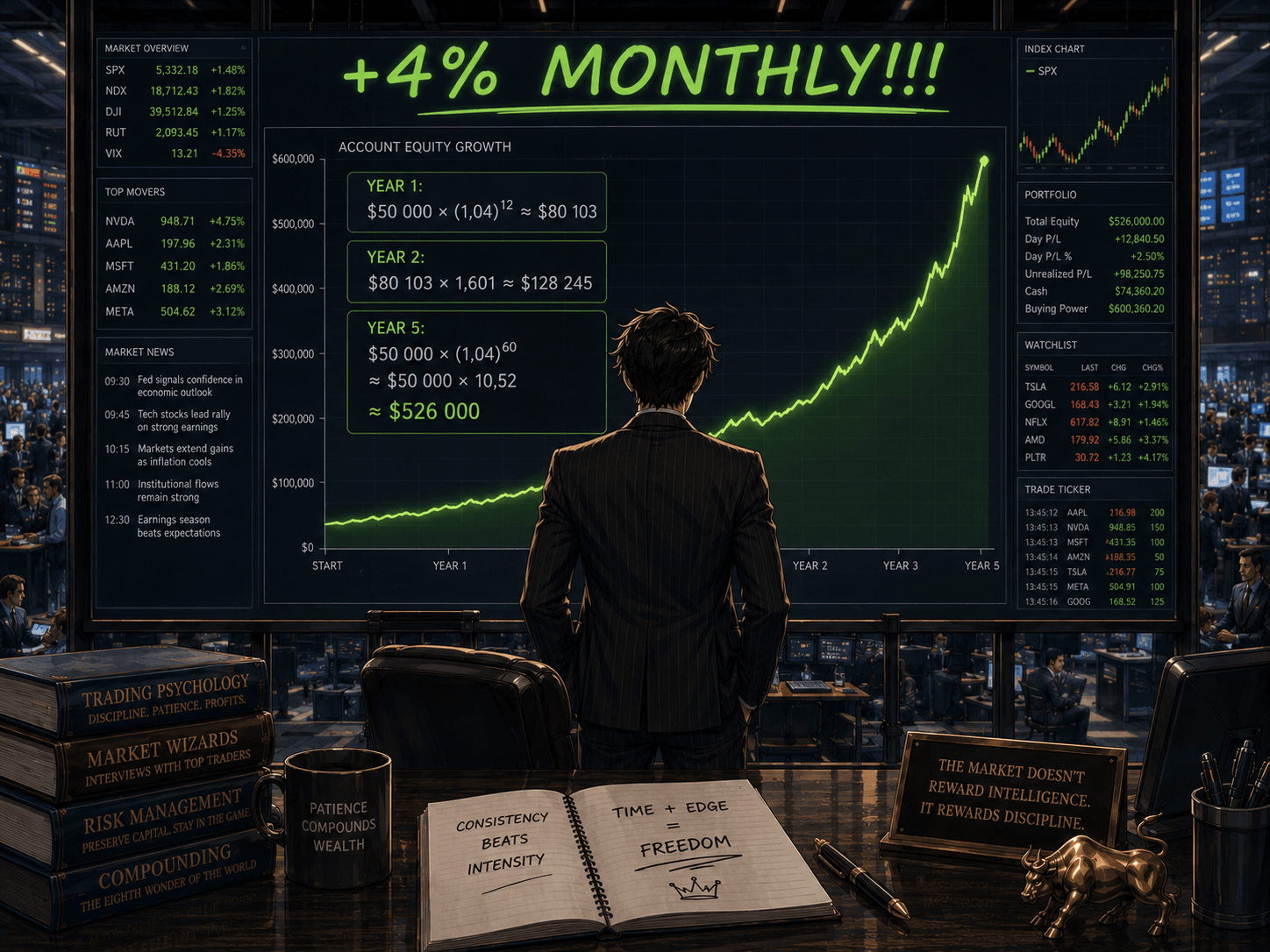

A trader has developed a strategy that produces an average of 4% per month with a maximum drawdown of 15% (controlled). He starts with capital of $50 000 and reinvests the profit monthly, without making withdrawals. Results by year:

Year 1: $50 000 × (1.04)^12 ≈ $80 103.

Year 2: $80 103 × 1.601 (coefficient for the second year) ≈ $128 245.

Year 5: $50 000 × (1.04)^60 ≈ $50 000 × 10.52 ≈ $526 000.

After 10 years, the account will exceed $5.5 million. At the same time, the trader merely systematically makes 4% per month, without allowing fatal losses.

ONCE AGAIN IN CAPITAL LETTERS: ONLY 4% PER MONTH OVER 10 YEARS TURNS 50 000 into 5 500 000+!!!

Of course, maintaining the same percentage return with growing capital is more difficult: instrument liquidity, slippage, psychological pressure. But the principle works: you only need to provide a positive mathematical expectation and preserve capital so that compound interest has time to show its magic.

The Psychology of Compound Interest: How Not to Interfere with Its Work

The most dangerous enemy of compound interest is the trader himself. The two main vices of a trader are the following.

<b>Withdrawing profit for consumption. </b>Every time you spend what you have earned on daily needs or emotional purchases, you steal future millions. An investor should pay himself a salary from another source or reinvest at least most of the income.

Breaking down into losses. One large loss can throw the account years back. If you have lost 50% of your capital, to return to the initial level, you need to earn 100% on the remaining money. This asymmetry kills the capitalization effect. Therefore professional risk management is the foundation.

Practical Recommendations: How to Implement the Principle in Your Trading

In order to start trading with the philosophy of compound interest in mind, you need to do the following.

Determine your rate of return and acceptable risk. Calculate what average monthly percentage of profit you are able to demonstrate steadily, taking drawdowns into account. Be honest.

Reinvest all profit until the account reaches the target level. For example, until the capital grows to the amount needed to generate passive income. Only after that should you start withdrawing a portion.

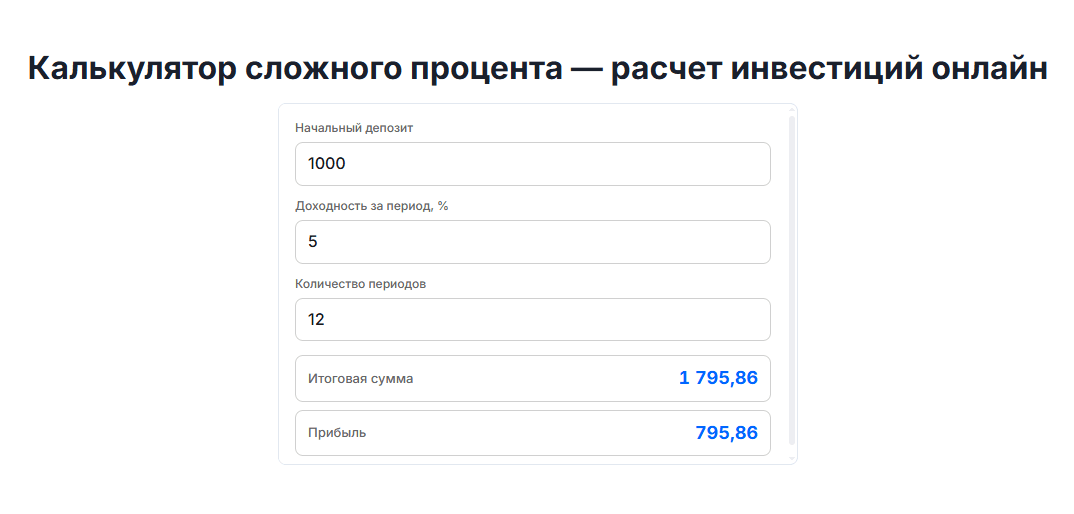

Use a compound interest calculator for forecasting. The compound interest calculator allows you to quickly create an account growth table by varying the rate of return. This will help you see the long-term perspective.

Avoid the risk of ruin. The rule is this: do not risk more than 1-2% of capital in one trade. Even a series of losses should not wipe out years of growth.

Remember commissions and taxes. Brokerage commissions and tax withdrawals work like negative compound interest. Optimize them in legal ways.