Central Bank Interest Rates: Impact on Currencies, Stocks, Bonds, and Cryptocurrencies

The central bank interest rate is one of the most important macroeconomic tools. In essence, it is the price of money in the economy. When the rate rises, loans become more expensive, money becomes more “valuable” over time, and demand for risky assets often declines. When the rate falls, financing becomes cheaper, there is more liquidity in the system, and markets usually receive support.

The impact of rates is not the same across different asset classes. For currencies, the stock market, bonds, and cryptocurrencies, the transmission mechanism is different. And even more important is that each central bank operates in its own economic environment: somewhere the main problem is inflation, somewhere it is recession, somewhere it is a weak currency, and somewhere it is supporting growth.

How the Interest Rate Dictates Market Behavior

The impact of interest rates set by central banks is varied and depends on the market and the economic cycle.

Currency Market (Forex)

In forex, the most direct and mechanistic channel of influence is observed. A rate increase makes the national currency more expensive (all else being equal) due to capital inflows into bonds with higher yields (Carry Trade).

It is worth noting that currencies react not to the decision itself, but to the divergence from the forecast and to the rhetoric (the Fed’s Dot Plot). The largest moves are seen in dollar pairs (EUR/USD, USD/JPY) because of a sharp change in the yield differential between Treasuries and European/Japanese bonds.

Stock Market (Indices and Stocks) and Bond Market

Here the relationship is more complex and more asymmetric. The market values companies’ future cash flows through discounting. The higher the risk-free rate (government bond yield), the lower the present value of future profits of growth companies (especially in the technology sector).

Sometimes the market rises on a rate hike if the Fed chair convinces everyone that the economy is strong (profit growth outweighs the discounting effect), and falls on a rate cut if it is perceived as a sign of recession.

The banking sector may rise as margins grow, while biotech and IT are more likely to enter a correction (the U.S. market has not been falling for a long time, only correcting).

For bonds, the relationship with rates is almost direct. When the central bank rate rises, yields on new bonds usually rise too, while prices of already issued securities fall. This is especially noticeable in long bonds, because they react more strongly to changes in expectations for future rates.

If the rate declines, bond prices generally rise. Therefore, bonds are often perceived as an asset sensitive to the monetary policy cycle.

Crypto Market

For a long time there was a myth that bitcoin did not correlate with traditional finance. After 2020, bitcoin’s correlation with the Nasdaq and S&P 500 indices became critically high. The crypto market behaves like an ultra-volatile penny stock.

The key driver for the crypto market is growth in the money supply. Therefore, rate cuts that lead to growth in the M2 money supply mean capital inflows into risky assets, and into the crypto market last of all. But monetary tightening drains liquidity; crypto falls first.

Note that a Fed rate increase strengthens the dollar. A strong dollar has historically pressured bitcoin.

Analysis of Reactions to Meetings of Global Central Banks

Not all central banks influence volatility equally. The regulator’s “weight” in the global economy and the phase of the monetary policy cycle matter.

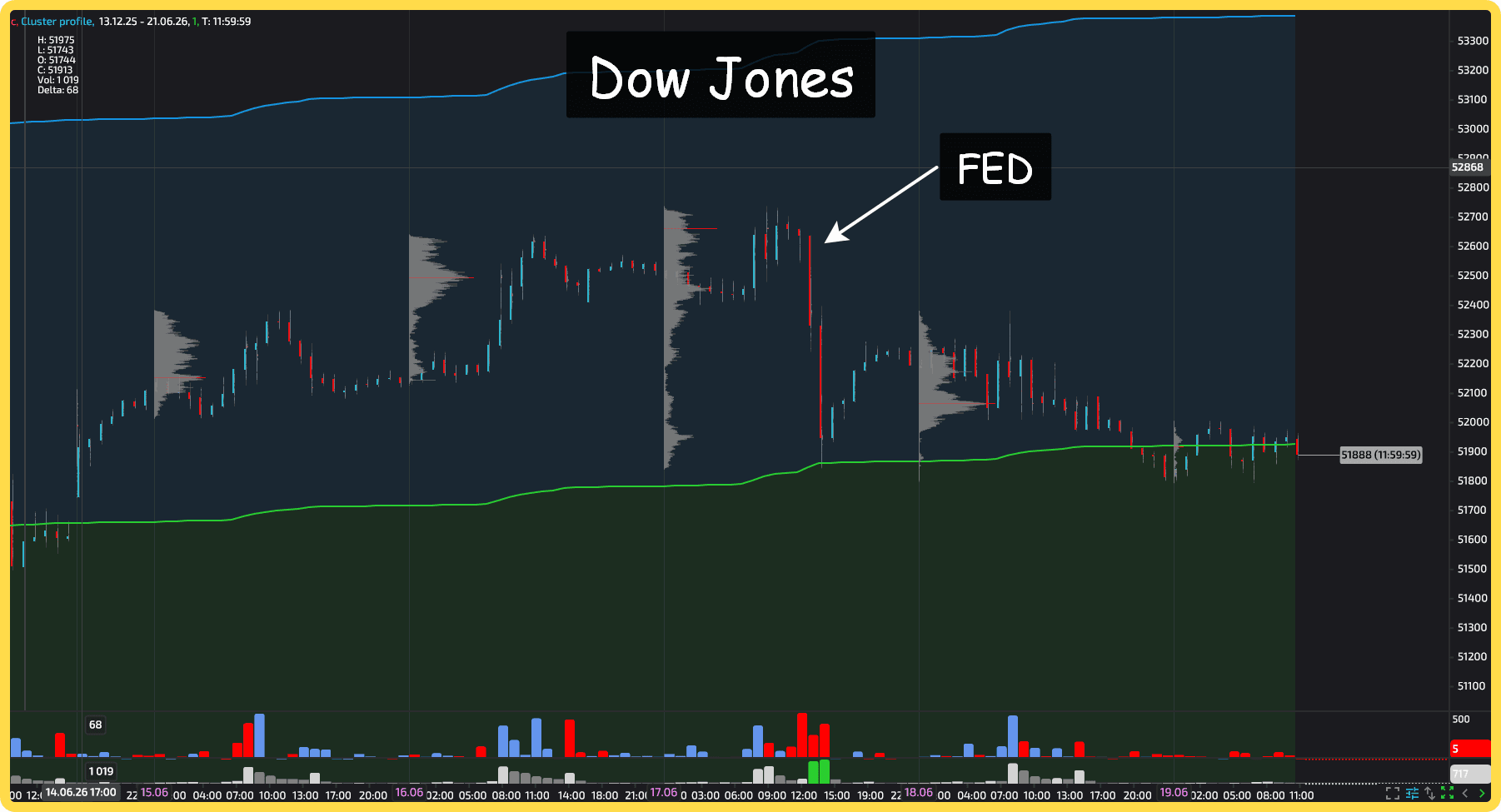

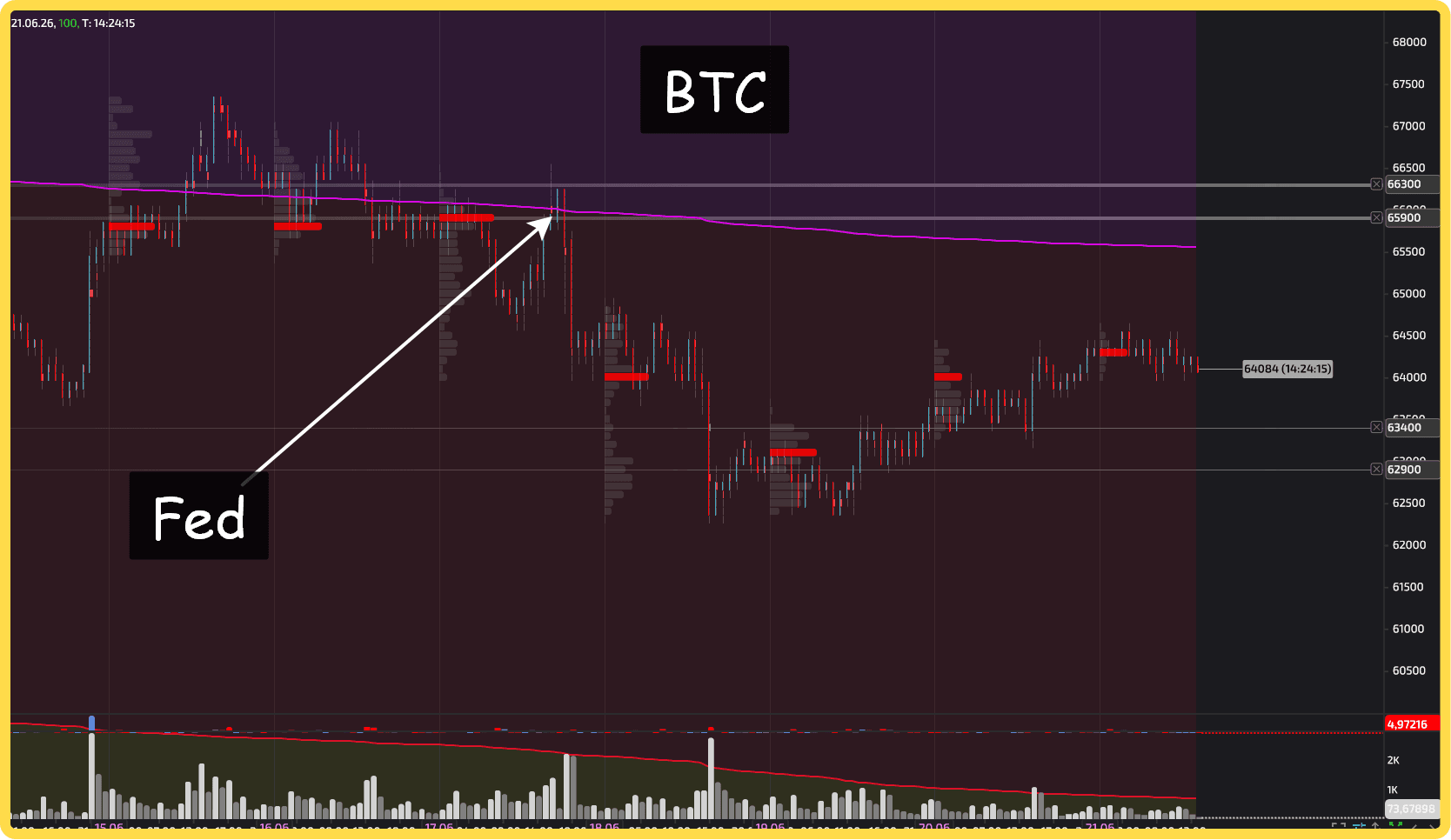

The Fed (U.S.): The Main One for All Markets

Fed decisions affect the whole world. This happens because the Fed manages the global reserve currency, the dollar. Tightening Fed policy sucks dollar liquidity out of the entire world, while easing policy, on the contrary, provides liquidity not only to the U.S., but also, after some time, to other economies.

Thus, FOMC (Federal Open Market Committee) meetings are the main event for all markets without exception.

Stock indices (S&P 500, etc.). The reaction to unexpectedly hawkish rhetoric often results in an intraday drop of 1.5–2.5%. However, statistically, after the meeting and press conference, a “reversal” pattern often kicks in as uncertainty is removed.

Cryptocurrencies. Bitcoin often moves ahead of time 5–10 minutes before the decision is released (insider/algorithmic front-running). Volatility in the publication hour jumps 3–5 times relative to the average daily level. Growth or decline can reach tens of percent, especially in secondary coins.

Currencies. Fed decisions of a long-term nature determine changes in medium-term and long-term trends in the currency market. During a tightening policy period (raising the discount rate), most currencies usually weaken against the dollar. But during an easing period (lowering the discount rate), on the contrary, the dollar weakens against most currencies.

ECB (Eurozone): fine-tuning the euro

ECB meetings have a special impact on the EUR/USD pair and European sovereign spreads (for example, Italian bond yields versus German ones).

Specifics of the EUR/USD reaction. A standard rate hike often leads to a fall in the euro if the market believes that the ECB is “behind the curve” and will not be able to raise rates as aggressively as the Fed. The euro rises only on hawkish rhetoric.

Volatility. The amplitude of EUR/USD moves at the moment of the decision is usually lower than at Fed meetings for the dollar index, but it rises sharply if the ECB head emphasizes fragmentation of the EU economy (spreads between countries) during the press conference. Then volatility flows from currencies into bonds, but the currency is also shaken.

Bank of Japan (BOJ): carry trade and global effect

For decades, Japan's central bank kept its rate at a negative or zero level, becoming the main source of almost free funding for global risk operations. Since mid-2026, the BOJ began carefully raising the discount rate.

Impact on JPY and the carry trade. The yen is a funding currency. Any hint of tightening (winding down YCC, raising the rate) instantly strengthens JPY, causing forced closing of short yen positions (carry trade unwind). This creates a “tsunami” across all markets: indexes fall from Tokyo to New York, flooding even crypto with volatility.

Nikkei 225. Paradoxically, the Japanese stock market often falls when the yen is weak and rises when it is strong, but at the moment of BOJ policy tightening, exporters suffer from a sharp strengthening of the currency, and the Nikkei may experience the strongest intraday collapses.

Bank of England (BOE): the pound and the inflation trap

The British regulator operates in unique conditions: chronically high inflation, weak economic growth, and the specifics of the sterling market.

GBP/USD and FTSE 100. The pound's reaction to the rate is straightforward, as in the case of the ECB.

Government bonds (GILTS). The main volatility often occurs in the government debt market. The 2022 crisis showed that unexpected BOE actions can provoke a collapse of pension funds and require emergency interventions, accompanied by wild turbulence in all British assets.

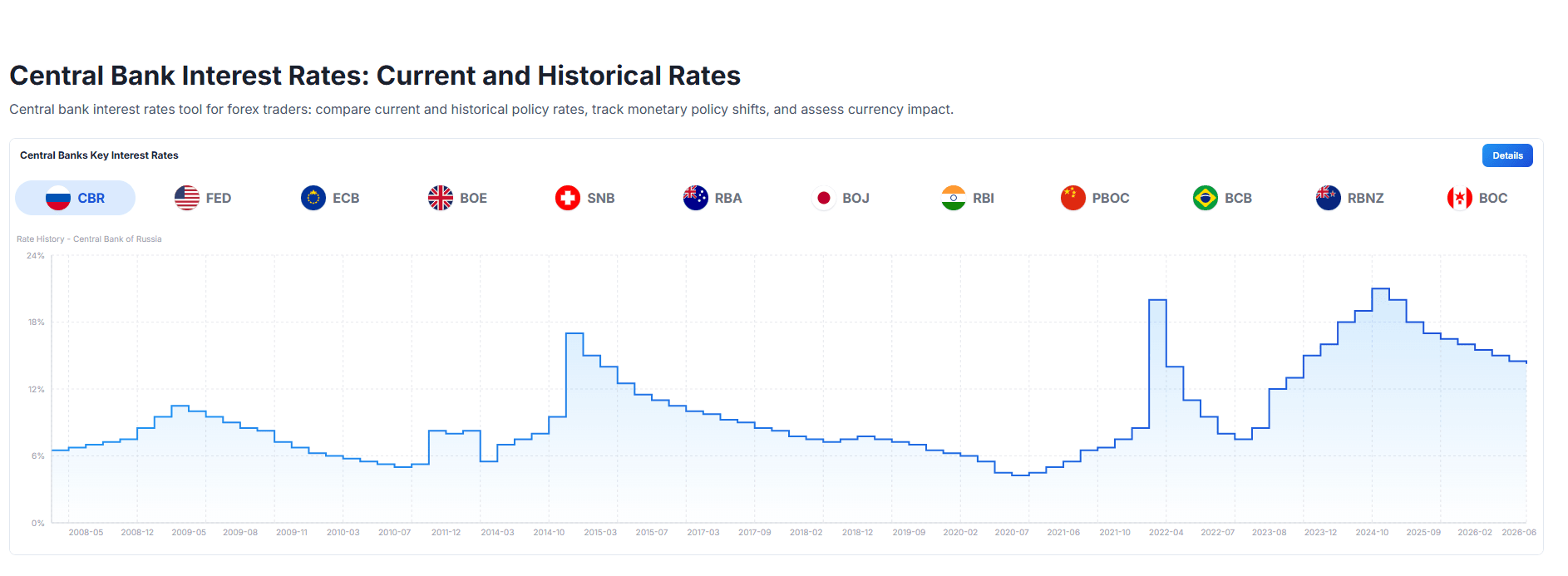

Central Bank of Russia (CBR): a special case of a closed loop

CBR meetings on the key rate have a huge impact on the local Russian market, but with limited transmission to external venues due to sanctions and infrastructure breaks. Previously, CBR policy strongly influenced the currencies of the former Soviet republics.

The ruble (USD/RUB, EUR/RUB, CNY/RUB). Before 2022, the classic logic worked: a rate hike strengthened the ruble through the carry trade.

Under conditions of limited convertibility and mandatory sale of foreign-currency revenue, the ruble's reaction became less predictable. The rate decision primarily affects yuan liquidity flows and domestic demand for currency from importers. Volatility on the meeting day often goes off the scale in the “foreign exchange market” exchange segment of the Moscow Exchange.

Moscow Exchange Index (IMOEX) and OFZ. Here the link is rigid. A rate increase crashes quotes of long OFZs and pressures stocks, especially developers and retailers. An unexpected rate hike can cause an intraday fall of the Moscow Exchange Index by 2-4%.

Combining central bank meetings and quarterly expiration

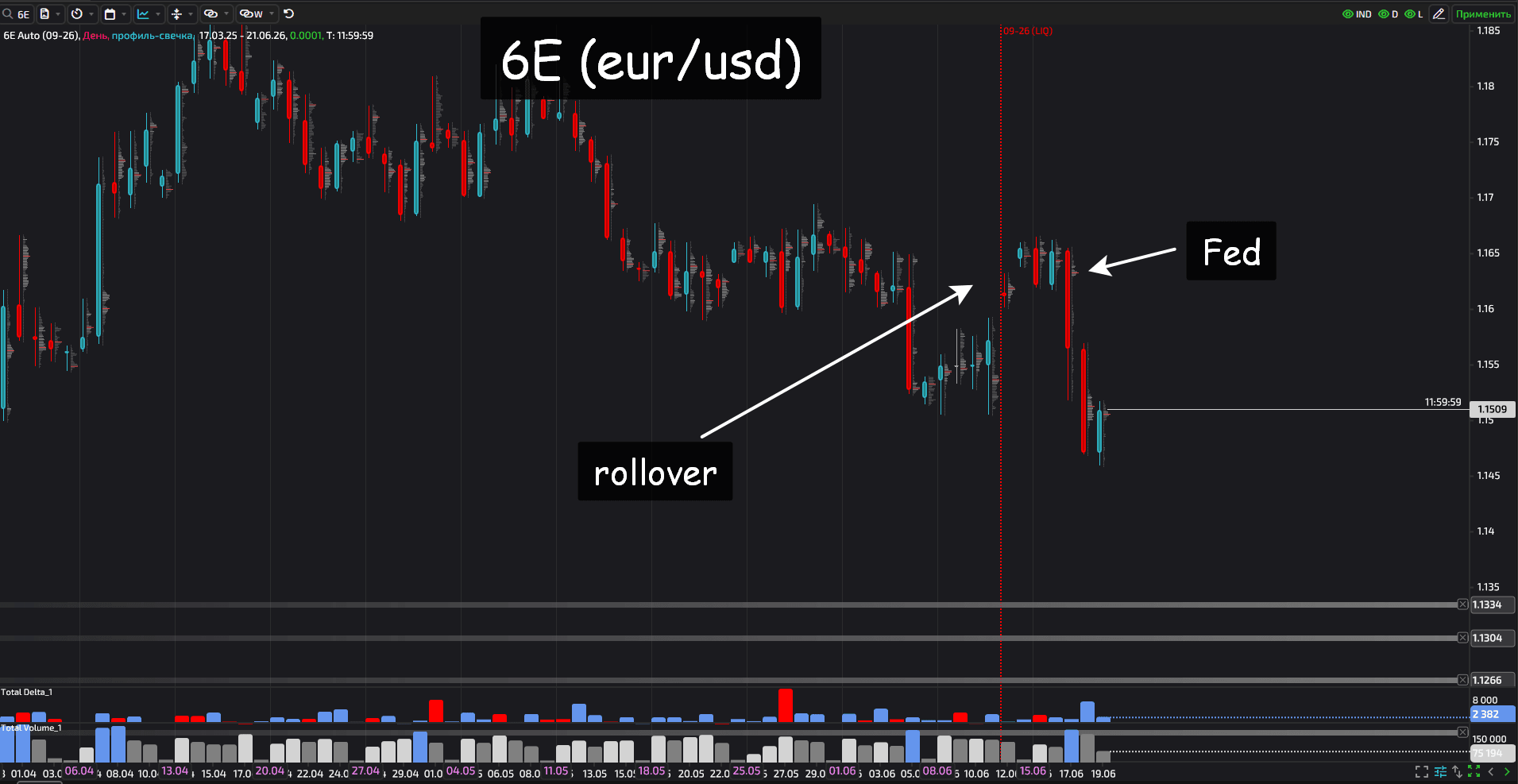

Quarterly expiration of futures and options is characterized by forced position closures by market makers. Major meetings of global central banks, primarily the Fed, usually take place together with expiration.

On an ordinary expiration day, volatility rises because of rollover - transferring positions from one quarterly contract to another). If a central bank meets on the same day or the day before, a multiplicative effect arises.

The mechanics of the process are as follows.

Gamma effect before the meeting (options). Before an important meeting, the options market becomes “more expensive.” Market makers who have sold options are forced to hedge their risks (gamma hedging) by buying or selling the underlying asset. The closer expiration is and the more important the meeting, the more aggressive the hedging, which rocks the market even before the news is released.

Fixing at the moment of expiration. Imagine the “Fed + quarterly expiration” scenario. Large funds hold colossal futures positions that are expiring. If the Fed issues an unexpected decision, funds cannot simply “sit out” the drawdown - they need to close the position here and now.

Rollover (futures and options). During the rollover period for quarterly securities, coinciding with a Fed meeting, medium-term and long-term market reversals often occur. At the same time, during these same periods, one can observe the birth of new serious movements within the previous dynamics.

Practical recommendations for a trader

Every trader should know the dates of central bank meetings that influence the trading instruments in their arsenal. To stay informed, we recommend using the “Central bank interest rates” tool. Here, information on the interest rates of 12 world central banks is collected in one place.

On days when Fed meetings and the expiration of quarterly securities coincide, it is dangerous to trade the first move after the news. At these moments, volatility is sharply elevated and spreads are widened. On the other hand, during this period the start of a new medium-term and long-term trend is possible, which gives an excellent opportunity to enter at the very beginning of a new impulse move.

On days when central bank meetings do not coincide with the expiration of quarterly futures, low volatility is most often observed without changes in global trends.

It is important to remember that most often after a move that began at the moment the interest rate was announced, a correction occurs to trade through the FVG (imbalance) zone.